Xylem Inc. (XYL) is a leading water technology company that designs, manufactures, and services solutions for water transport, treatment, testing, and efficient use. It serves utilities, industrial, and residential customers worldwide, addressing challenges like clean water supply and wastewater management. Headquartered in Washington, D.C., Xylem drives global innovation in sustainable water solutions. The company has a market capitalization of $30.86 billion.

As Xylem faces weaker-than-expected demand for its water treatment equipment, which has led to subdued guidance, its stock has declined modestly over the past year. Over the past 52 weeks, the stock has declined 2.9%, while it is down 7.4% year-to-date (YTD). It had reached a 52-week high of $154.27 in October 2025, but is down 18.3% from that level.

The S&P 500 index ($SPX) is up 12.9% over the past 52 weeks but is down marginally YTD. Therefore, the stock has underperformed the broader market over these periods. Compared with Xylem’s own sector, we also observe underperformance. The State Street Industrial Select Sector SPDR ETF (XLI) has increased 25.4% over the past 52 weeks, while it has rallied 11.4% YTD.

On Feb. 10, Xylem reported growth in its fourth-quarter financials for fiscal 2025. The company’s revenue increased 6.3% year-over-year (YOY) to $2.40 billion, which was higher than the $2.38 billion that Street analysts had expected. Its adjusted EPS also grew 20.3% from the prior-year period to $1.42, meeting Street’s expectations. Nevertheless, the stock declined 8% intraday on Feb. 10, as Xylem issued modest organic revenue growth guidance for fiscal 2026.

For the current quarter, Street analysts expect Xylem’s profit to increase 5.8% YOY to $1.09 per diluted share, while for the current year, it is expected to increase 7.9% to $5.48 per diluted share, followed by a 9.7% growth to $6.01 per diluted share in the following year. The company also has a solid history of surpassing consensus estimates, topping them in three of the four trailing quarters and matching them in one instance.

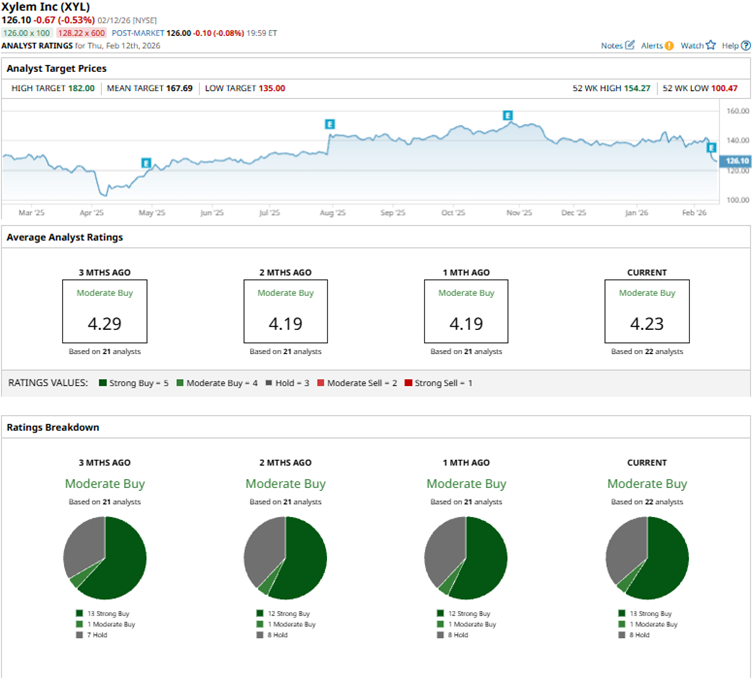

Among the 22 Wall Street analysts covering Xylem’s stock, the consensus is a “Moderate Buy.” That’s based on 13 “Strong Buy” ratings, one “Moderate Buy,” and eight “Holds.” The ratings configuration has become more bullish than a month ago, with the number of “Strong Buy” ratings increasing from 12 to 13.

Post the Q4 earnings release, Barclays analyst William Grippin maintained an “Overweight” rating but lowered the price target from $166 to $156, reflecting differing market conditions and expectations. Citigroup analyst Andrew Kaplowitz also maintained a “Buy” rating but cut the price target from $182 to $174.

Xylem’s mean price target of $167.69 indicates a 33% upside over current market prices.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart