Carvana has been on fire lately. In the past six months alone, the company’s stock price has rocketed 97%, reaching $243.09 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now still a good time to buy CVNA? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Does Carvana Spark Debate?

Known for its glass tower car vending machines, Carvana (NYSE: CVNA) provides a convenient automotive shopping experience by offering an online platform for buying and selling used cars.

Two Things to Like:

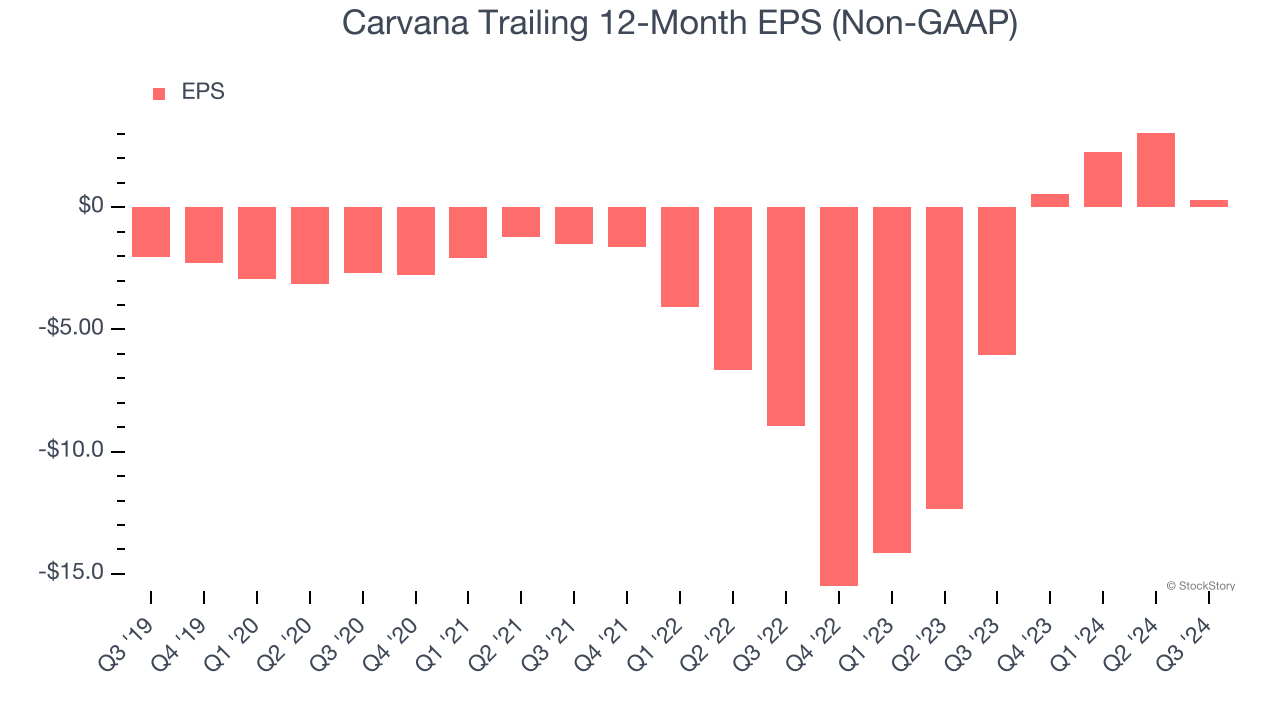

1. Outstanding Long-Term EPS Growth

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Carvana’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

2. Increasing Free Cash Flow Margin Juices Financials

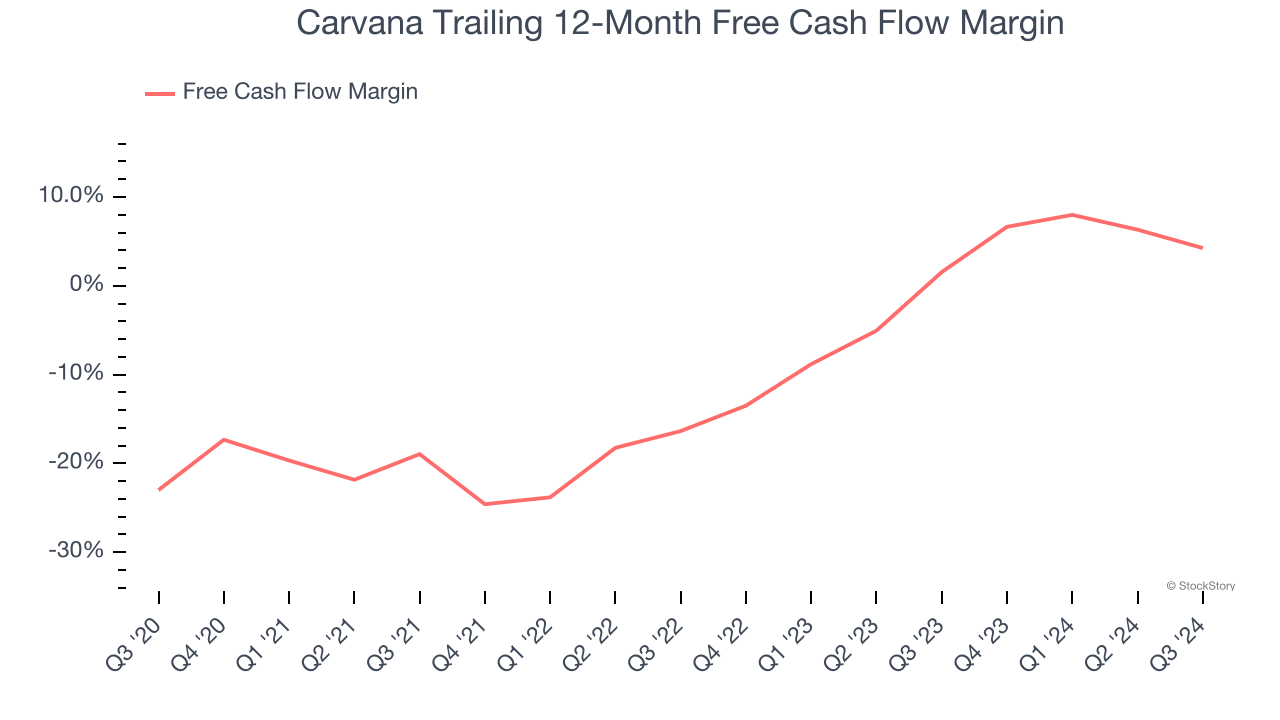

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Carvana’s margin expanded by 23.2 percentage points over the last few years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose by more than its operating profitability. Carvana’s free cash flow margin for the trailing 12 months was 4.3%.

One Reason to be Careful:

Declining Retail Units Sold Reflect Product Weakness

As an online retailer, Carvana generates revenue growth by expanding its number of users and the average order size in dollars.

Carvana struggled to engage its audience over the last two years as its retail units sold have declined by 23% annually. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Carvana wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

Final Judgment

Carvana’s merits more than compensate for its flaws, and with the recent surge, the stock trades at 22.5× forward EV-to-EBITDA (or $243.09 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Carvana

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.