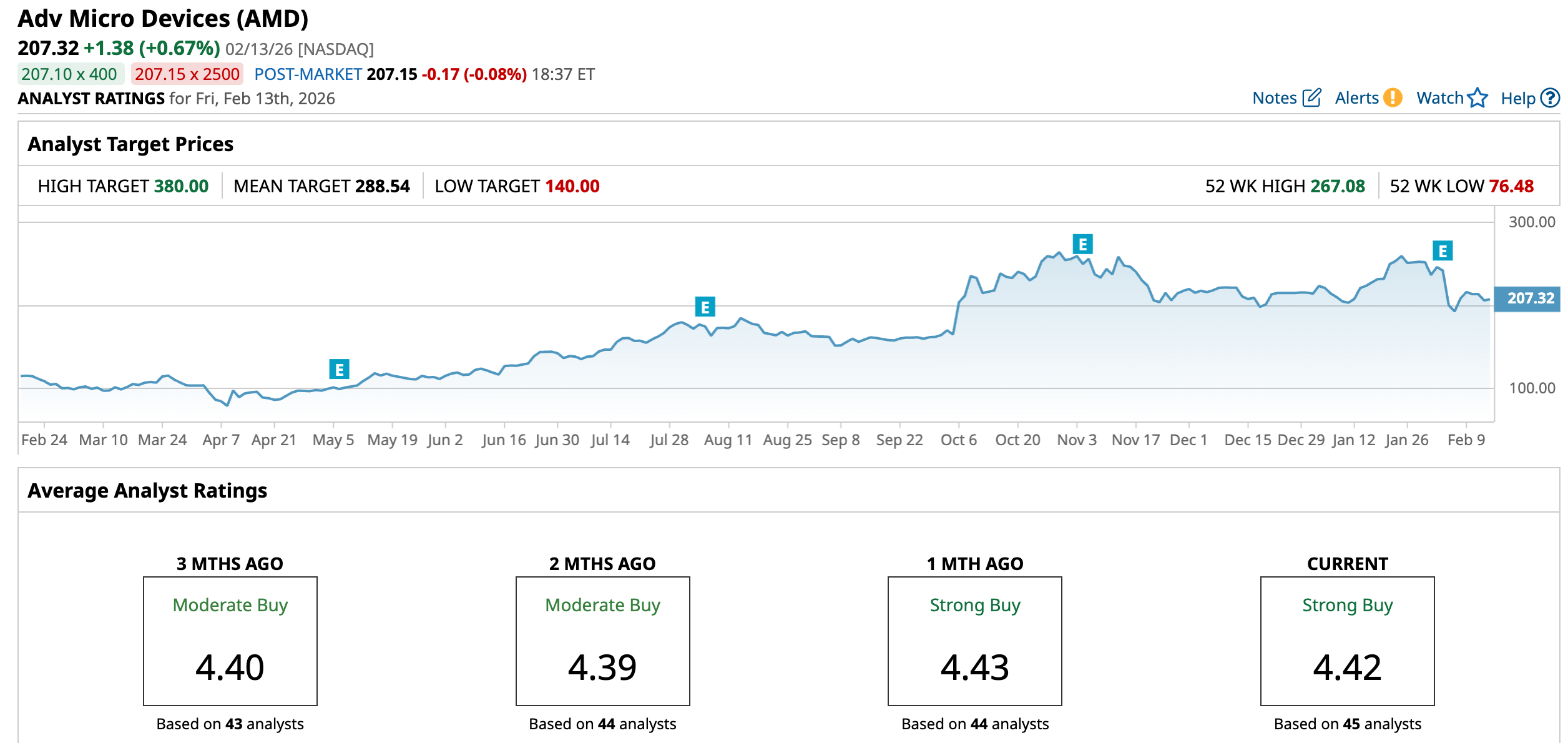

After a strong rally throughout 2025, Advanced Micro Devices (AMD) stock recently pulled back, sliding about 28.8% from its recent peak of $267.08. The stock came under pressure following its recent quarterly results.

Despite recent weakness, Wall Street’s outlook on AMD stock remains bullish. Analysts point to strong underlying demand for AMD’s high-performance computing and artificial intelligence (AI) products, which are expected to drive revenue and earnings growth in the coming quarters. These end markets continue to benefit from rising enterprise and data center spending, positioning the company well for longer-term growth.

Further, analysts’ average price target of $288.54 for AMD stock indicates an upside potential of 39% from its Feb. 13 closing price of $207.32.

AMD’s AI and Server Share Gain Sets the Stage for Solid 2026

AMD is well-positioned for strong growth in 2026, driven by rising demand in the data center and PC markets. The company has continued to gain share in server and PC processors while rapidly expanding its data center AI business. This momentum reflects growing adoption of Instinct accelerators and the ROCm software ecosystem.

AMD’s revenue rose 34% year-over-year (YOY) to $10.3 billion in the fourth quarter, supported by strong sales of EPYC server CPUs, Ryzen client processors, and Instinct AI accelerators. Profitability grew faster, with net income up 42% to $2.5 billion and free cash flow nearly doubling to $2.1 billion.

The Data Center segment remains the key growth driver for AMD. Segment revenue climbed 39% YOY to $5.4 billion, reflecting server CPU share gains and the rapid ramp of Instinct MI350 Series GPUs. Fifth-generation EPYC processors accounted for more than half of total server revenue during the quarter, signaling accelerating customer adoption.

