One of the hottest stocks on Wall Street is partnering up with an aviation company that’s working to commercialize electric aircraft for regional travel. It’s an interesting collaboration between Palantir Technologies (PLTR), whose artificial intelligence-powered platform brings in new business hand over fist, and the much smaller Surf Air Mobility (SRFM).

Both companies are tapping the power of AI to reshape their industries, but their risk profiles couldn’t be more different. Which is the better buy right now—Palantir or Surf Air?

Palantir: The Big Data Juggernaut

Denver-based Palantir is a data mining company that uses its powerful Gotham and Foundry platforms to help customers sort data and provide real-time analytics. Both Gotham and Foundry are incorporated into Palantir’s groundbreaking Artificial Intelligence Platform, which uses interactive chat-style AI to allow users to access the platforms with minimal training.

The company has its roots as a government contractor that works with the military and intelligence agencies and famously was credited with helping to pinpoint the location of 9/11 mastermind Osama bin Laden. AIP has allowed Palantir to expand to other branches of government, as well as commercial businesses, as it helps manage supply chains, inventories, and provides predictive analysis so management can best position their companies for success.

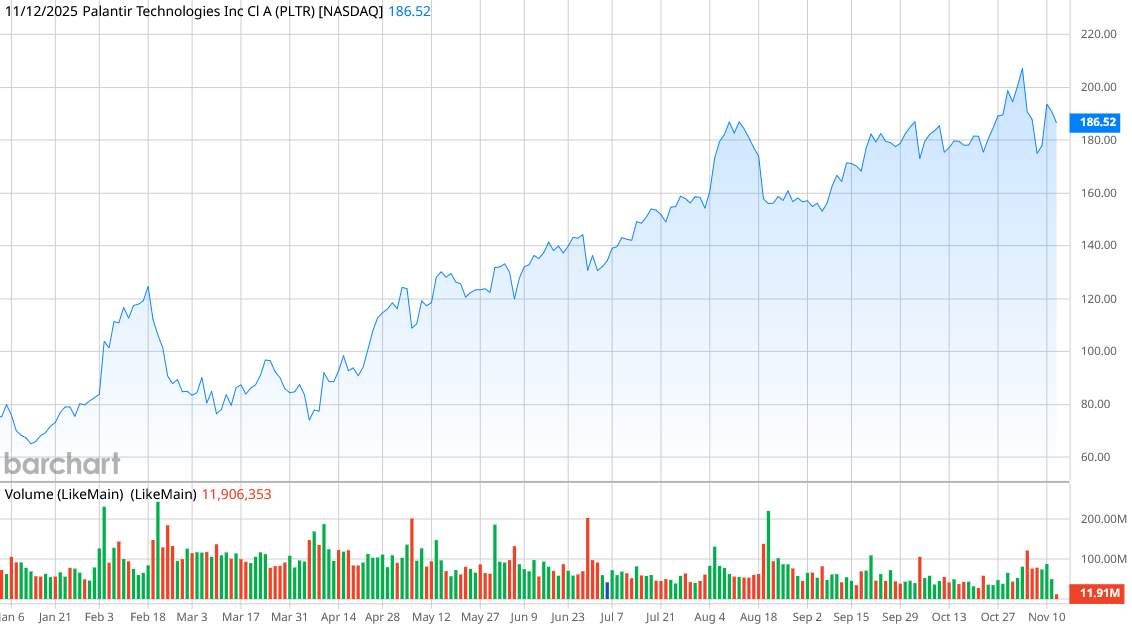

PLTR has been one of the hottest stocks in the stock market for the last two years, up 145% so far this year. It now sports a market capitalization of about $453 billion. Earnings in the third quarter showed gains of 63% on a year-over-year (YoY) basis to $1.18 billion. U.S. commercial revenue was up 121% to $397 million. U.S. government revenue was $486 million, increasing 52% from a year ago.

The major issue for Palantir, however, is its extreme valuation. Palantir has a price-to-earnings (P/E) ratio of 569 and a forward P/E of 345. Its price-to-sales (P/S) ratio is also extremely high at 160. But CEO Alex Karp brushes off those concerns. “It has indeed been difficult for outsiders to appraise our business, either its significance in shaping our current geopolitics or its value in the vulgar, financial sense,” he wrote in a letter to shareholders. “The reality is that Palantir has made it possible for retail investors to achieve rates of return previously limited to the most successful venture capitalists in Palo Alto.”

