Palantir Technologies Inc. (PLTR), based in Denver, Colorado, builds advanced data analytics software for government and commercial clients. With a market capitalization of around $400.1 billion, it firmly occupies “mega-cap” territory, reserved for companies that are valued above $200 billion.

The company supports this stature through a diversified portfolio of platforms such as Gotham, Foundry, Apollo, and AIP, serving intelligence analysis, enterprise operations, system deployment, and large language model integration.

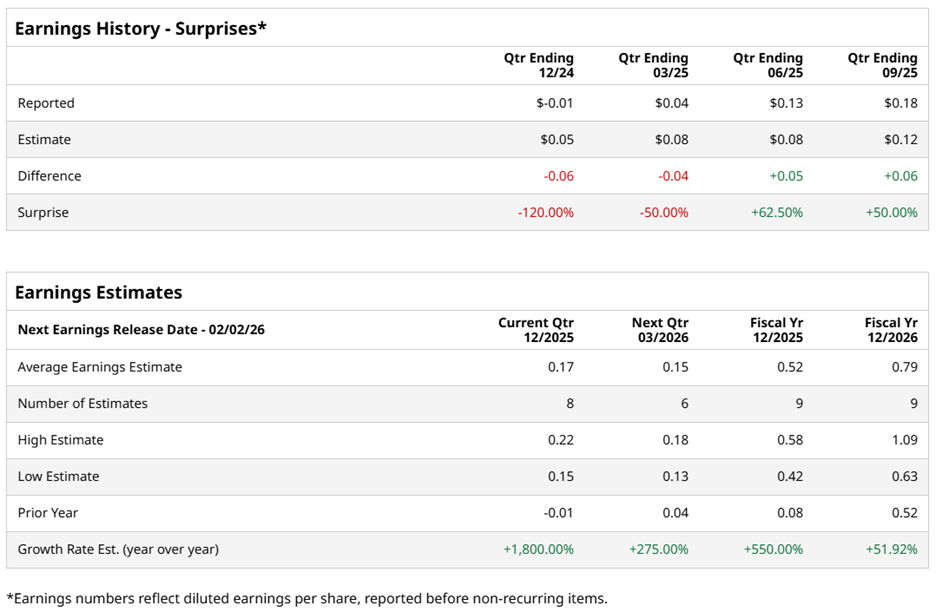

Attention now centers on Palantir’s Q4 fiscal 2025 earnings, scheduled for Monday, Feb. 2, after market close. Wall Street forecasts diluted EPS of $0.17, a 1,800% increase from last year’s $0.01 loss per share. However, the company has beaten EPS estimates in only two of the past four quarters.

The prior quarter set a high bar. On Nov. 3, 2025, the company posted its Q3 fiscal 2025 financial results, wherein Palantir posted revenue of $1.18 billion, up 62.8% year over year and well above the $1.09 billion analyst estimates. Adjusted EPS came in at $0.21, surpassing the Street’s expectations of $0.17.

Management credited this strength to rapid expansion in the U.S. commercial segment, where enterprise customers accelerated adoption of the Artificial Intelligence Platform. Markets initially applauded the results, but optimism faded quickly. Valuation concerns, combined with disclosure of a large options position betting against the stock, pushed PLTR stock down nearly 7.9% in the following session.

Despite near-term volatility, analysts expect earnings momentum to persist. They project diluted EPS for fiscal 2025 to rise 550% year over year to $0.52, followed by another 51.9% increase to $0.79 in fiscal 2026.

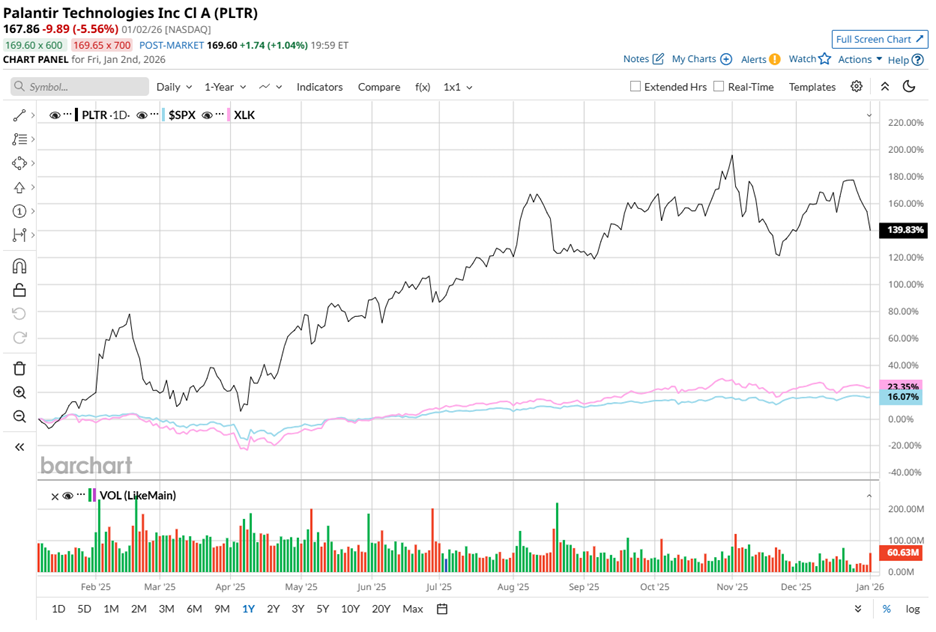

Stock performance already reflects lofty expectations. Over the past 52 weeks, PLTR stock surged 123.3%, while it gained 5.6% year-to-date (YTD). By comparison, the S&P 500 Index ($SPX) rose 16.9% over the same year and only marginally YTD, underscoring Palantir’s exceptional relative strength.

The contrast sharpens further against the State Street Technology Select Sector SPDR ETF (XLK). The ETF advanced 24.4% over the past 52 weeks and again only marginally YTD.

Momentum further strengthened on Dec. 10, 2025, as Palantir's shares climbed 3.3% after the U.S. Navy announced a landmark partnership with Palantir. The deal rolls out Foundry and AIP across the Maritime Industrial Base via ShipOS, authorizing up to $448 million. Strategically, this anchors Palantir deeper into defense infrastructure, reinforcing long-term revenue durability and mission-critical relevance.

Despite that validation, analysts continue to temper enthusiasm. Elevated valuation multiples and the sector's mixed performance have kept the consensus rating at “Hold,” unchanged for the past three months. Of 21 analysts, five recommend “Strong Buy,” 13 advise “Hold,” one suggests “Moderate Sell,” and two flag “Strong Sell.”

Even so, the average price target of $192.67 implies potential upside of 14.8%, while the Street-high target of $255 represents a gain of 51.9% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- CES 2026, Sector Rotation and Other Key Things to Watch this Week

- Tesla Stock Has Been Flat For 2 Months - How to Make a 3.2% Yield in One-Month Puts

- GOOGL Stock Rocked in 2025, But Is Google’s 2026 Forecast as Bright?

- The Saturday Spread: How Basketball Analytics May Help Extract Alpha (CPNG, DBX, BBY)