It has been a busy time for tech investors as four of the “Magnificent 7” constituents — namely Microsoft (MSFT), Apple (AAPL), Meta Platforms (META), and Tesla (TSLA) — recently released their December quarter earnings. The market’s reaction to the earnings has been somber as investors question growing artificial intelligence (AI) capital expenditures.

Microsoft and Meta Platforms are two stories in contrast, though. While the former saw a double-digit dip on Jan. 29, Meta Platforms soared by a similar quantum and rose above $700. Notably, META stock previously fell below $700 following the company's third-quarter 2025 earnings release in October and traded below that level until Q4 earnings turned the tide.

With this recent momentum in mind, is $1,000 per share a reasonable expectation for META stock next? Let's take a closer look at the risks and opportunities investors should be aware of when it comes to Meta Platforms.

Meta's Monetization of WhatsApp and Threads Is a Major Opportunity

Meta’s digital ad business, which accounts for nearly all of its revenues, has been doing remarkably well. Looking ahead, Meta Platforms expects to monetize Threads and WhatsApp further. The company is expanding ads on Threads to all remaining countries and will gradually roll out ads on Status in WhatsApp. Paid messaging in WhatsApp is another growth driver for Meta, and the business is now running at an annual revenue run rate of over $2 billion.

Instagram Reels, which was launched to take on TikTok, continues to show strong traction as well. Meta said that, in Q4, total watch time on the platform rose 30% year-over-year (YOY) in the United States. The company plans to add more languages to the video dubbing feature on Instagram, which would help further drive engagement and, by extension, revenues. AI would also help Meta further increase the efficacy of ads by making them even more targeted.

Reality Labs Losses Are Expected to Peak in 2026

Meta Platforms' foray into hardware with AI glasses could potentially be another major growth avenue. However, Reality Labs continues to remain a drag on the company's finances. The segment posted an operating loss of over $6 billion in Q4. The segment also lost $19.1 billion last year, while cumulative losses since 2020 have topped $80 billion.

Reality Labs is now focusing on glasses and wearables after having virtually given up on the metaverse — the project after which Meta had renamed itself from Facebook in 2021. For 2026, Meta Platforms expects the segment’s losses to be “similar” to last year. Additionally, CEO Mark Zuckerberg said that Reality Labs' losses would “likely peak” this year.

Key Risks Investors Should Watch Out For

While Meta Platforms' revenues are growing at a brisk pace, the firm is also witnessing a steep rise in both operating expenses and capex. For 2026, Meta forecast total expenses to be between $162 billion and $169 billion. At the midpoint, the figure is 42% higher than last year. Meta’s 2026 expenses are expected to grow at a faster pace than its revenues, which would take a toll on margins. However, the company still expects its 2026 operating income in absolute dollar terms to be higher than the previous year. We see a similar trend across almost all other tech giants, which are seeing their expenses swell amid the burgeoning AI investments.

Meta expects its 2026 capex to be between $115 billion to $135 billion, which is significantly higher than last year's capex of $72.2 billion. For 2026, Meta is optimistic about meeting the capex requirements through internal accruals. However, the company touted the possibility of “prudent amounts of cost-efficient external financing” to maintain its net cash position. While the company did not provide a specific answer to this, it might struggle to generate enough free cash flows this year as it pours billions more into building AI infrastructure. Rising AI capex would put pressure on Meta's balance sheet, which is otherwise quite strong.

Another risk that Meta investors should watch out for is the clampdown on teens using social media. Australia has taken the lead and banned kids under the age of 16 from using social media platforms. France is next in line, with the country’s lawmakers approving a ban on social media for teens under the age of 15. The law is set to be effective in September 2026, and more countries — particularly in Europe — might take a similar stance.

Commenting on the clamor to bar children from social media, Meta Platforms CFO Susan Li said during the Q4 earnings call that the company is seeing “scrutiny on youth-related issues.” Li added that there are “a number of trials scheduled for this year in the U.S., which may ultimately result in a material loss.”

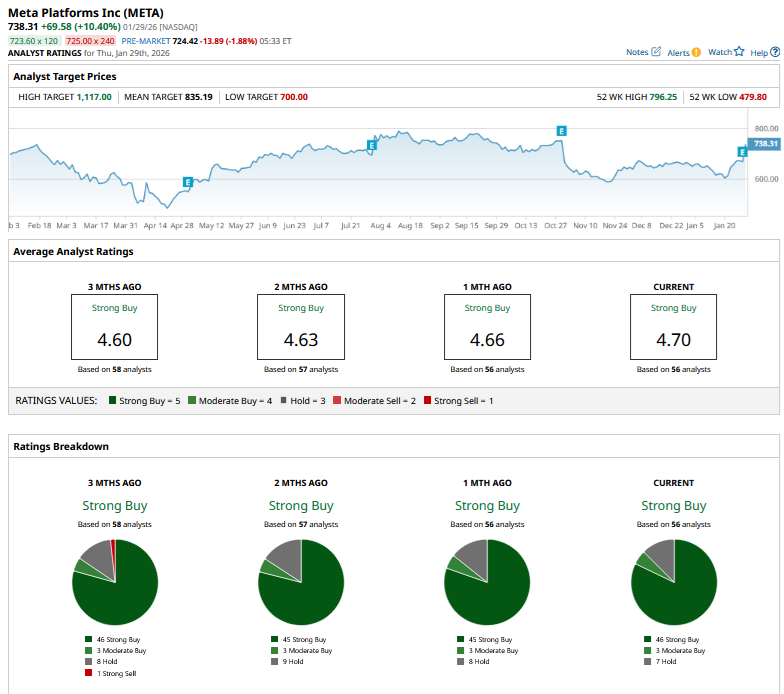

META Stock Forecast: Is It Headed to $1,000?

Wall Street analysts were generally impressed with Meta’s Q4 earnings and upbeat Q1 guidance, and several raised their price targets on META.

Among leading brokerages, Bank of America raised its target price from $810 to $885. Meanwhile, Cantor Fitzgerald raised its target to $860 from $750 while Jefferies analyst Brent Thill expects META stock to rise to $1,000.

Meta’s core (non-AI) business is doing remarkably well, and its revenues have grown by over 20% in the previous two years, with consensus estimates calling for similar growth this year. No other “Magnificent 7" stock — barring what else but Nvidia (NVDA) — has achieved this feat. However, Meta’s profitability is challenged, and the company’s 2026 per-share earnings are expected to be similar to 2025.

META stock trades at a forward price-to-earnings (P/E) multiple of 24 times, which is not unreasonable given the kind of topline growth the company brings to the table. The company’s profitability should improve in 2027 and beyond as Reality Labs losses (hopefully) narrow while overall expense growth moderates.

With all that in mind, I would bet on META hitting $1,000. If not this year, the stock may achieve that mark sometime early next year as the company continues to show remarkable resilience in its core business while continuing to monetize WhatsApp and Threads.

On the date of publication, Mohit Oberoi had a position in: META , MSFT , AAPL , NVDA , TSLA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart