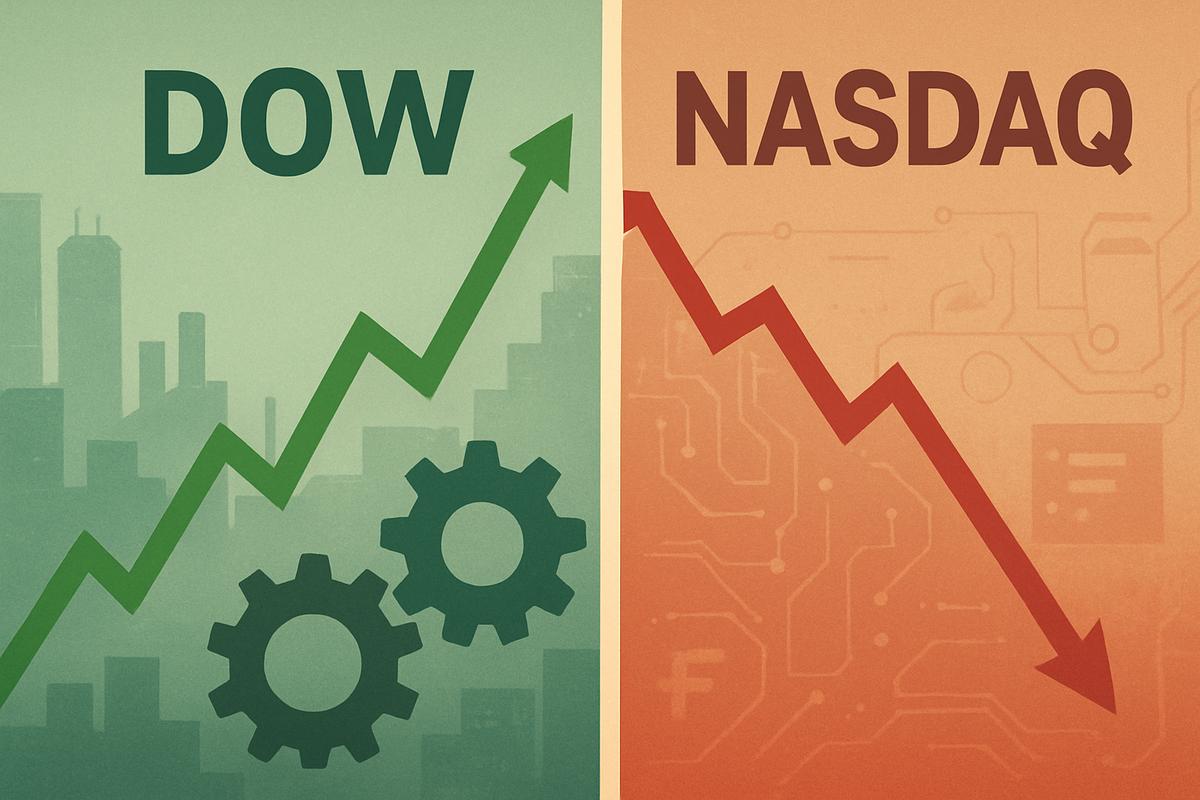

December 11, 2025 – The U.S. stock market is currently witnessing a striking and arguably unprecedented divergence, as the Dow Jones Industrial Average (DJIA) continues its ascent to record highs, while the tech-heavy Nasdaq Composite grapples with a significant slump. This "Great Divergence" signals a profound recalibration of investor sentiment, marking a distinct shift away from the high-flying growth stocks that have dominated the market for years and towards more traditional, value-oriented companies.

This market dynamic, unfolding as 2025 draws to a close, has immediate implications for investors, signaling a potential sector rotation and a re-evaluation of risk across portfolios. While the Dow's robust performance reflects confidence in established industries and a potential embrace of value, the Nasdaq's struggles highlight growing skepticism about the lofty valuations and immediate profitability of the technology and artificial intelligence (AI) sectors.

Unpacking the Market's Split Personality

The current market landscape is characterized by a stark contrast in performance between the two major indices. The Dow Jones Industrial Average (DJIA) has demonstrated remarkable strength, breaching the 48,000 mark in November 2025 and surging to a new all-time high of 48,564.65 on December 11, 2025. This impressive run includes 17 record highs for the year, with year-to-date gains exceeding 13%. This momentum has been buoyed by a rotation into "real economy" stocks, cyclicals, and small-cap companies, benefiting from recent Federal Reserve interest rate cuts.

In stark contrast, the Nasdaq Composite has entered a "tech slump" or "retreat." On December 11, 2025, the index fell by 0.7%, with Nasdaq futures dropping sharply by 1.5% earlier in the day. This downturn was significantly exacerbated by a disappointing earnings report from Oracle (NYSE: ORCL), which missed cloud revenue targets and announced a substantial $15 billion increase in data center spending. Oracle's shares plunged over 15%, dragging down other major AI-linked tech stocks such as Nvidia (NASDAQ: NVDA) and Broadcom (NASDAQ: AVGO). Despite a strong year overall for the Nasdaq, with a year-to-date return of 22.5% as of December 10, 2025, the recent pullback indicates heightened scrutiny of tech sector valuations and a demand for clearer pathways to profitability.

The timeline leading up to this moment includes a series of Federal Reserve interest rate cuts—the third of the year—bringing the key rate to a range of 3.5% to 3.75%. While these cuts generally provide a broad market lift, their impact is now being filtered through sector-specific considerations. Fed Chair Jerome Powell's comments, suggesting further rate hikes are unlikely and prioritizing the job market, have also shaped sentiment. The overall market environment is increasingly characterized by "instability," with rapid shifts in economic determinants affecting various sectors unevenly, leading to a "K-shaped" backdrop where some sectors thrive while others struggle.

Winners and Losers in the Shifting Sands

This significant market divergence is creating a clear divide between companies that are poised to benefit and those that face increasing headwinds. The rotation into value and cyclical stocks is proving advantageous for established businesses in traditional sectors, while the tech slump is primarily impacting growth-oriented companies, particularly those with high valuations or substantial exposure to the AI boom.

Companies Winning from the Rotation: The shift towards value and cyclicals, often bolstered by lower interest rates and a desire for stability, is benefiting several sectors. Financials are seeing strong gains, with companies like Goldman Sachs (NYSE: GS) performing well. Regional banks and Business Development Companies (BDCs) such as Ares Capital (NASDAQ: ARCC), Blue Owl Capital Corporation (NYSE: OBDC), and Hercules Capital (NYSE: HTGC) are also positioned to gain. Industrials, often considered "blue-chip" stocks, are showing resilience, with companies like General Electric (NYSE: GE), 3M Co. (NYSE: MMM), and Honeywell (NASDAQ: HON) being favored. Select Consumer Staples and Discretionary firms with strong fundamentals, such as Home Depot (NYSE: HD) and Visa (NYSE: V), are also seeing significant upticks. The Healthcare sector, with its defensive characteristics and growth opportunities, is attracting investors, exemplified by Stryker (NYSE: SYK). Furthermore, Housing-Related Companies like Carlisle Companies (NYSE: CSL) and Builders FirstSource (NYSE: BLDR) are expected to drive portfolio gains, alongside certain Energy stocks.

Companies Losing from Tech/AI Scrutiny: The tech slump is hitting growth-oriented companies hard, especially those whose valuations rely heavily on future AI potential. Oracle (NYSE: ORCL) experienced a significant plunge (over 13-14%) after its disappointing earnings, becoming a "bellwether for the AI investment boom" and intensifying fears of an "AI bubble." AI-related chipmakers are also experiencing weakness; Nvidia (NASDAQ: NVDA), Advanced Micro Devices (NASDAQ: AMD), and Broadcom (NASDAQ: AVGO) all saw declines following Oracle's report and renewed valuation concerns. The sell-off has not been isolated, impacting broader megacap tech firms such as Apple (NASDAQ: AAPL), Amazon (NASDAQ: AMZN), Alphabet (NASDAQ: GOOGL), Meta Platforms (NASDAQ: META), and Tesla (NASDAQ: TSLA), all of which were in the red.

A Broader Economic Reassessment

The divergence between the Dow and Nasdaq is more than just a market anomaly; it reflects a fundamental reassessment of market health and broader economic trends. This scenario highlights a significant sector rotation, where market leadership is shifting away from the technology sector and towards other parts of the economy, particularly value and cyclical stocks. This trend has been building throughout 2024 and 2025, expanding beyond the "Magnificent Seven" mega-cap tech stocks. A key factor in the tech slump is an "AI reality check," as investors scrutinize the immediate profitability and returns of substantial capital deployed in AI, demanding more than just aspirational growth narratives.

The impact of interest rates also plays a crucial role. While the Federal Reserve has implemented rate cuts, continued high or rising interest rates generally pressure tech valuations, as growth stocks are "long-duration" assets whose valuations heavily rely on future earnings potential. Higher borrowing costs make it more expensive for tech firms to fund innovation. Furthermore, the tech sector has seen significant global layoffs, impacting economic growth, consumer spending, and commercial real estate, particularly in tech hubs. This downturn forces tech companies to prioritize cost control over rapid innovation. The benefits of AI adoption are also largely concentrated among a few dominant large technology companies, potentially creating structural imbalances and uneven economic distribution.

The ripple effects of this divergence are widespread. The market is likely to experience continued volatility and ongoing sector rotations, potentially leading to a prolonged period where value and cyclical stocks consistently outperform growth stocks. A sustained tech slump could dampen overall economic growth and consumer spending. Investors are increasingly encouraged to diversify portfolios beyond solely tech, with a balanced approach becoming crucial. The labor market may also see shifts, with continued tech layoffs and new opportunities in AI-related fields. Regulatory scrutiny on "Big Tech" is intensifying globally, with concerns over market concentration and antitrust issues, particularly within the nascent generative AI market. Governments are actively pursuing regulations to rein in digital giants and restore fair competition.

Historically, market divergences between growth and value, or between different indices, are not new. The bursting of the dot-com bubble in the early 2000s, which saw the Nasdaq Composite decline almost 80%, serves as a prominent precedent for a shift away from overvalued tech. While less extreme divergences are common, some analysts note that a simultaneous record high for the Dow and a significant slump for the Nasdaq could be "unprecedented" since the Nasdaq's inception in 1971, highlighting the unique combination of factors at play in December 2025.

Navigating the Path Ahead

The coming months will be critical in determining the trajectory of this market divergence. In the short term, through mid-2026, continued volatility and sector rotation are highly probable. "Smart money" will likely continue to rebalance portfolios, moving away from growth-oriented equities towards value and cyclical stocks. The tech sector could face a more severe correction if AI investment concerns deepen, or a "flight to quality" within tech, favoring established giants with diversified revenue streams. Conversely, sectors like financial services, energy, industrials, healthcare, and consumer staples are expected to see continued demand. The Federal Reserve's future interest rate decisions will remain a critical factor, with any indication of rates staying "higher for longer" potentially fueling further value outperformance.

In the long term, historical patterns suggest that divergences between indices tend to converge, "regressing to the mean." While growth stocks have dominated for the past decade, historical data indicates that value stocks have long-term potential during market reversals, with some forecasts suggesting value could outperform growth by a significant margin over the next five to ten years. A durable resurgence of value shares may be primed if interest rates remain elevated. While technological innovation, including AI, remains fundamental to future economic growth, investors will likely apply greater scrutiny to valuations and demand clearer pathways to profitability from tech companies. Diversification will be a core strategy, with a well-balanced portfolio crucial for navigating varying economic conditions.

Strategic pivots will be essential for investors. This includes employing sector rotation strategies, focusing on value investing opportunities in overlooked companies with strong fundamentals, and maintaining a balanced portfolio approach that combines growth and defensive stocks. Risk management, through thorough research, informed decision-making, and regular portfolio rebalancing, will be paramount. International diversification may also offer valuation opportunities and reduce risk.

Opportunities will emerge for value investors to find fundamentally strong companies in traditional sectors that may be undervalued. Defensive sectors like consumer staples, healthcare, and utilities could offer stability. Dividend-paying stocks from established industries may become more attractive. Agile investors can use tactical allocation to capture short-term opportunities. However, challenges include continued market volatility, concentration risk if investors remain overly exposed to a few high-valuation tech names, persistent inflationary pressures, and the potential for an economic slowdown.

A New Chapter for the Market

The Dow's record highs juxtaposed against the Nasdaq's tech slump mark a significant turning point in the financial markets of December 2025. This "Great Divergence" is a powerful indicator of a fundamental recalibration in investor sentiment, shifting focus from speculative growth to proven value and profitability. It underscores a market that is becoming more discerning, demanding concrete returns and sustainable growth beyond narrative-driven enthusiasm, particularly in the tech sector.

Moving forward, the market will likely be characterized by continued volatility and dynamic sector rotations. Investors should prepare for an environment where traditional industries may regain leadership, and a more balanced, diversified approach to investing becomes not just advisable, but imperative. The long-term implications could include a durable resurgence of value investing and a more critical assessment of technological innovations, where genuine profitability is prioritized over aspirational growth. What investors should watch for in the coming months are further signals from the Federal Reserve regarding interest rates, the earnings reports of key tech and industrial companies, and any shifts in geopolitical and economic stability that could influence sector performance.

This content is intended for informational purposes only and is not financial advice