Broad-market leaders often emerge after a single catalytic development reshapes an industry’s competitive map. Sometimes those catalysts are incremental, and sometimes they’re seismic, forcing investors to reassess positioning.

Nvidia (NVDA) just experienced the latter as it announced it would license AI inference technology from startup Groq (a non-exclusive agreement). Under this deal, Groq’s founder, Jonathan Ross, president Sunny Madra, and other key engineers will join Nvidia to help advance Groq’s low-latency inference chips. Reports peg the transaction at about $20 billion in cash. That was Nvidia’s largest deal to date, although neither company officially confirmed the price. Groq will remain an independent entity under new leadership.

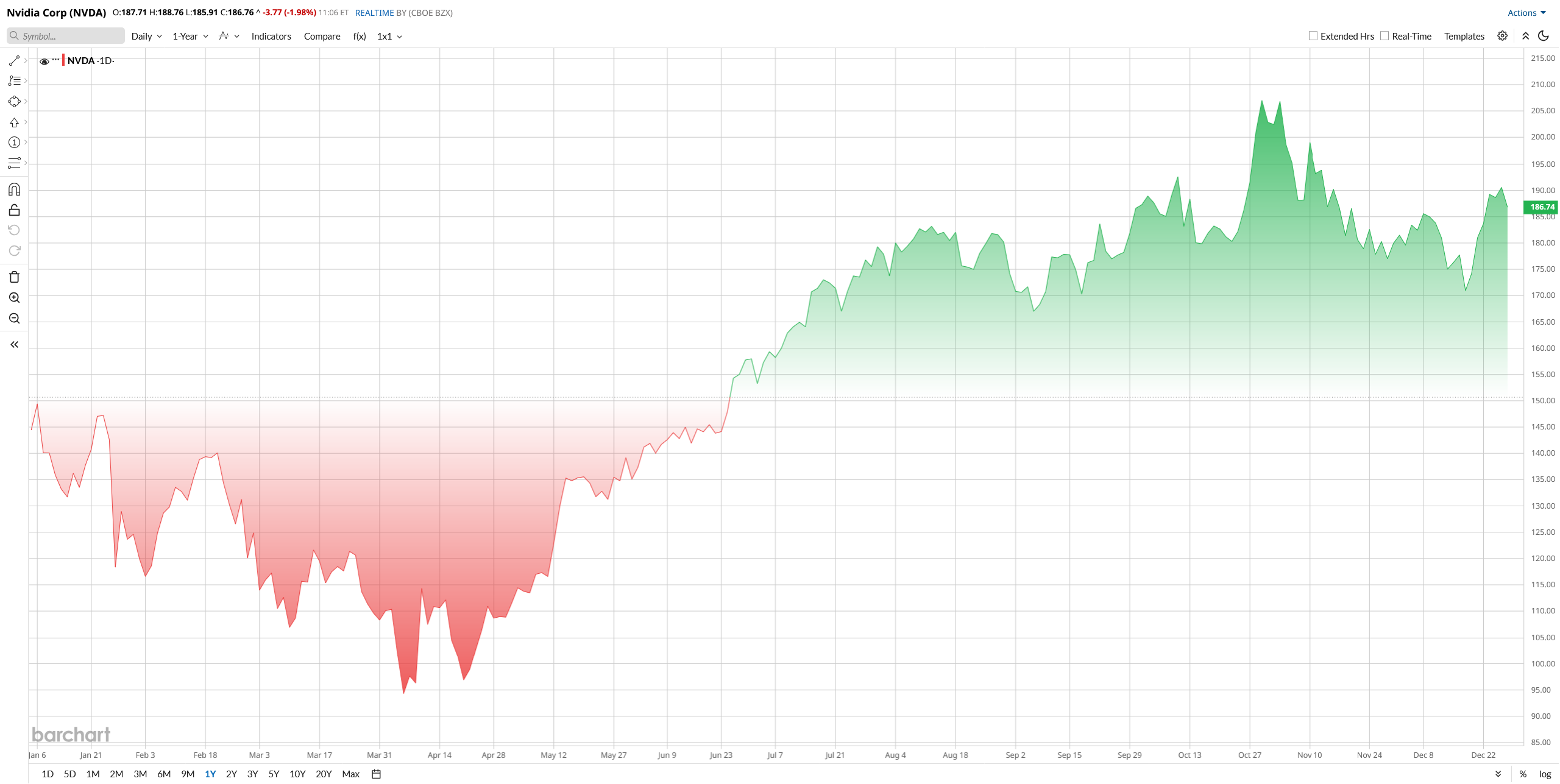

Nvidia Stock Performance

Nvidia shares jumped on the news. NVDA climbed roughly 2% on Dec. 26, intraday trading in the $188 to $192 range immediately after the announcement. This was built on a late-2025 rally as NVDA was up about 8% over the prior five trading days. Overall, the stock is near all-time highs. Technical analysts note that clearing the previous resistance around $194 would open the way toward higher targets in the $229 to $250 zone. Conversely, any pullback into the $180 to $190 range is now considered a buying opportunity, with strong support expected in that area.

