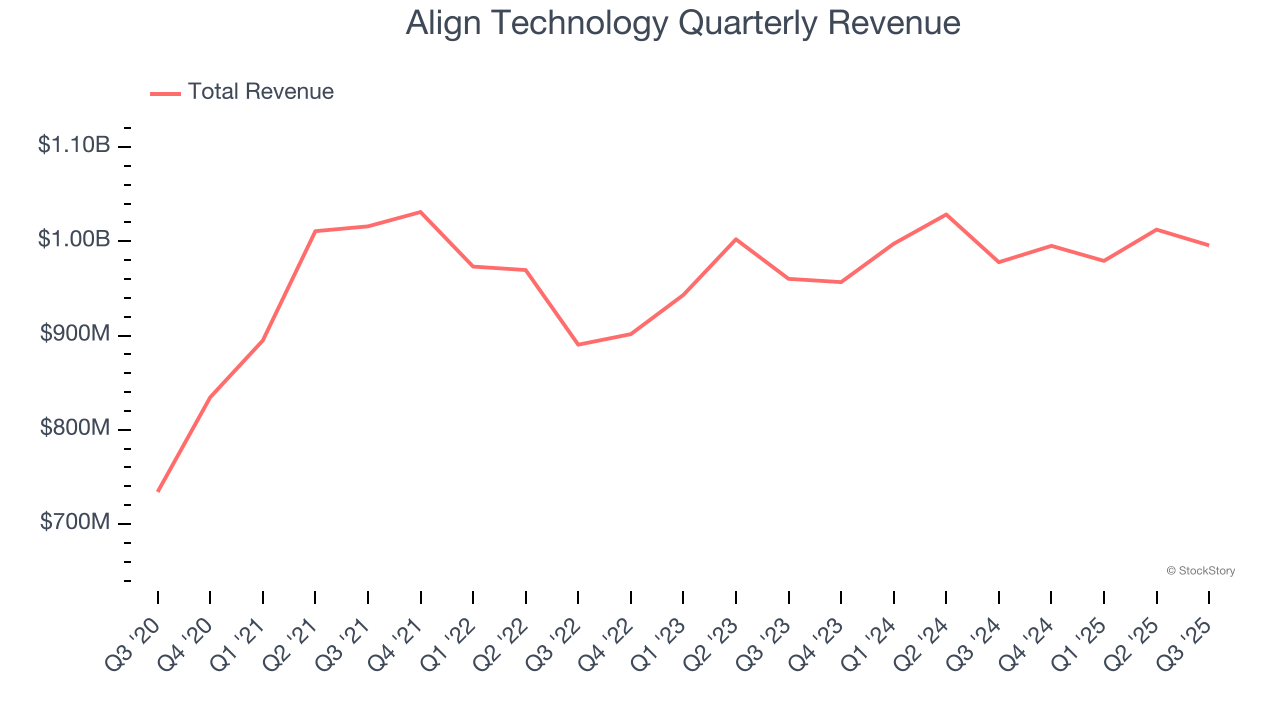

Dental technology company Align Technology (NASDAQ: ALGN) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 1.8% year on year to $995.7 million. The company expects next quarter’s revenue to be around $1.04 billion, close to analysts’ estimates. Its non-GAAP profit of $2.61 per share was 8.4% above analysts’ consensus estimates.

Is now the time to buy Align Technology? Find out by accessing our full research report, it’s free for active Edge members.

Align Technology (ALGN) Q3 CY2025 Highlights:

- Revenue: $995.7 million vs analyst estimates of $974.4 million (1.8% year-on-year growth, 2.2% beat)

- Adjusted EPS: $2.61 vs analyst estimates of $2.41 (8.4% beat)

- Adjusted Operating Income: $237.8 million vs analyst estimates of $216 million (23.9% margin, 10.1% beat)

- Revenue Guidance for Q4 CY2025 is $1.04 billion at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 9.7%, down from 16.6% in the same quarter last year

- Sales Volumes rose 4.9% year on year, in line with the same quarter last year

- Market Capitalization: $9.65 billion

Company Overview

Pioneering an alternative to traditional metal braces with nearly invisible plastic aligners, Align Technology (NASDAQ: ALGN) designs and manufactures Invisalign clear aligners, iTero intraoral scanners, and dental CAD/CAM software for orthodontic and restorative treatments.

Revenue Growth

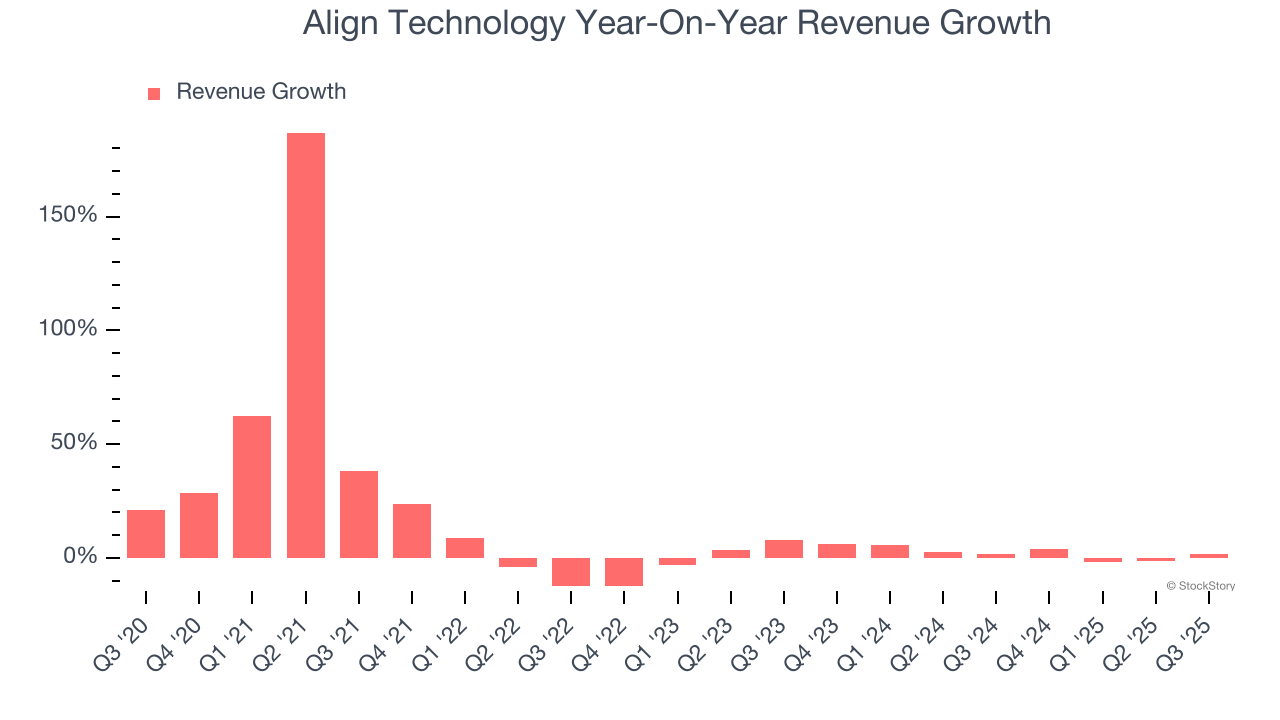

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, Align Technology’s sales grew at a decent 11.7% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Align Technology’s recent performance shows its demand has slowed as its annualized revenue growth of 2.3% over the last two years was below its five-year trend.

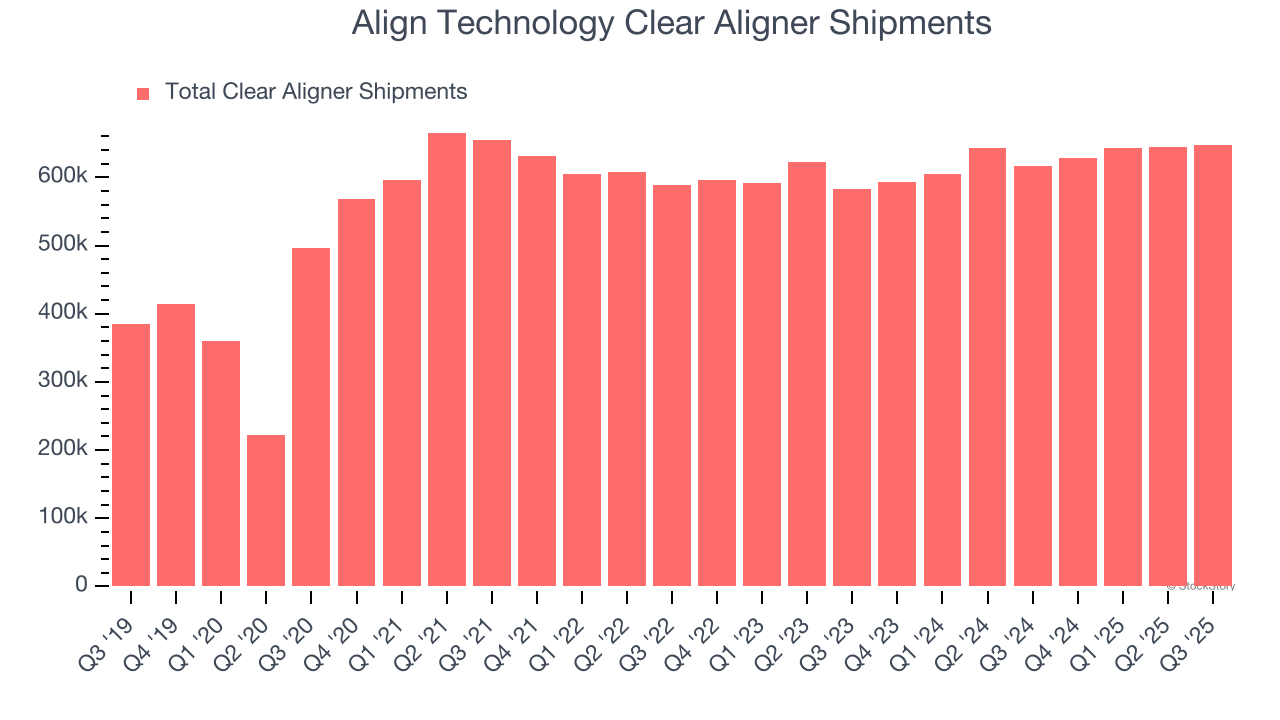

We can dig further into the company’s revenue dynamics by analyzing its number of clear aligner shipments, which reached 647,750 in the latest quarter. Over the last two years, Align Technology’s clear aligner shipments averaged 3.5% year-on-year growth. Because this number is in line with its revenue growth, we can see the company kept its prices fairly consistent.

This quarter, Align Technology reported modest year-on-year revenue growth of 1.8% but beat Wall Street’s estimates by 2.2%. Company management is currently guiding for a 4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not catalyze better top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

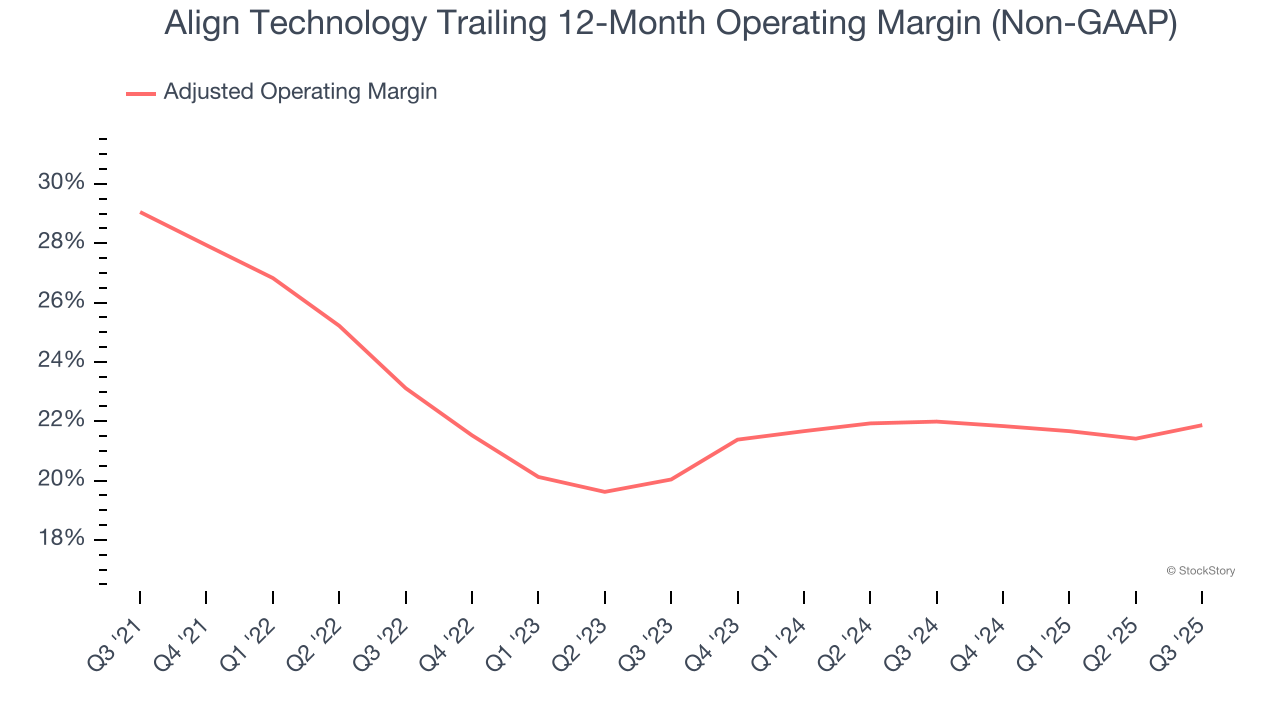

Adjusted Operating Margin

Align Technology has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 23.2%.

Looking at the trend in its profitability, Align Technology’s adjusted operating margin decreased by 7.2 percentage points over the last five years, but it rose by 1.8 percentage points on a two-year basis. Still, shareholders will want to see Align Technology become more profitable in the future.

This quarter, Align Technology generated an adjusted operating margin profit margin of 23.9%, up 1.8 percentage points year on year. This increase was a welcome development and shows it was more efficient.

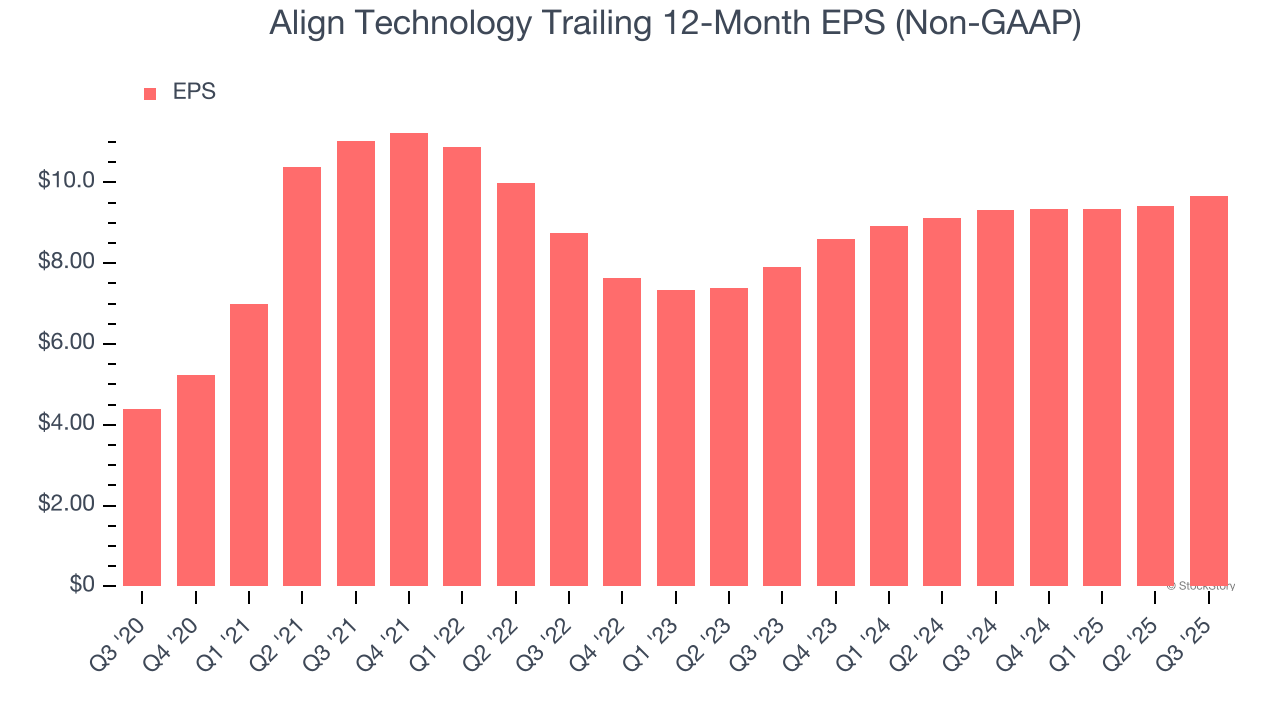

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Align Technology’s EPS grew at an astounding 17.1% compounded annual growth rate over the last five years, higher than its 11.7% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its adjusted operating margin didn’t improve.

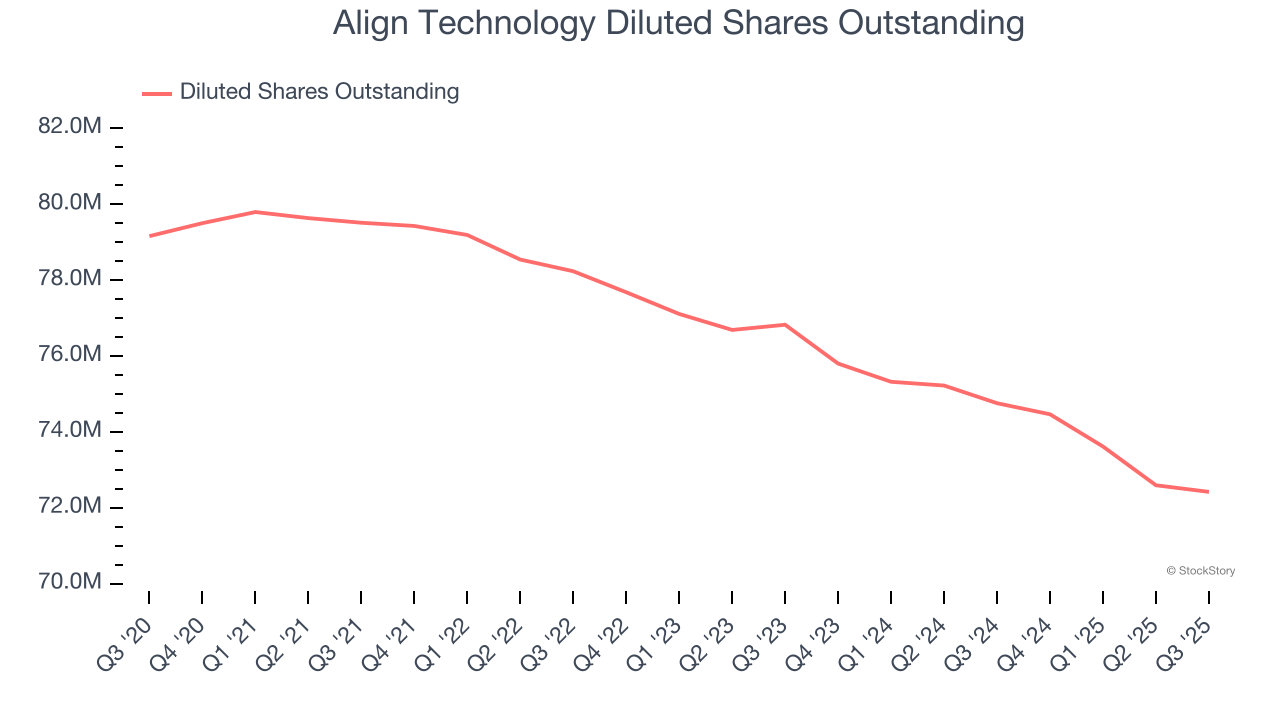

We can take a deeper look into Align Technology’s earnings to better understand the drivers of its performance. A five-year view shows that Align Technology has repurchased its stock, shrinking its share count by 8.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q3, Align Technology reported adjusted EPS of $2.61, up from $2.35 in the same quarter last year. This print beat analysts’ estimates by 8.4%. Over the next 12 months, Wall Street expects Align Technology’s full-year EPS of $9.67 to grow 10.5%.

Key Takeaways from Align Technology’s Q3 Results

It was encouraging to see Align Technology beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 15.5% to $152.50 immediately after reporting.

Indeed, Align Technology had a rock-solid quarterly earnings result, but is this stock a good investment here? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.