Delta Air Lines, Inc. (DAL) is one of the largest and most established airlines in the world, headquartered in Atlanta, Georgia. It operates an extensive global network serving more than 300 destinations across more than 50 countries. With a market cap of $43.2 billion, the company offers flight status information, bookings, baggage handling, and other related services.

Shares of this global airline leader have underperformed the broader market considerably over the past year. DAL has declined 2.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 15%. However, momentum has rebounded more recently, with DAL surging 18.4% over the past six months, comfortably outpacing the index’s 9.2% gain.

Narrowing the focus, DAL has also trailed the U.S. Global Jets ETF’s (JETS) 6.4% rise over the past year but exceeded the ETF’s 12.2% return over the past six months.

On Jan. 13, Delta Air Lines reported its Q4 FY2025 earnings, prompting a modest 2.4% dip in its shares as investors digested the results. Despite the market reaction, the airline delivered a strong year-end performance, with operating revenue climbing 3% year over year to nearly $16 billion, fueled by diversified revenue streams and resilient demand, even amid disruptions from a temporary U.S. government shutdown. On a non-GAAP adjusted basis, Delta reported earnings per share of $1.55, in line with expectations, reflecting underlying operational strength despite broader macro headwinds.

Delta is projecting strong momentum heading into 2026, signaling confidence in both top-line growth and profitability expansion. For the first quarter of 2026, the airline expects revenue to increase by 5%–7% year over year, driven by continued strength in both consumer and corporate demand. For the full year 2026, Delta is guiding toward adjusted earnings per share in the range of $6.50 to $7.50, which implies roughly 20% growth in EPS compared with 2025 at the midpoint of the forecast.

For the current fiscal year, ending in December 2026, analysts expect DAL’s EPS to increase 24.1% to $7.22 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

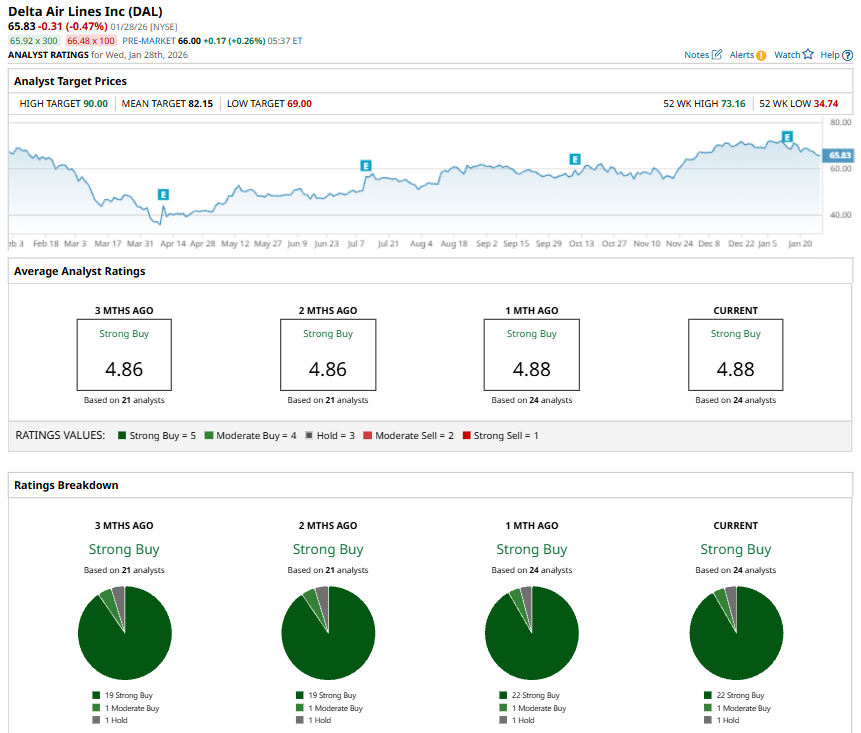

Among the 24 analysts covering DAL stock, the consensus is a “Strong Buy.” That’s based on 22 “Strong Buy” ratings, one “Moderate Buy,” and one “Hold.”

This configuration is bullish than two months ago, with 19 analysts suggesting a “Strong Buy.”

On Jan. 14, UBS analyst Atul Maheswari maintained a “Buy” rating on Delta Air Lines while trimming the firm’s price target to $87 from $90.

The mean price target of $82.15 represents a 24.8% premium to DAL’s current price levels. The Street-high price target of $90 suggests an ambitious upside potential of 36.7%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart