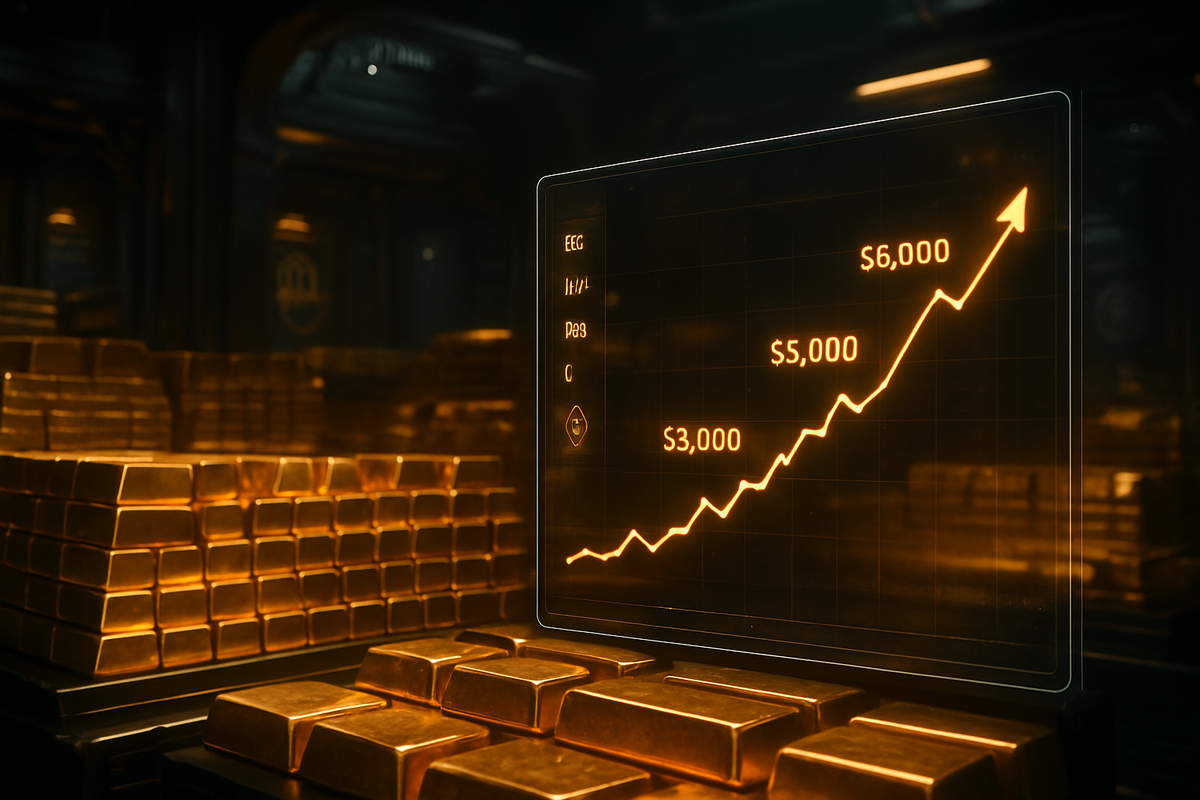

As of March 12, 2026, the global financial landscape has witnessed a tectonic shift in the valuation of precious metals, driven not by retail speculation, but by the relentless "base load demand" of the world’s most powerful central banks. Over the past two years, gold has shed its reputation as a mere defensive asset, evolving into a strategic cornerstone for sovereign reserves. This structural transition has seen prices shatter the $3,000 per ounce barrier in early 2025, with major institutional analysts now forecasting a trajectory toward $6,000 as the "de-dollarization" trend accelerates.

The immediate implication of this trend is the creation of a "hard floor" under gold prices. Unlike the volatile flows of the 2010s, the current market is supported by price-insensitive sovereign buyers who view gold as a hedge against currency debasement and geopolitical sanctions. This persistent buying pressure has decoupled gold from its traditional inverse relationship with real yields, allowing the metal to maintain record valuations even in an environment of elevated interest rates. For the broader market, this signals a "Great Re-Rating" of hard assets, forcing institutional investors to recalibrate their portfolios in favor of commodity-backed security.

The Era of Sovereign Accumulation

The narrative of the current gold bull market began in earnest in 2024, a year that saw central banks purchase a staggering 1,086 tonnes of gold. This was the third consecutive year of demand exceeding the 1,000-tonne mark, a level previously thought to be an anomaly. Leading this charge were the People’s Bank of China (PBoC) and the Central Bank of Russia (CBR), both of which have transitioned from periodic buyers to permanent accumulators. As of March 2026, the PBoC has extended its official buying streak to 16 consecutive months, bringing its reported holdings to 2,308 tonnes. However, industry experts suggest the "shadow" reserves of China, facilitated through state-owned banks and the Shanghai Gold Exchange, could actually range between 3,000 and 5,000 tonnes.