Looking ahead, the demand for server CPUs remains favorable. Hyperscalers are scaling capacity to meet sustained growth in cloud services and AI workloads, while enterprises are upgrading aging data centers. These trends will drive further adoption of EPYC and share gains. Additionally, its expanding platform ecosystem, deepening software support, and aggressive go-to-market execution provide a solid base for future growth.

The company’s Data Center AI business is in a high-growth phase. Fourth-quarter Instinct GPU revenue reached a record level, supported by the higher shipment of the MI350 Series. Adoption broadened during the period, and the new product cycle should enable AMD to deepen relationships with existing cloud partners while onboarding additional enterprise and AI-focused customers.

Overall, AMD is witnessing significant demand for its products and solutions. Emerging and agentic AI workloads are driving incremental demand for powerful CPUs alongside accelerators, further benefiting EPYC.

Looking toward 2026, increased EPYC penetration in cloud and enterprise environments, broader adoption of Instinct accelerators, continued client processor share gains, and a recovery in the embedded segment create a sturdy foundation for top and bottom line growth.

Moreover, AMD projects its revenue to increase at a CAGR of over 35% in the next three to five years, alongside significant operating margin expansion and annual EPS surpassing $20 within that timeframe.

In summary, AMD’s accelerating revenue, margin expansion, and strong earnings growth could continue support its share price.

Is AMD Stock a Buy Now?

While AMD stock has pulled back from its recent highs, the company’s fundamentals remain solid. The acceleration in the adoption of EPYC processors and Instinct accelerators, along with expanding margins, positions AMD to sustain healthy double-digit earnings growth in 2026 and beyond.

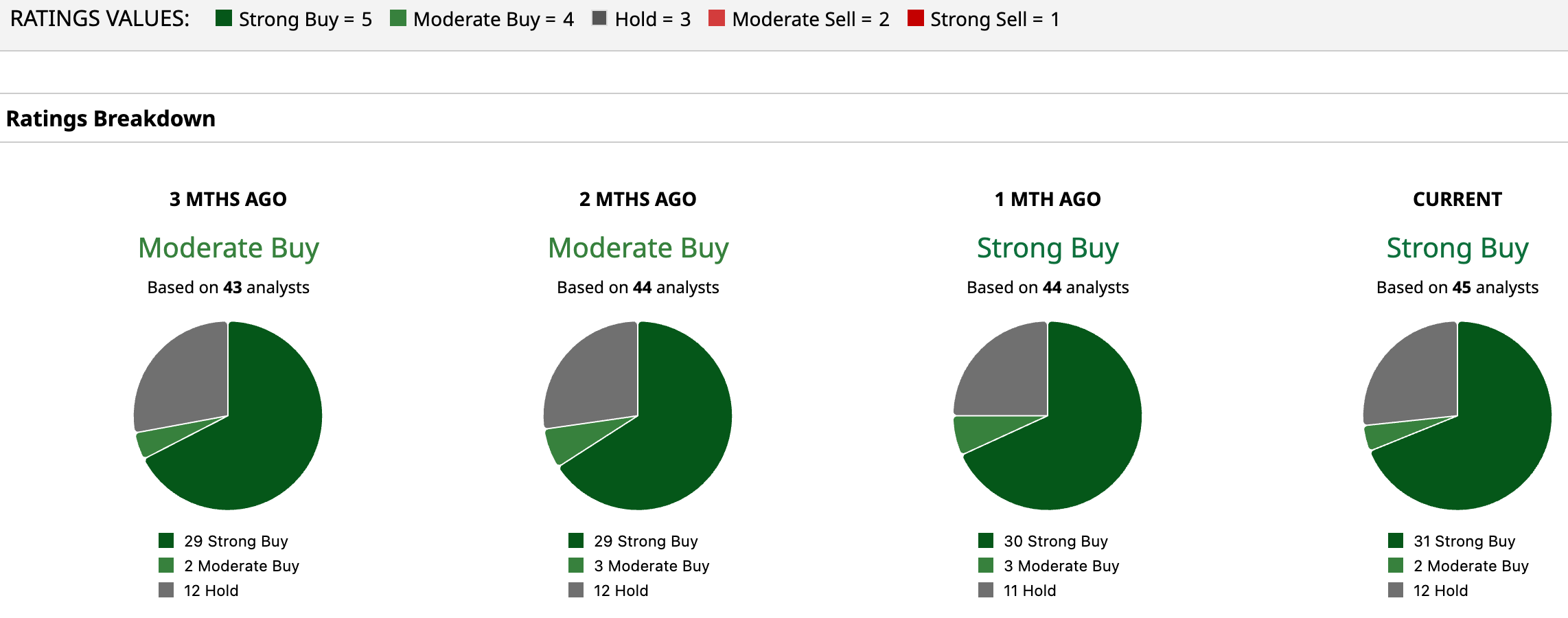

Wall Street analysts have a “Strong Buy” consensus rating on AMD stock. Further, its valuation indicates further upside. AMD stock currently trades forward price-to-earnings (P/E) ratio of 37.9x, which looks compelling relative to its earnings growth potential. Analysts expect its EPS to surge 72.2% in 2026, followed by 60% increase in 2027. Given this growth, the current valuation suggests continued upside in AMD stock.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart