Micron (MU) will release its second-quarter fiscal 2026 earnings on Wednesday, March 18. The announcement follows a big rally in MU stock. Over the past three months, MU has surged 92%. Moreover, the stock has climbed over 342% in the past year, outperforming most top technology stocks.

The big rally in Micron stock reflects significantly high demand for its advanced memory products. As artificial intelligence (AI) workloads expand, data centers and AI systems require high-bandwidth, high-capacity memory. This has driven strong growth in Micron’s DRAM, NAND, and high-bandwidth memory (HBM) revenue.

Supporting its investment case are tight supply dynamics, which have driven prices higher and bolstered Micron’s top and bottom lines. Notably, Micron has significantly expanded margins and is growing its bottom line at a solid pace, further driving its share price.

Thanks to a solid demand environment, option traders are positioning for a potentially large move following the Q2 earnings release. Contracts expiring on March 27 imply a move of roughly 11% in either direction. That expectation is notably higher than the company’s average post-earnings move of about 5.5% over the past four quarters, indicating that the market anticipates a stronger reaction to this report.

However, investors should take caution. Micron’s shares declined after earnings in three of the past four quarters, suggesting that even strong quarterly results may not translate into an immediate positive market reaction.

Micron Q2 Earnings: Here’s What to Expect

Micron’s management has maintained an optimistic outlook heading into the results. The company has guided for a significant acceleration in revenue growth, supported by strong end-market demand. At the same time, improving pricing dynamics in the memory market are expected to support margin expansion, which could translate into another period of strong earnings growth. These factors may continue to boost investor confidence in the stock, even after its substantial run-up.

Management remains optimistic, forecasting new highs across several key financial metrics, including revenue, margins, EPS, and free cash flow.

For the fiscal second quarter, Micron anticipates revenue of approximately $18.7 billion, an increase of more than 132% year-over-year (YoY). This would mark a significant acceleration compared with the 57% YoY revenue growth reported in the first quarter.

Profitability is also expected to improve significantly. Gross margin is projected to reach 68%, up from an adjusted gross margin of 37.9% a year earlier. EPS is forecasted at approximately $8.42, compared with adjusted EPS of $1.56 in the prior-year period. Analyst estimates are slightly higher, with second-quarter earnings expectations of about $8.52 per share, representing substantial YoY growth.

Supporting its financials is the ongoing momentum in the data center segment. Demand for server units remains robust, and Micron has positioned itself well in this segment through its portfolio of high-value products, including HBM, high-capacity server memory modules, and data-center solid-state drives (SSDs), to capture demand and accelerate growth.

Supply dynamics in the memory market are also playing a supportive role. Industry supply remains relatively tight, allowing manufacturers to maintain pricing discipline. Overall, Micron’s focus on higher-value products and solid pricing is helping the company expand margins while sustaining strong revenue growth.

Looking ahead, Micron has also finalized agreements covering price and volume for its entire calendar-year 2026 supply of HBM, including next-generation HBM4 products. Management expects the addressable market for HBM to expand rapidly in the coming years, positioning the company to benefit from long-term demand growth.

In short, Micron will likely deliver significant growth in Q2, which could support its share price rally.

Is MU Stock Still a Buy?

While Micron is likely to deliver significant growth and provide an upbeat outlook, its valuation suggests there may still be room for growth. MU stock trades at 12.4 times forward earnings, which appears attractive relative to its EPS growth trajectory.

Consensus projections indicate that Micron’s earnings could surge by about 349.4% in fiscal 2026, driven by high demand and increased pricing. Looking beyond 2026, growth is expected to remain robust, with an additional 42% increase in EPS for fiscal 2027.

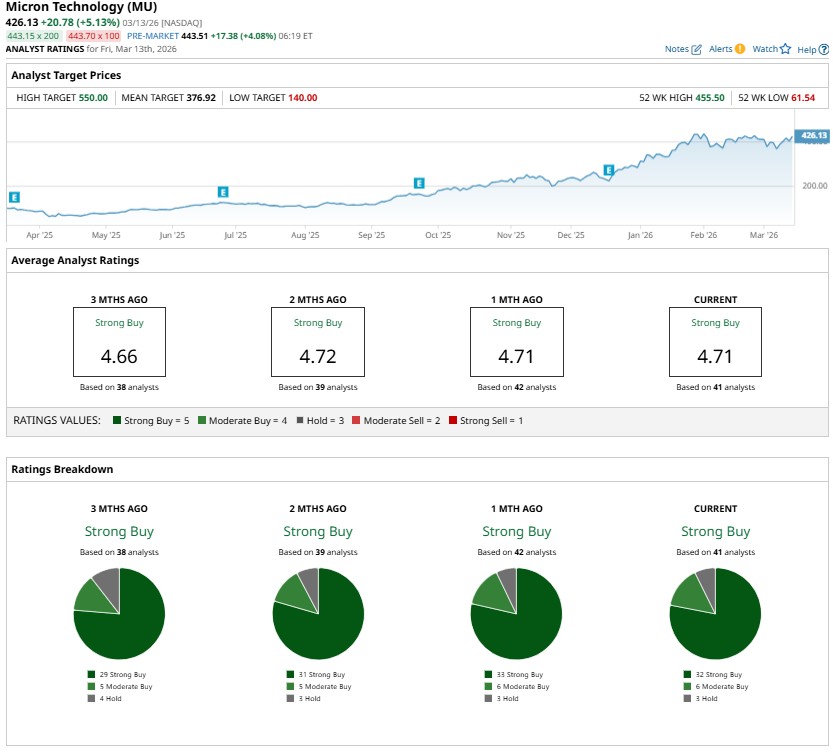

Most analysts covering Micron currently rate the stock a “Strong Buy,” reflecting confidence in the company’s ability to capitalize on rising demand for advanced memory technologies.

Overall, strong growth, a reasonable valuation, and a favorable analyst outlook make Micron’s investment case ahead of Q2 earnings.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart