Dayforce has had an impressive run over the past six months as its shares have beaten the S&P 500 by 23.9%. The stock now trades at $70, marking a 36.5% gain. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Dayforce, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

We’re glad investors have benefited from the price increase, but we're swiping left on Dayforce for now. Here are two reasons why you should be careful with DAY and a stock we'd rather own.

Why Is Dayforce Not Exciting?

Founded in 1992 as Ceridian, an outsourced payroll processor and transformed after the 2012 acquisition of Dayforce, Dayforce (NYSE: DAY) is a provider of cloud based payroll and HR software targeted at mid-sized businesses.

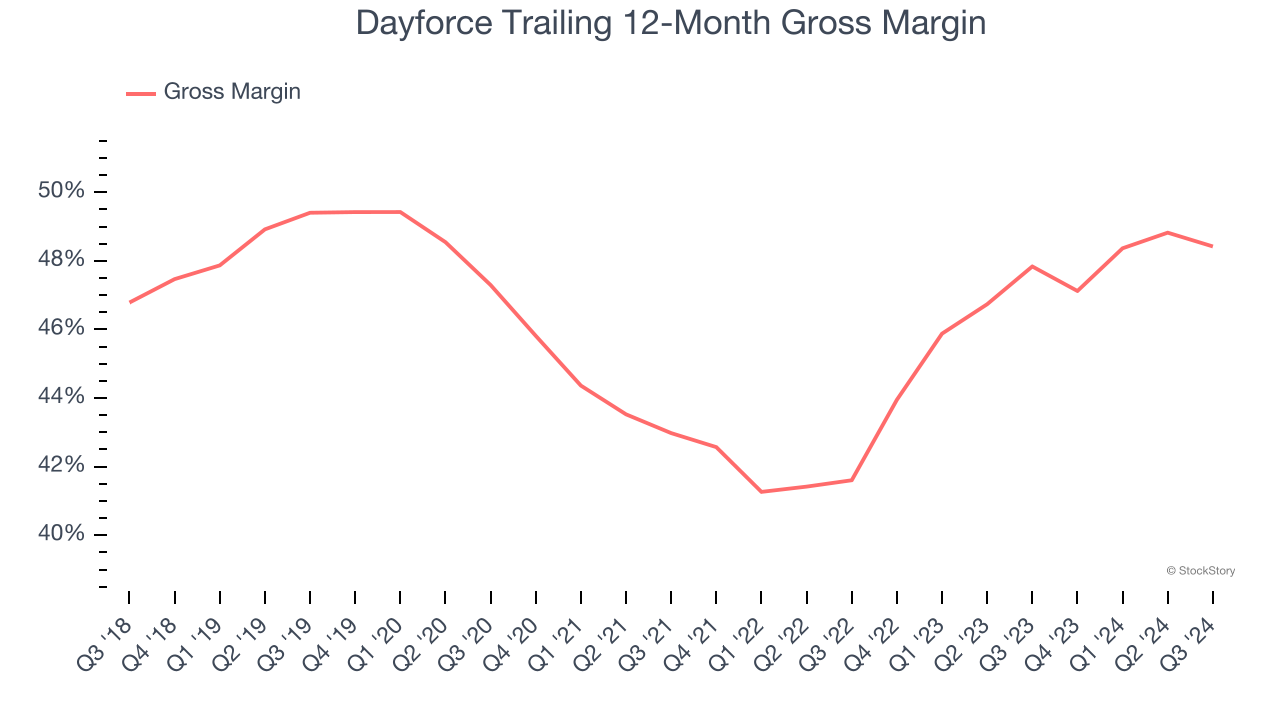

1. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Dayforce, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Dayforce’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 48.4% gross margin over the last year. Said differently, Dayforce had to pay a chunky $51.58 to its service providers for every $100 in revenue.

2. Free Cash Flow Projections Disappoint

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts’ consensus estimates show they’re expecting Dayforce’s free cash flow margin of 10.7% for the last 12 months to remain the same.

Final Judgment

Dayforce isn’t a terrible business, but it doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 5.9× forward price-to-sales (or $70 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of Dayforce

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.