The possible decision by President Donald Trump’s administration to green light exports of the high-performance Nvidia (NVDA) H200 artificial intelligence (AI) chips to China could mark a dramatic turning point for the semiconductor giant and potentially a major catalyst for investors. After export restrictions that wiped out Nvidia’s access to China’s lucrative AI market, the reversal might restore billions in lost revenue and reopen one of the world’s largest growth markets for AI infrastructure.

U.S. Commerce Secretary Howard Lutnick said the decision on whether Nvidia can export its high-end H200 chips to China is now directly in Trump's hands. Trump is weighing two national security trade-offs — keeping China tied to U.S. technology by allowing some chip sales, or restricting access to preserve the United States' edge in the AI race.

Nvidia, which argues that current rules leave China’s massive data-center market to foreign competitors, has already been limited to selling a downgraded H20 chip approved earlier this year. The debate comes as China recently banned foreign AI chips in state-funded data centers, adding new urgency to Trump’s decision.

Meanwhile, given how integral China remains to global AI demand, a favorable ruling could reignite enthusiasm about Nvidia’s near-term growth prospects. But as with any geopolitical inflection point, the upside may come hand-in-hand with renewed scrutiny and regulatory uncertainty, making this a high-stakes moment for both the company and its shareholders. Is this the right entry point in NVDA stock?

About Nvidia Stock

Nvidia is a global leader in accelerated computing and AI, renowned for pioneering the graphics processing unit (GPU) that revolutionized gaming, data centers, and AI-driven computing. Headquartered in Santa Clara, California, Nvidia’s technology now powers everything from high-performance gaming and cloud computing to autonomous vehicles and generative AI applications. With a market capitalization of roughly $4.4 trillion, Nvidia stands among the world’s most valuable companies, driven by its dominance in AI infrastructure and continued innovation in next-generation chip design.

The stock price journey of NVDA has been significant. NVDA stock has gained 34% year-to-date (YTD), a strong surge that underscores growing investor confidence. Over the past 52 weeks, the stock has delivered a 28% total return, marking yet another year of solid gains.

What’s fueling this performance? First and foremost, the explosion in demand for AI. Nvidia remains a leading supplier of GPUs that power AI training and data-center workloads. Analysts and investors are pricing in continued strong growth as companies worldwide invest heavily in AI infrastructure.

Meanwhile, Nvidia hit a 52-week high of $212.19 on Oct. 29 and also became the first publicly traded company ever to surpass a $5 trillion market cap, a milestone that captured investor attention. However, NVDA stock is currently down 15% from that high.

The surge was driven by a perfect storm of optimism around Nvidia’s dominance in AI infrastructure and a wave of major strategic developments. The company revealed a massive pipeline for AI chip orders — reportedly amounting to $500 billion over the next several quarters — and announced partnerships and investments spanning AI supercomputing, 6G telecom networks, and cloud infrastructure.

Growing global demand for high-performance GPUs and AI hardware, fueled by the ongoing AI boom, reinforce the view that Nvidia is becoming the backbone of the next generation of computing.

Nvidia’s dominant position has led it to trade at a pronounced premium valuation compared to its industry peers, at 41 times forward earnings.

A Strong Q3 Performance

Nvidia delivered a particularly strong showing in its third quarter of fiscal 2026 results, underscoring just how deep the demand for AI infrastructure has become. On Nov. 19, the company reported revenue of $57 billion for the quarter ended Oct. 26, representing a 62% year-over-year (YOY) jump and a 22% increase from the prior quarter.

The company’s data-center business was the main engine, with data-center revenue hitting $51.2 billion, up 66% from a year ago, reflecting surging demand for AI-ready GPUs and cloud computing infrastructure. The firm’s profitability remained strong, with non-GAAP gross margins held around 73.6% and the non-GAAP EPS at $1.30, a 60% YOY rise and comfortably ahead of Wall Street estimates.

Management also offered bullish forward guidance, expecting around $65 billion (plus or minus 2%) in revenue in the fourth quarter of fiscal 2026. That projection suggests confidence in continued strong demand for its AI chips and data-center gear despite macroeconomic headwinds or geopolitical uncertainty.

