Titan International has been treading water for the past six months, recording a small return of 1.9% while holding steady at $8.40. The stock also fell short of the S&P 500’s 12.6% gain during that period.

Is there a buying opportunity in Titan International, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

We're sitting this one out for now. Here are three reasons why we avoid TWI and a stock we'd rather own.

Why Is Titan International Not Exciting?

Acquiring Goodyear’s farm tire business in 2005, Titan (NSYE:TWI) is a manufacturer and supplier of wheels, tires, and undercarriages used in off-highway vehicles such as construction vehicles.

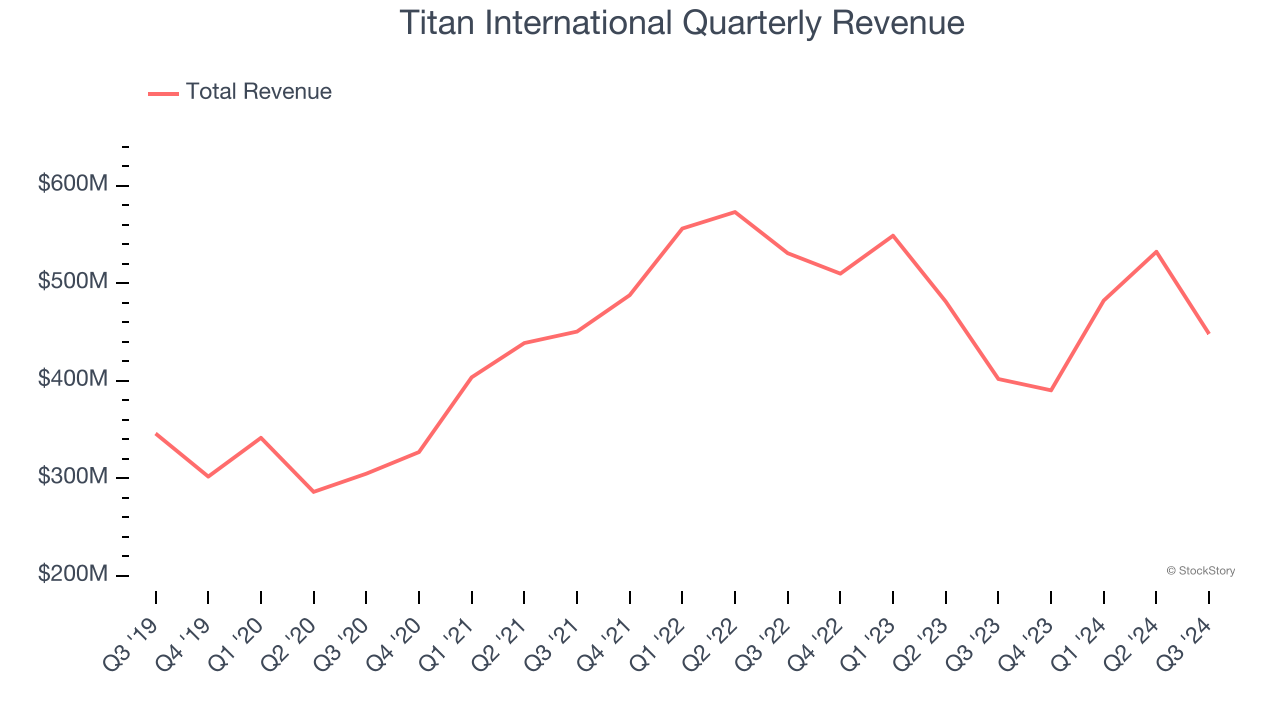

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Titan International’s 4.2% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the industrials sector.

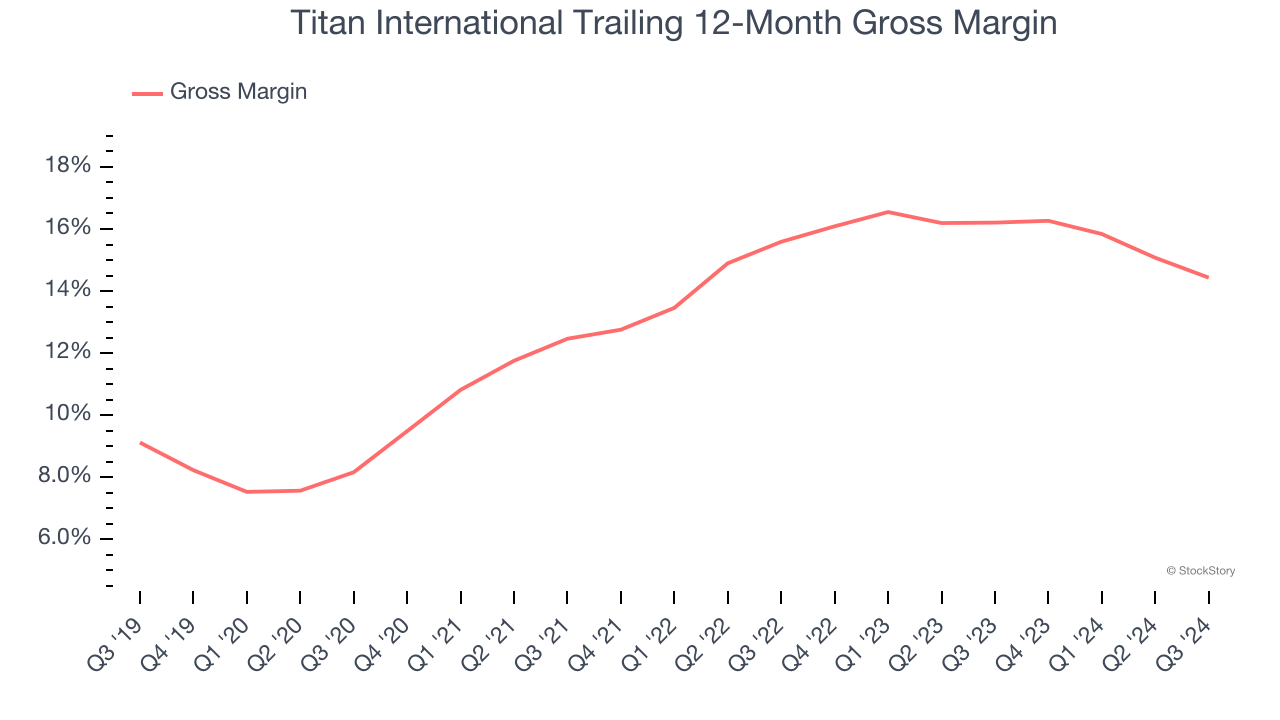

2. Low Gross Margin Reveals Weak Structural Profitability

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Titan International has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 13.9% gross margin over the last five years. That means Titan International paid its suppliers a lot of money ($86.14 for every $100 in revenue) to run its business.

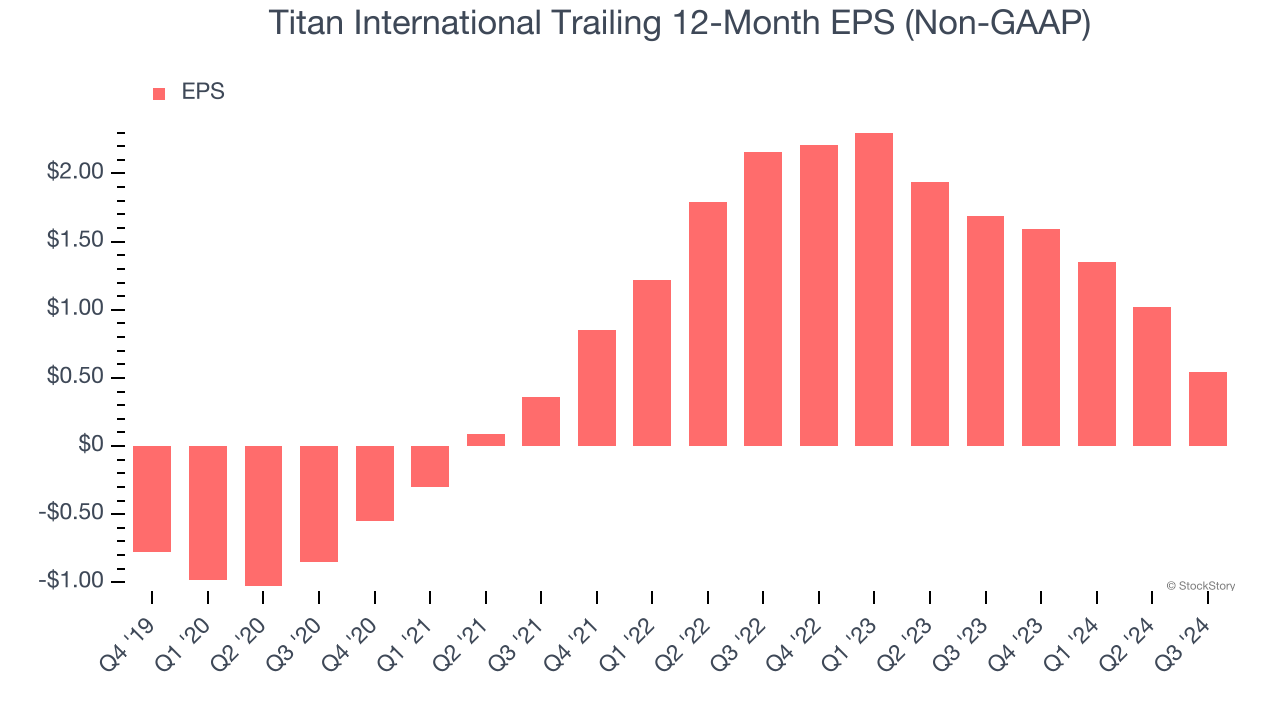

3. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for Titan International, its EPS declined by more than its revenue over the last two years, dropping 50%. This tells us the company struggled to adjust to shrinking demand.

Final Judgment

Titan International’s business quality ultimately falls short of our standards. With its shares underperforming the market lately, the stock trades at 21.3× forward price-to-earnings (or $8.40 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of our top digital advertising picks.

Stocks We Like More Than Titan International

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.