Russia’s strategy has been equally transformative, albeit focused on domestic security. Following the freezing of its foreign exchange assets in 2022, the CBR completed a total repatriation of its gold reserves, ensuring that 100% of its holdings are stored within its own borders. While Russia did sell approximately 230 tonnes in late 2025 to manage budget deficits and support the ruble, it remains the world’s fifth-largest holder. This "base load" demand—a constant stream of buying regardless of price—has effectively neutralized traditional selling pressure from Western institutional desks, creating a supply-demand imbalance that keeps prices afloat even during periods of sideways market trading.

Mining Giants and ETF Providers Reaping the Rewards

The primary beneficiaries of this sustained gold demand are the global mining leaders and the financial institutions managing gold-backed instruments. Newmont (NYSE: NEM) and Barrick Gold (NYSE: GOLD) have seen their margins expand significantly as the spot price of gold decoupled from production costs. These companies, which struggled with inflationary pressures in 2022 and 2023, are now generating record free cash flow. Similarly, royalty and streaming firms like Franco-Nevada (NYSE: FNV) have proven to be major winners, as they benefit from higher prices without the direct operational risks of mining, providing a high-leverage play on the central bank-driven price floor.

In the financial services sector, the resurgence of Western investor interest has breathed new life into gold ETFs. In 2025, global gold ETFs recorded an unprecedented $89 billion in inflows, a reversal of the outflows seen in previous years. State Street (NYSE: STT), which manages the SPDR Gold Shares (NYSEARCA: GLD), saw its flagship fund attract over $12.9 billion in net new assets in a single year. BlackRock (NYSE: BLK) has seen similar success with its iShares Gold Trust (NYSEARCA: IAU), which recorded $8.6 billion in inflows. For these asset managers, the return of gold as a "must-have" asset class for diversified portfolios has resulted in a significant boost to assets under management (AUM) and fee revenue.

A Structural Shift in Global Reserve Management

The wider significance of this event cannot be overstated; it marks the end of the post-Bretton Woods era of unquestioned U.S. dollar dominance. The "base load" demand from central banks is a direct response to the weaponization of the dollar and the ballooning U.S. national debt. By diversifying into gold, central banks are effectively opting out of the "counterparty risk" inherent in fiat currencies. This trend is no longer limited to the BRICS nations; emerging economies like Malaysia and Uzbekistan have joined the fray, signaling a broader movement toward "multipolar" reserve management.

Historically, gold was viewed as a "zero-yield" liability during times of high interest rates. However, the 2024-2026 period has shattered this precedent. Gold’s ability to hit record highs while the Federal Reserve maintained a "higher-for-longer" stance suggests that the market now values gold’s "solvency" more than its "yield." This shift mirrors the inflationary era of the 1970s but on a much larger scale, as the volume of global debt today is exponentially higher. The ripple effect is being felt in the currency markets, where the correlation between the dollar and gold has weakened, forcing a re-evaluation of how "safe haven" assets are defined in the 21st century.

The Path to $6,000: Short-Term Pain for Long-Term Gain

Looking ahead to the remainder of 2026 and into 2027, the market is bracing for a potential "melt-up" scenario. While central bank demand provides the floor, the "ceiling" is being pushed higher by a convergence of ETF inflows and retail demand. Major financial institutions have adjusted their targets accordingly; Goldman Sachs has set a 2026 price target of $5,400, while J.P. Morgan has gone even further, suggesting a "structural rebasing" could push gold to $6,300 per ounce. These forecasts are predicated on the assumption that central banks will continue to purchase at least 700 to 900 tonnes annually, combined with a weakening of the U.S. fiscal position.

The short-term challenge for the market will be the "price sensitivity" of retail consumers, particularly in India and China, who may pull back as gold approaches $4,000. However, strategic pivots by central banks—such as China’s move to turn Hong Kong into a global gold hub—suggest that the infrastructure for a gold-backed trade system is being built in real-time. Investors should prepare for a period where "volatility" is replaced by "consistent upward drift," as the scarcity of physical gold meets the infinite demand of central bank printing presses.

Summary and Investor Takeaways

The role of central bank demand in supporting gold prices through 2024 and 2026 has fundamentally changed the nature of the precious metals market. By providing a "base load" of demand, nations like China and Russia have protected gold from traditional market downturns and paved the way for a historic bull run. As gold stabilizes above $3,000 and eyes the $6,000 mark, the era of gold as a "fringe" asset is officially over. It has reclaimed its throne as the ultimate arbiter of value in an uncertain world.

Moving forward, investors should watch for two key indicators: the monthly reserve reports from the PBoC and the net inflow data for major ETFs like GLD and IAU. If central bank buying remains above 750 tonnes for 2026, the $5,000+ price targets from major banks will likely move from "possibility" to "inevitability." The "Great Re-Rating" is underway, and for those holding physical gold or mining equities, the coming quarters promise to be some of the most lucrative in financial history.

This content is intended for informational purposes only and is not financial advice.