Rare earths are back in focus because supply chain control, not just demand, is now driving the investment story. China accounts for nearly 70% of the world’s rare earth mining and roughly 90% of global rare earth processing, keeping a tight grip on materials used in everything from EVs to consumer electronics, so even a “delay” can move markets. However, China’s promise to delay its newest rare earth export restrictions for a year has created a narrow window for the U.S. and allies to build alternatives faster.

That temporary opening is why investors are hunting for non‑Chinese exposure heading into 2026. Neo Performance Materials (NOPMF) has become one of the clearest public-market proxies, with a year-to-date (YTD) gain of 108%. After a run like that, should investors keep buying for the new year, or is the easy upside already gone? Let's find out.

What the Latest Quarter Really Shows

Neo Performance Material, with a market cap of about $480.5 million, is a Canada‑based producer of engineered rare earth materials and high‑performance magnets. Its dividend profile is modest but tangible, with a forward annual dividend of $0.29, implying a yield of roughly 2.51%.

NOPMF is currently trading at $11.75 as of this morning, Dec. 30. While NOPMF stock has slid 19% in the past three months and 5% in the past month, it is still up 108% YTD.

This valuation now embeds higher expectations. It trades at a forward P/E of 26.25x versus a sector median near 17.75x, suggesting investors are willing to pay a premium for its rare earth leverage and earnings momentum.

Their latest earnings report, released on Nov. 13, helps explain that confidence. This quarter ending 09/25 saw EPS of $0.19 versus a $0.15 consensus, a $0.04 beat that translated into a 26.67% positive surprise. It also showed Q3 2025 revenue of $122.2 million compared with $111.3 million a year earlier, while YTD sales rose to $358.5 million from $340.9 million, signaling steady demand for its high‑value products.

The company posted $8.5 million, or $0.20 per share, in Q3 2025 versus just $1.1 million, or $0.03 per share, a year earlier, and YTD adjusted EPS climbed to $0.48 from $0.16. That performance helped lift adjusted EBITDA to $19.2 million for Q3 and $55.3 million for the first nine months, with margins of 15.7% for the quarter and 15.4% YTD, showing slight quarterly compression but a solid improvement versus the prior YTD period.

Neo’s Next Leg of Growth

Neo’s recent fundamental moves help explain why the market is suddenly willing to pay up for its rare earth story. The company is putting real capital behind Europe’s push to reduce dependence on Chinese supply, with a heavy rare earth pilot line at its Silmet facility now nearing completion and commissioning expected in early 2026.

This pilot line is designed to produce dysprosium and terbium, two critical inputs for high‑performance permanent magnets that need to operate reliably at high temperatures in EV motors and other demanding applications.

The company has already completed the sale of a majority equity interest in certain Chinese rare earth separation assets, which further tilts its footprint toward Western‑aligned supply chains and frees up resources to backstop this European build‑out.

Neo has also moved from plans to a physical footprint. The company has held the grand opening of a new, state‑of‑the‑art permanent magnet manufacturing facility in Estonia. That inauguration is positioned as a milestone in building a resilient, independent European base for critical rare earth magnets. Those magnets are tied directly to electric vehicles, wind energy, robotics, and the broader energy transition.

NOPMF is also tightening its commercial ties with one of the most important customers in the region’s industrial landscape. The company recently announced an extension of its strategic partnership for high‑performance magnets with Robert Bosch GmbH, one of the world’s leading automotive and industrial technology groups.

This agreement keeps Neo embedded in Bosch’s long‑term plans for advanced magnet applications, from electrified powertrains to precision industrial systems, and helps underpin volumes for the new European magnet facility as it ramps up.

What Wall Street Expects Next

Analysts are not treating Neo’s 100%+ run in 2025 as a one‑off pop. They are already looking ahead to the next catalyst, with the next earnings release scheduled for March 17, 2026, covering the crucial holiday season quarter that will close out fiscal 2025. For the current quarter ending this December, the average EPS estimate sits at $0.10, a big swing from the prior year’s -$0.12, which translates into an expected YoY growth rate of about 183%.

For the next quarter, in March, the Street is looking for EPS of $0.15 versus $0.08 a year earlier. That implies another hefty jump, with estimated growth of roughly +87.50% as Neo’s higher‑margin rare earth and magnet volumes ramp.

The full‑year numbers tell an even sharper inflection story, as for fiscal December 2025, the average EPS estimate sits at $0.44 compared with just $0.05 in the prior year. That works out to a projected growth rate of about 780%.