For reference, NVDA stock is currently significantly overvalued compared to its peers. For example, its price-to-sales ratio is 25, notably higher than the sector median of 3.

Impact of the Gorq Deal With Nvidia

Analysts widely agree that the Groq deal reinforces Nvidia’s leadership in AI inference. By bringing Groq’s low-latency Language Processing Unit technology and key engineers into its ecosystem, Nvidia significantly expands its capabilities in real-time AI workloads such as robotics, edge inference, and always-on data center applications. The move reflects a broader industry shift away from pure AI training toward continuous, 24/7 inference computing, positioning Nvidia at the center of the next phase of AI adoption.

Just as important, the deal strengthens Nvidia’s competitive moat. Absorbing Groq’s talent and intellectual property reduces future competitive threats while accelerating innovation internally. With massive free cash flow and a fortress balance sheet, Nvidia can comfortably absorb a roughly $20 billion transaction without financial strain, underscoring its long-term strategic and financial dominance.

Nvidia Delivered Blowout Q3

Nvidia's fiscal third-quarter results were quite strong, coming ahead of estimates. The chipmaker hit record revenue of $57 billion, a 62% year-over-year (YoY) jump that topped guidance of $54 billion and accelerated from the prior quarter’s 56% growth. While revenue surged, gross margins retreated about 140 basis points, and the firm has yet to show operating leverage; nevertheless, it remains highly profitable with a 55.8% net margin.

Networking product momentum gained strength, challenging incumbents like Arista and letting Nvidia capture more of the data center stack. The balance sheet is robust, with $60.6 billion in cash versus $8.5 billion of debt, supporting dividends, buybacks, and strategic investments.

Looking ahead, management guided roughly $65 billion for the next quarter, implying about 65% YoY growth, and sustained supply execution and cloud demand will determine if growth endures broadly.

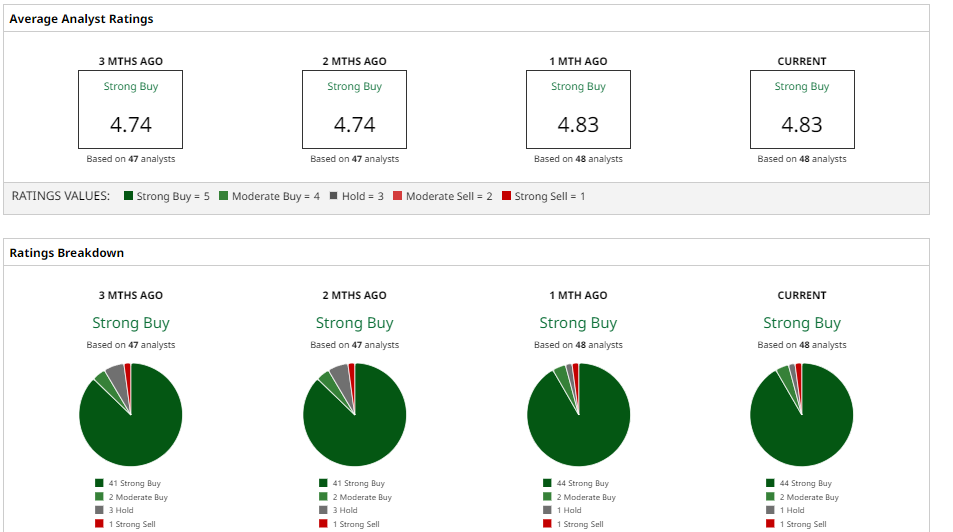

What Do Analysts Say About NVDA Stock?

As we are heading to 2026, many analysts have reiterated their positive views on NVDA stock following the Gorq deal. Bank of America reiterated its “Buy” rating on Nvidia with a $275 12-month price target, calling the Groq deal a surprise but ultimately a strategic move. The firm noted that the transaction highlights Nvidia’s awareness that the AI market is shifting from training-heavy workloads toward real-time inference, which requires more specialized silicon.

Baird maintained an “Outperform” rating and also set a $275 price target, arguing that while Nvidia’s GPUs should continue to dominate long term, integrating Groq’s ASIC-based inference technology could materially expand Nvidia’s total addressable AI market over time.

Bernstein kept its “Outperform” stance, noting that although a $20 billion price tag may appear steep, it is manageable given Nvidia’s massive cash position and multi-trillion-dollar market capitalization.

Overall, analysts remain bullish, with the consensus target at $256, which suggests the stock still could gain approximately 37% from the current price.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- This 1 Cheap Quantum Computing Stock Could Be a Top Buy for 2026

- Short Sellers Are Betting Against Lumentum Stock. Will They Be Proven Right?

- A Santa Claus Rally Could Supercharge Nvidia Stock Into 2026. Should You Buy Shares Here?

- A Less-Costly Way to Buy Costco to Gain Leveraged Upside in COST Stock