Analysts tracking Nvidia project EPS to climb 50% YOY to $4.39 in fiscal 2026, then grow another 53% to $6.73 in fiscal 2027.

What Do Analysts Expect for Nvidia Stock?

Last month, Bernstein reaffirmed its “Outperform” rating and $275 price target on Nvidia after reviewing the company’s weekend memo that aimed to counter recent bearish claims circulating in the media and on social platforms. The memo addressed concerns about receivables, working capital, depreciation timelines, and revenue circularity. Bernstein said Nvidia’s explanations were generally solid and effective in easing these doubts.

Raymond James also reaffirmed a “Strong Buy” rating on Nvidia with a $272 target after the company issued the memo refuting recent fraud allegations, reinforcing confidence in its fundamentals. Raymond James also pointed to continued demand for Nvidia’s Blackwell platform and exceptional revenue growth, underscoring the firm’s view that Nvidia’s long-term trajectory remains solid despite recent controversy.

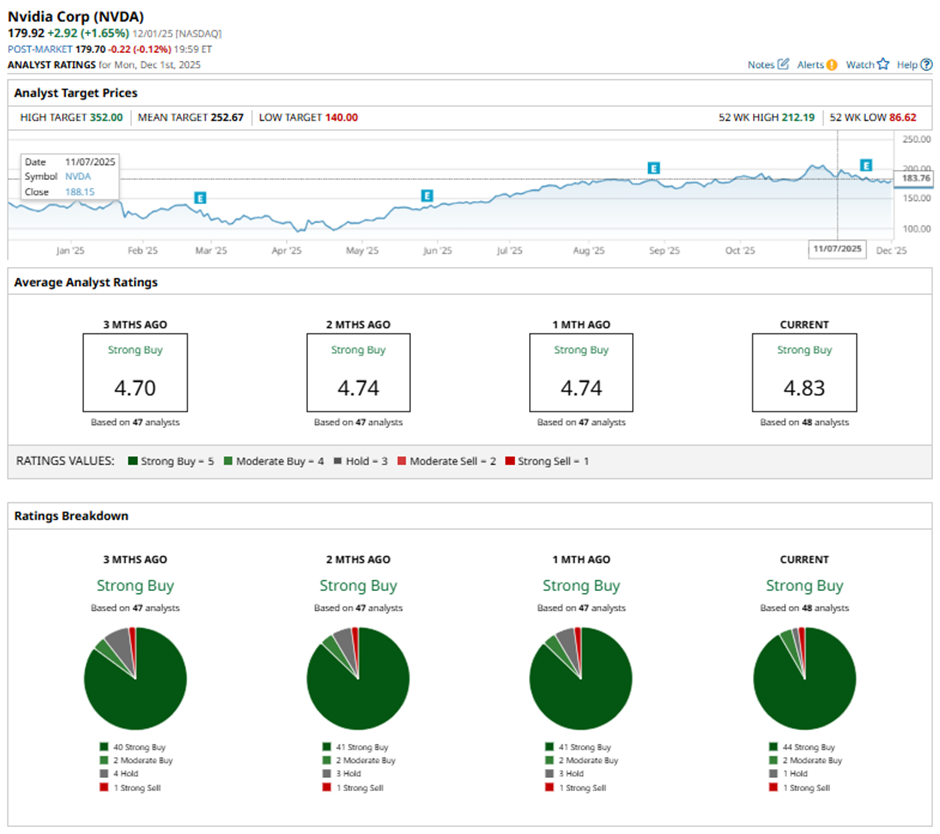

Wall Street’s bullishness is evident in Nvidia having a consensus “Strong Buy” rating. Of the 48 analysts covering NVDA stock, 44 advise a “Strong Buy,” two suggest a “Moderate Buy,” one analyst is on the sidelines with a “Hold” rating, and one offers a “Strong Sell” rating.

The average analyst price target for NVDA is $252.67, indicating potential upside of 41%. The Street-high target price of $352 suggests that the stock could rally as much as 97% from here.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart