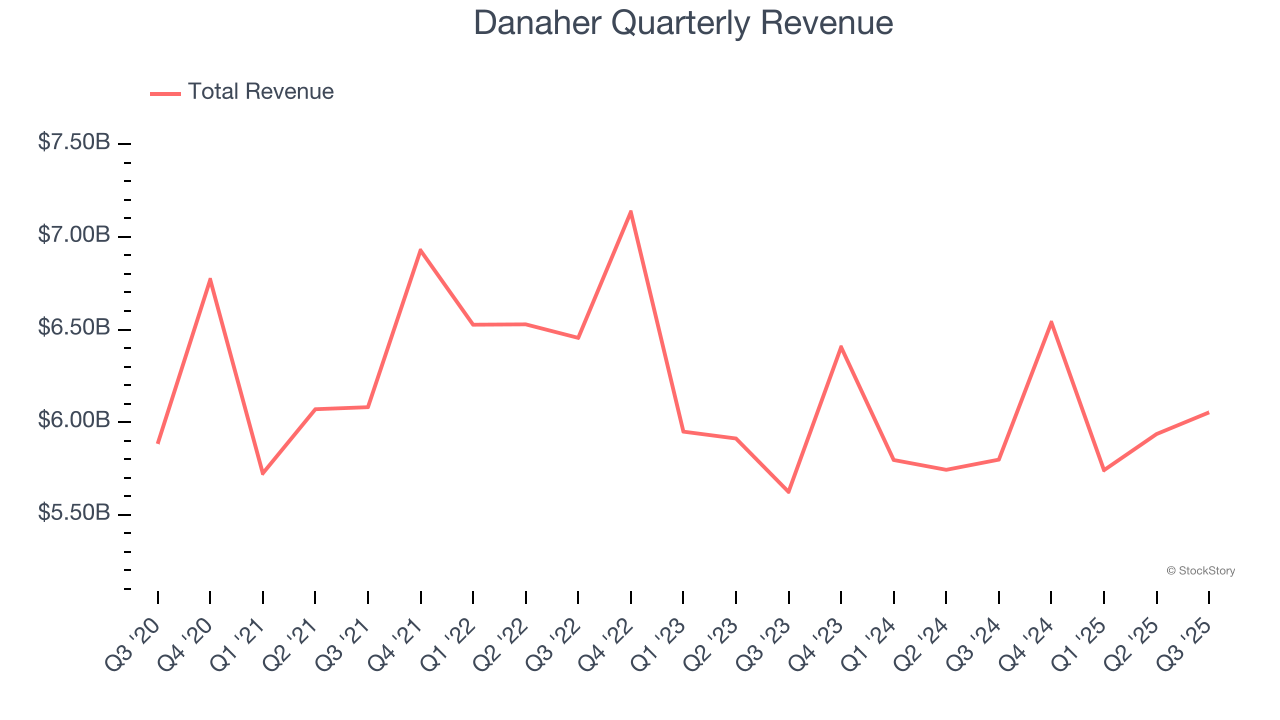

Diversified science and technology company Danaher (NYSE: DHR) reported revenue ahead of Wall Street’s expectations in Q3 CY2025, with sales up 4.4% year on year to $6.05 billion. On the other hand, next quarter’s revenue guidance of $6.70 billion was less impressive, coming in 4.7% below analysts’ estimates. Its non-GAAP profit of $1.89 per share was 9.8% above analysts’ consensus estimates.

Is now the time to buy Danaher? Find out by accessing our full research report, it’s free for active Edge members.

Danaher (DHR) Q3 CY2025 Highlights:

- Revenue: $6.05 billion vs analyst estimates of $6.01 billion (4.4% year-on-year growth, 0.8% beat)

- Adjusted EPS: $1.89 vs analyst estimates of $1.72 (9.8% beat)

- Revenue Guidance for Q4 CY2025 is $6.70 billion at the midpoint, below analyst estimates of $7.03 billion

- Management reiterated its full-year Adjusted EPS guidance of $7.75 at the midpoint

- Operating Margin: 19.1%, up from 16.5% in the same quarter last year

- Free Cash Flow Margin: 22.6%, up from 21% in the same quarter last year

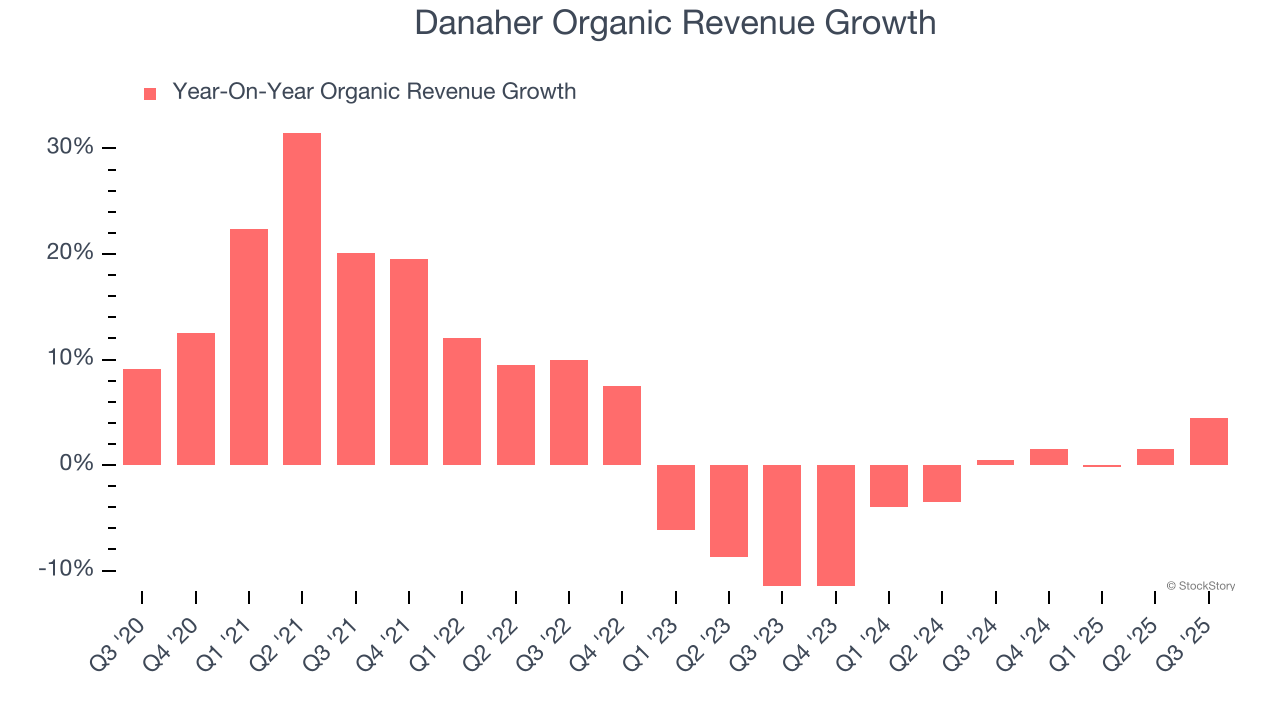

- Organic Revenue rose 4.5% year on year vs analyst estimates of 2.2% growth (229.3 basis point beat)

- Market Capitalization: $149.2 billion

Rainer M. Blair, President and Chief Executive Officer, stated, "We are encouraged by our third quarter results. DBS-driven execution paired with continued momentum in our bioprocessing business and better-than-anticipated respiratory revenue at Cepheid enabled us to exceed our revenue, earnings and cash flow expectations."

Company Overview

Born from a real estate investment trust that transformed into a manufacturing powerhouse, Danaher (NYSE: DHR) is a global science and technology company that provides specialized equipment, software, and services for biotechnology, life sciences, and diagnostics.

Revenue Growth

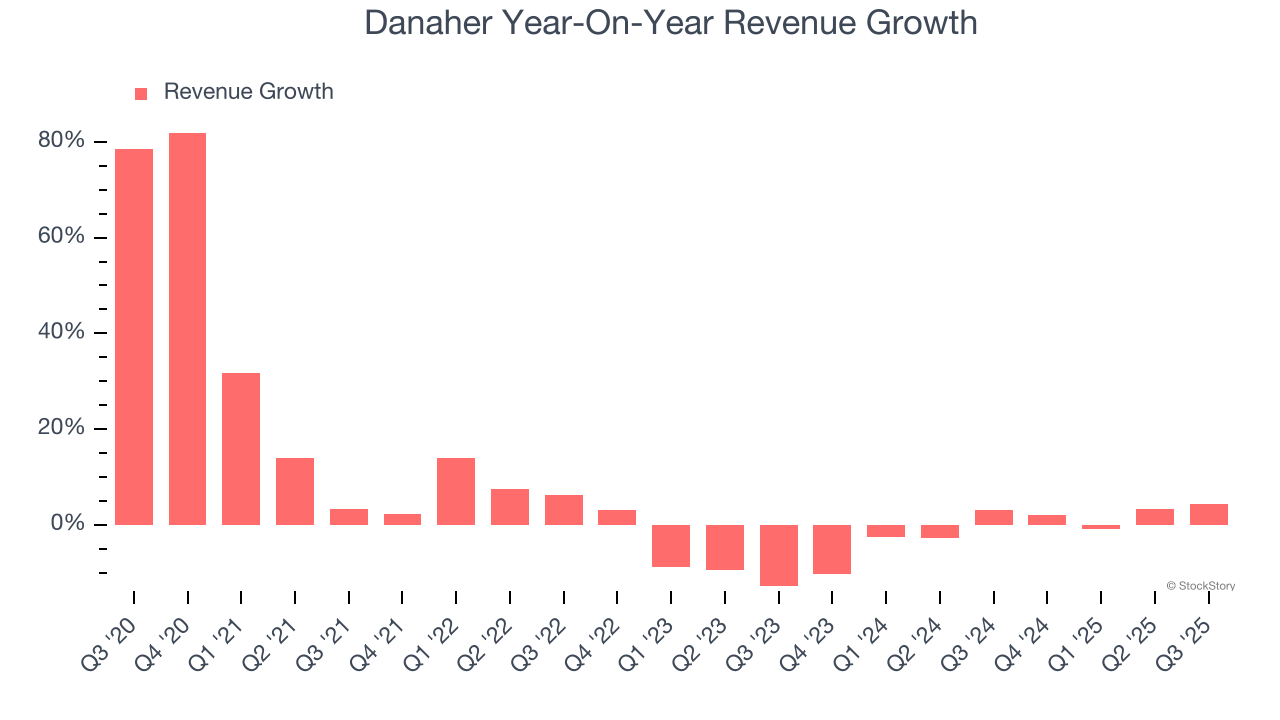

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Danaher’s sales grew at a mediocre 4.7% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Danaher’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Danaher’s organic revenue averaged 1.4% year-on-year declines. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Danaher reported modest year-on-year revenue growth of 4.4% but beat Wall Street’s estimates by 0.8%. Company management is currently guiding for a 2.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.6% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and suggests its newer products and services will fuel better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

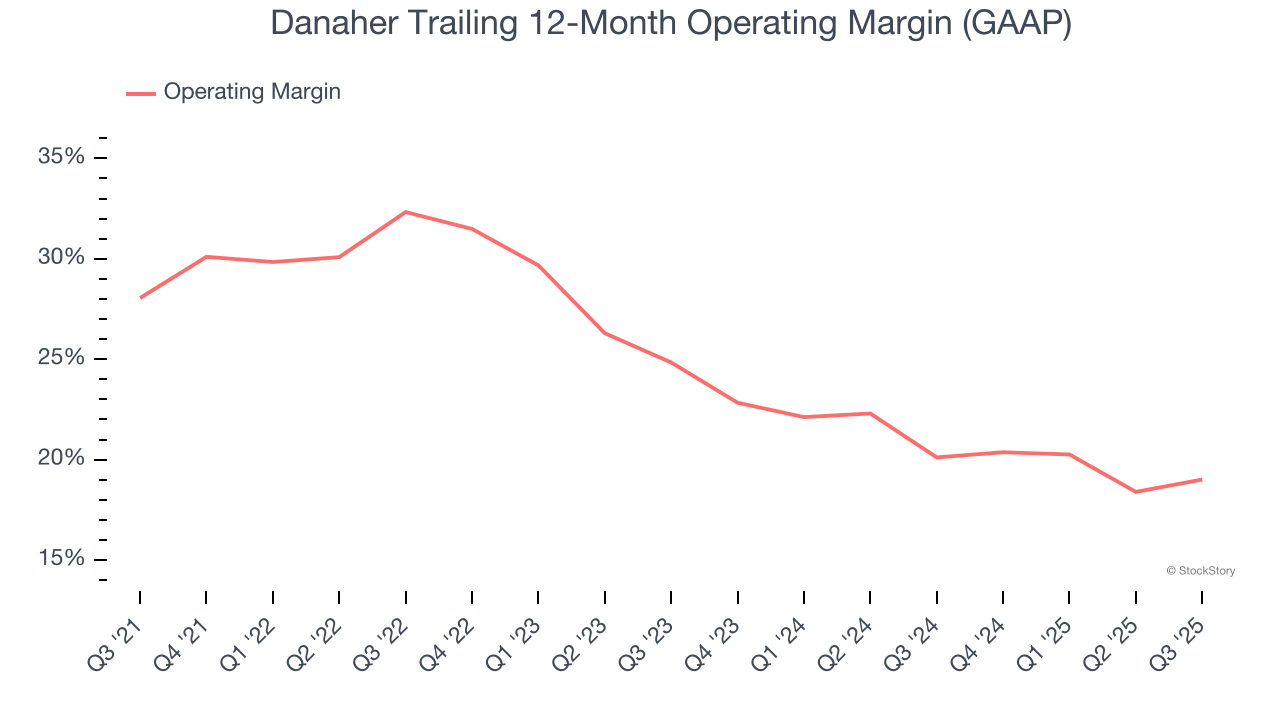

Danaher has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 25%.

Looking at the trend in its profitability, Danaher’s operating margin decreased by 9 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 5.8 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q3, Danaher generated an operating margin profit margin of 19.1%, up 2.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

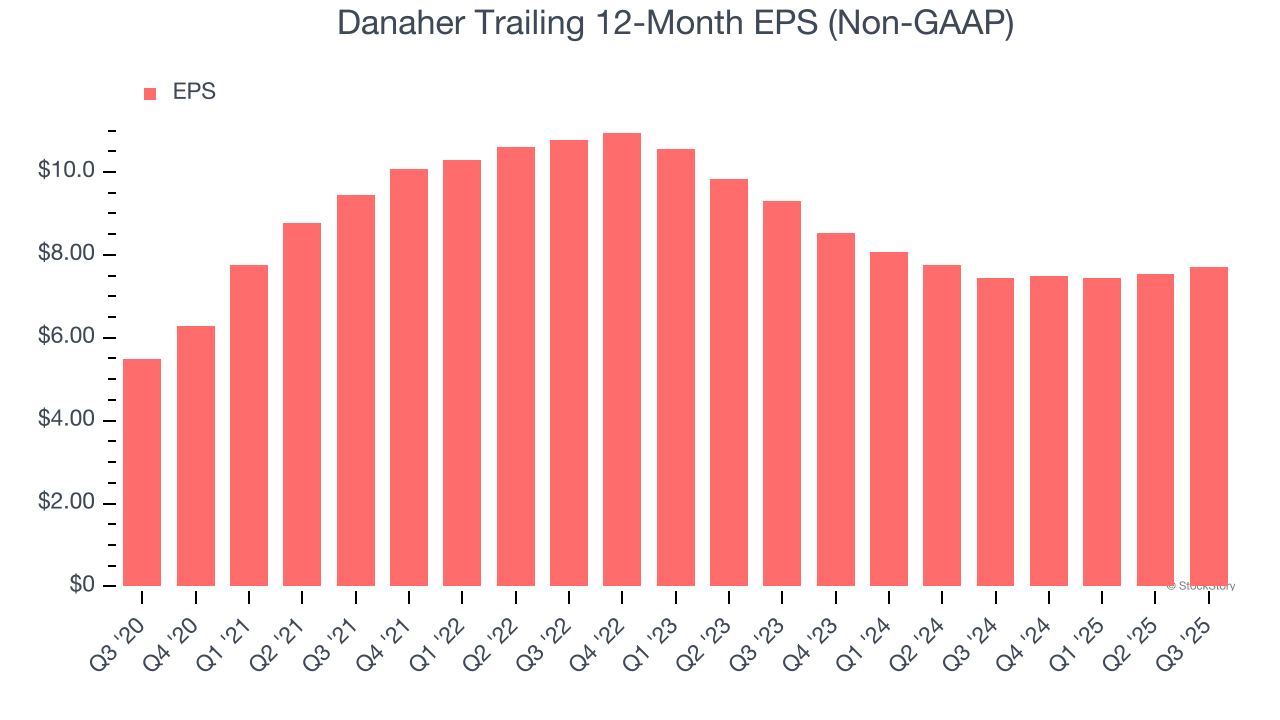

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Danaher’s EPS grew at a solid 7% compounded annual growth rate over the last five years, higher than its 4.7% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

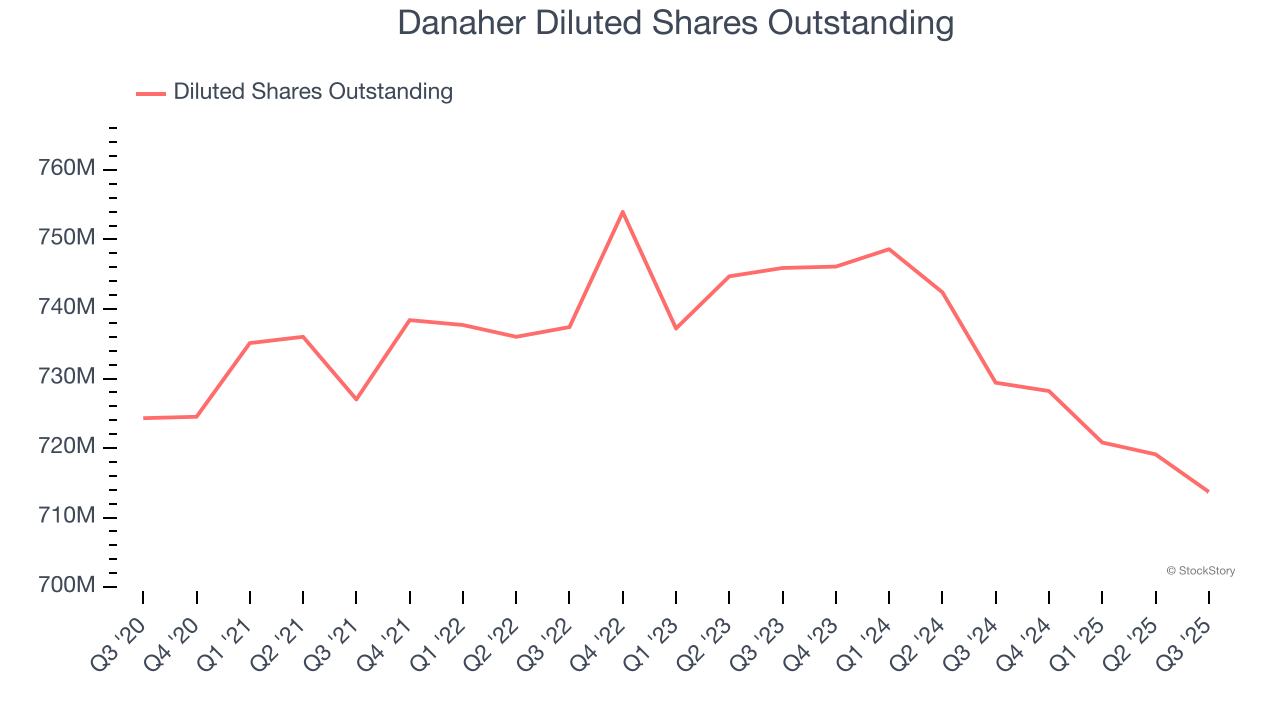

Diving into the nuances of Danaher’s earnings can give us a better understanding of its performance. A five-year view shows that Danaher has repurchased its stock, shrinking its share count by 1.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q3, Danaher reported adjusted EPS of $1.89, up from $1.71 in the same quarter last year. This print beat analysts’ estimates by 9.8%. Over the next 12 months, Wall Street expects Danaher’s full-year EPS of $7.71 to grow 7.7%.

Key Takeaways from Danaher’s Q3 Results

We enjoyed seeing Danaher beat analysts’ organic revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its full-year EPS guidance was just in line with Wall Street’s estimates. Overall, this print was mixed. The stock remained flat at $207 immediately following the results.

Big picture, is Danaher a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.