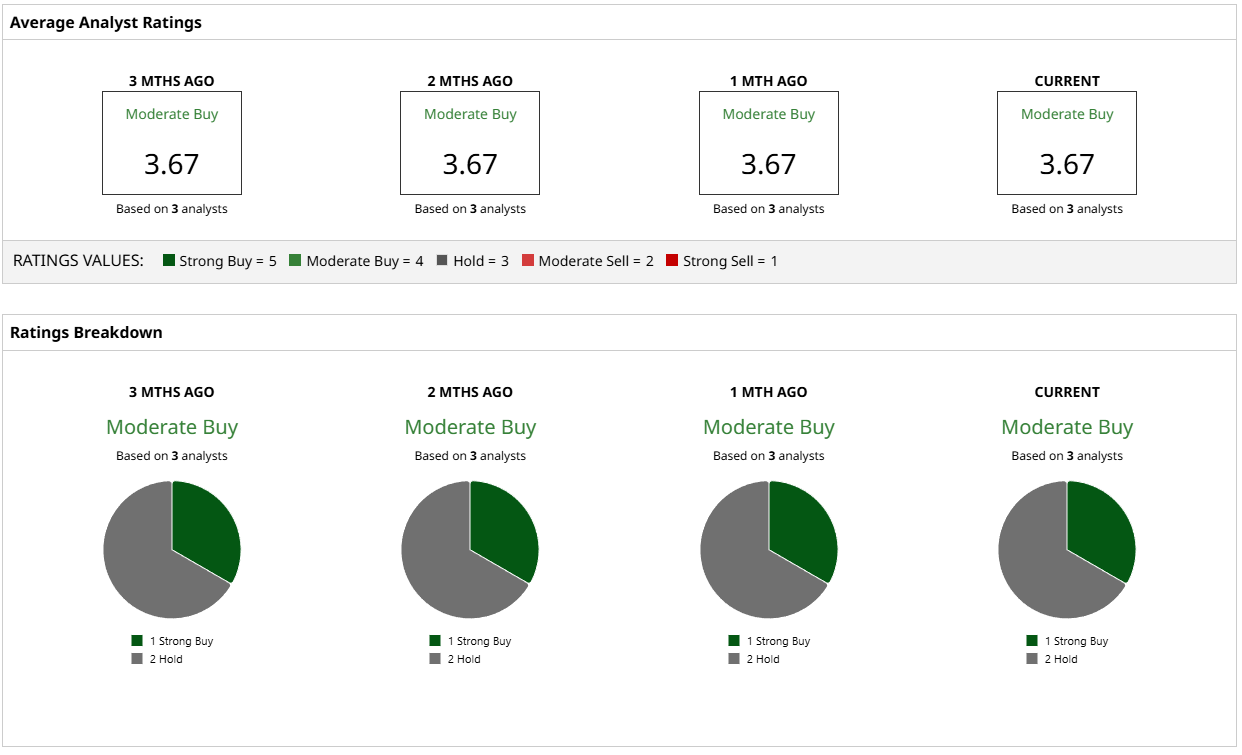

Analysts are split on PLTR stock, with 14 of 21 covering the stock recommending that investors “Hold.” Four of them put a “Strong Buy” on the stock, and three others recommend selling. The stock is currently trading just under its mean price target of $192.67.

Surf Air Mobility: The Struggling Aircraft Electrifier

Surf Air Mobility, whose headquarters are in Los Angeles, is much smaller than Palantir, with a market cap of only $130 million. The company is working on developing powertrain technology to electrify aircraft fleets and plans to offer its products to regional air carriers.

The stock has also been struggling this year as Surf Air seeks to gain traction. Shares are down 43% in 2025, falling to just $3 per share.

Management just announced a $100 million deal to develop and commercialize its proprietary SurfOS software, which includes $26 million from new equity issuances and $74 million in a senior secured convertible note to a private investor.

Surf Air said as part of its transaction, it will also issue $6 million in common stock to Palantir as a prepayment for continued access to its software and services. “This strategic transaction marks a pivotal moment for Surf Air Mobility, expanding and accelerating our transformation plan, while providing capital for continued development of SurfOS over the next several years and significantly strengthening our balance sheet,” CEO Deanna White said.

Earnings for the second quarter included revenue of $27.4 million, down 15% from a year ago. Management said the lower revenue was expected as the company exited unprofitable scheduled routes and shifted its focus to its On Demand business. Scheduled Service revenue dropped 12%, while the On Demand business increased 26%.

The company posted a net loss in the second quarter of $28 million versus a loss of $27 million in Q2 2024. Surf Air is expected to post Q3 earnings after the closing bell today.

Only three analysts cover Surf Air stock, with one suggesting it is a “Strong Buy” and the other two giving the stock a “Hold” rating. Analysts have a mean price target of $7.88, which would be a 154% increase.

Which Stock Is a Better Buy?

It depends entirely on your risk tolerance. Palantir is bringing in new business hand over fist, closing more than 200 deals in the third quarter valued at more than $1 million each. Surf Air, meanwhile, has massive potential but currently is cutting corners—and giving away stock to Palantir to maintain access to Palantir’s software.

For me, PLTR is the better stock, despite its steep valuation.

On the date of publication, Patrick Sanders had a position in: PLTR . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- D-Wave’s Contracts Could Be Worth ‘Millions of Dollars.’ Should You Buy QBTS Stock Now?

- Bargain Buy or Risky Bet? Bath & Body Works Slides to 52-Week Low

- Michael Burry Accuses Meta Platforms of ‘Common Fraud’ and Inflated Earnings. Should You Still Buy META Stock Now?

- As IBM Rallies on a Quantum Computing Breakthrough, Here’s Where the Stock Could Be Headed Next