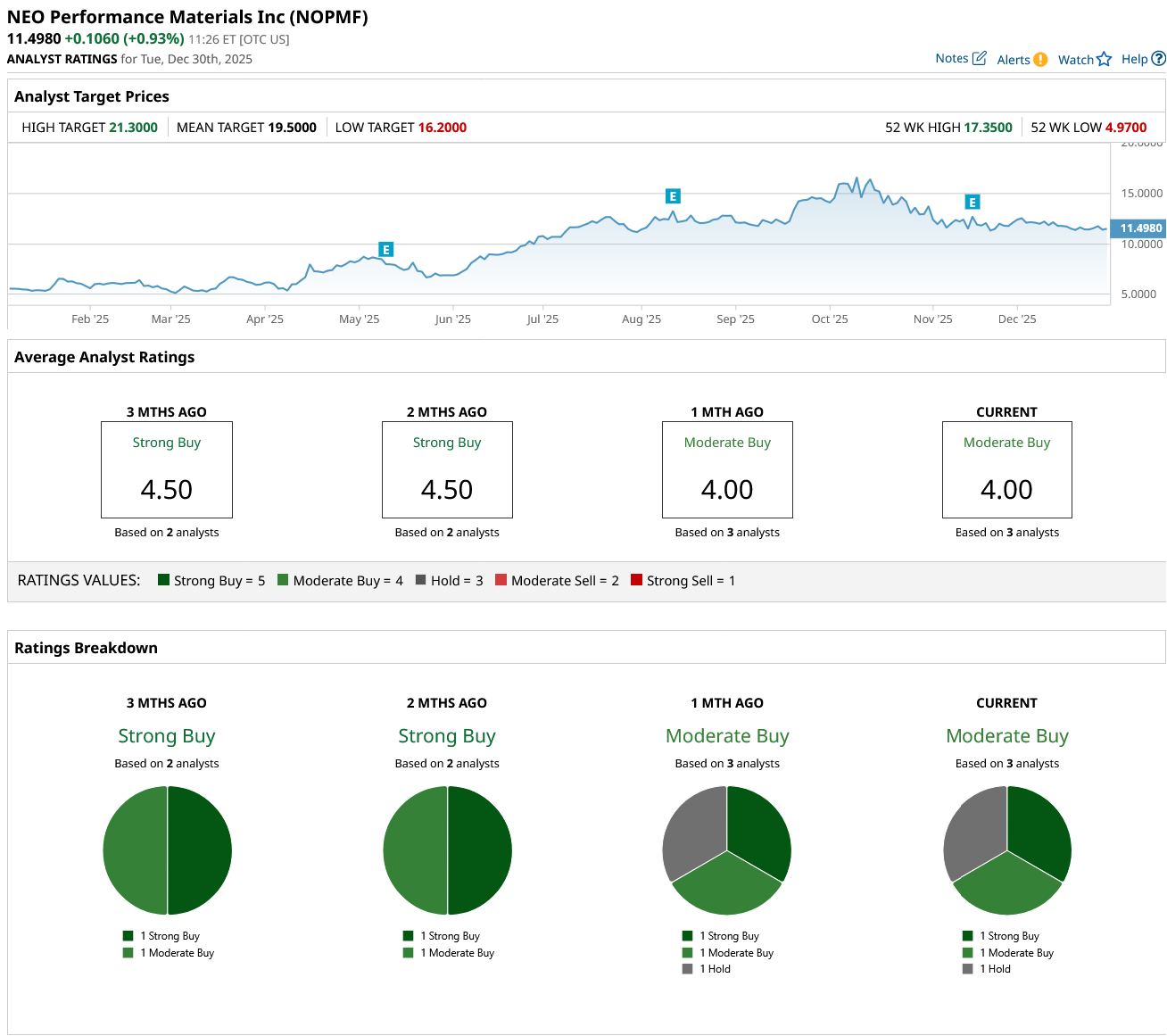

The rating and target picture back that up, even if coverage is still thin, with a consensus “Moderate Buy” on NOPMF based on three analysts. Its average price target comes in at $19.50, which, against the recent price of about $11.50, implies roughly 70% upside from here.

Conclusion

If the goal is long-term exposure to the West’s push to build non‑Chinese rare earth and magnet capacity, NOPMF still looks like a reasonable “keep buying,” but only in small, disciplined increments after a 105%+ year. Most likely, shares will drift higher into 2026 if results continue to improve, but expect pullbacks and choppy trading after such a considerable run. A clean break back above recent levels would need fresh proof in upcoming quarters, so averaging in (not chasing spikes) is the safer way to stay involved.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Altria’s (MO) Unusual Options Activity Just Tipped Its Hand to a Hidden Multi-Dimensional Opportunity

- Nvidia Just Officially Bought $5 Billion Worth of Intel Stock. Should You Buy INTC Too?

- This Rare Earths Stock Gained 108% in 2025. Should You Keep Buying It for the New Year?

- Play the Red-Hot Metals Market with This 1 Aluminum Stock