Wrapping up Q2 earnings, we look at the numbers and key takeaways for the modern fast food stocks, including Shake Shack (NYSE: SHAK) and its peers.

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

The 8 modern fast food stocks we track reported a slower Q2. As a group, revenues missed analysts’ consensus estimates by 1.5%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 18% since the latest earnings results.

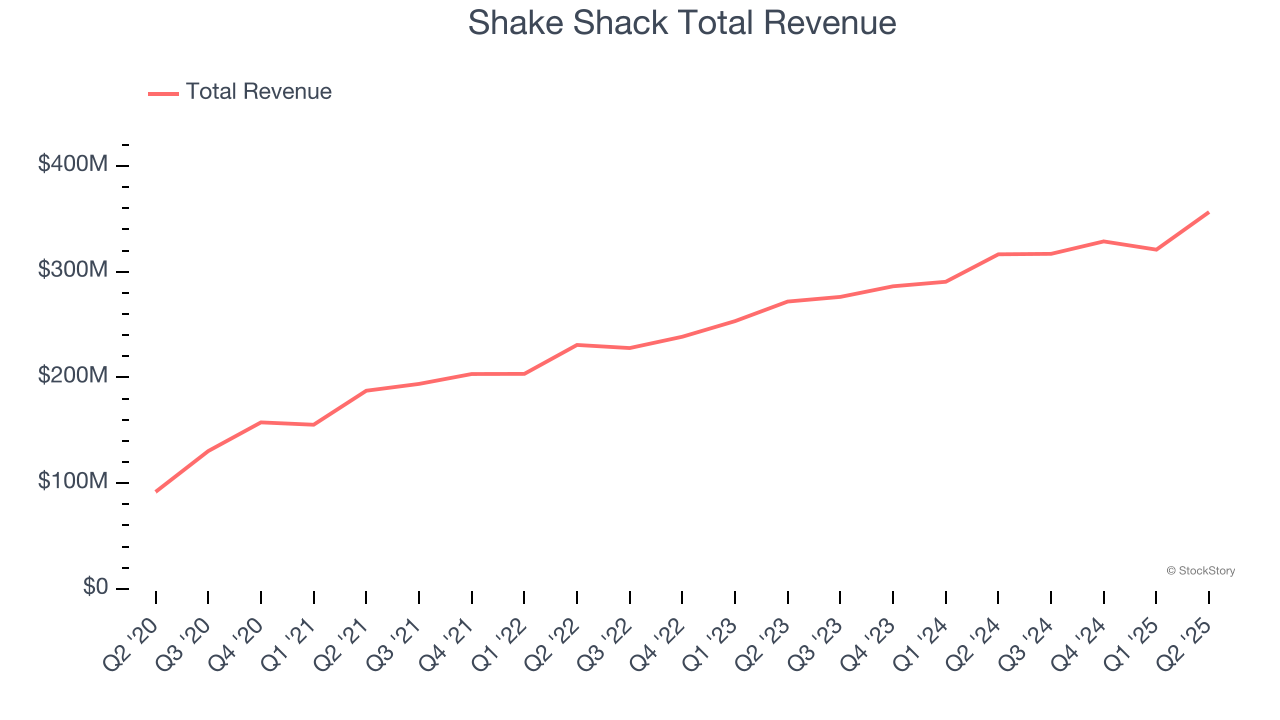

Best Q2: Shake Shack (NYSE: SHAK)

Started as a hot dog cart in New York City's Madison Square Park, Shake Shack (NYSE: SHAK) is a fast-food restaurant known for its burgers and milkshakes.

Shake Shack reported revenues of $356.5 million, up 12.6% year on year. This print exceeded analysts’ expectations by 0.9%. Overall, it was a strong quarter for the company with a solid beat of analysts’ EBITDA and EPS estimates.

Shake Shack scored the biggest analyst estimates beat of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 32.9% since reporting and currently trades at $94.59.

Is now the time to buy Shake Shack? Access our full analysis of the earnings results here, it’s free.

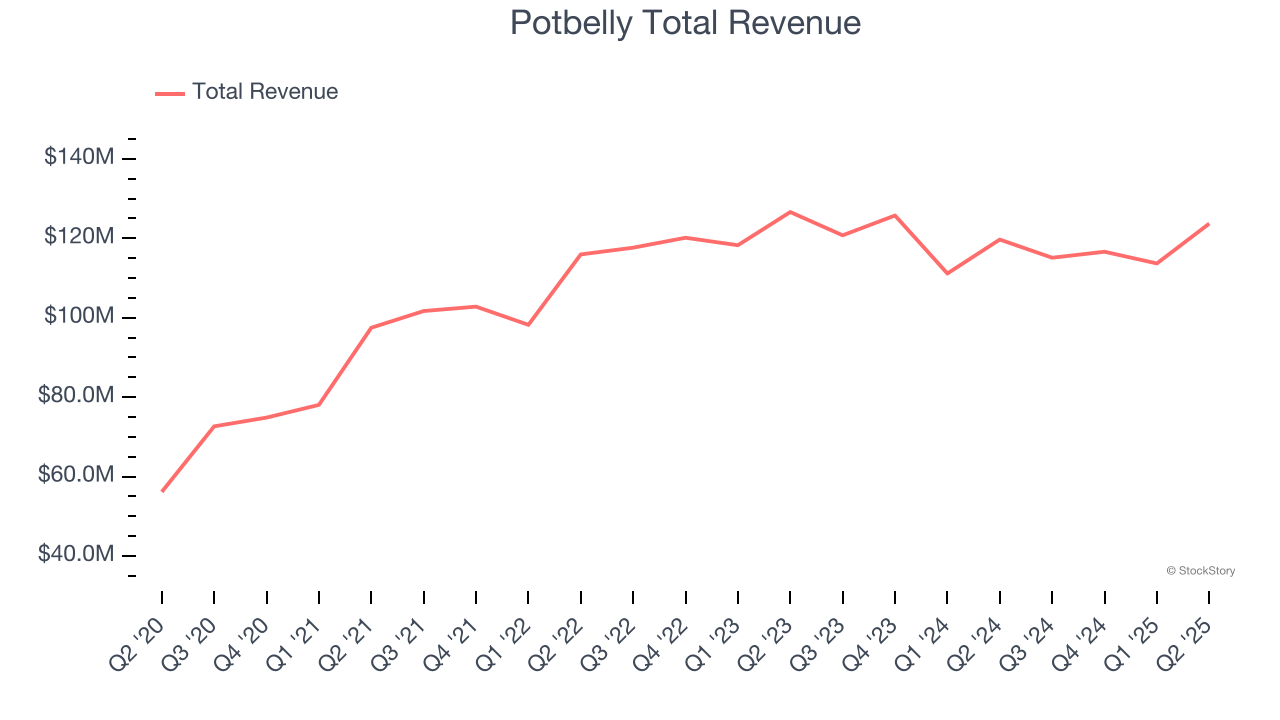

Potbelly (NASDAQ: PBPB)

With a unique origin story where the company actually started as an antique shop, Potbelly (NASDAQ: PBPB) today is a chain known for its toasty sandwiches.

Potbelly reported revenues of $123.7 million, up 3.4% year on year, outperforming analysts’ expectations by 0.9%. The business had a strong quarter with an impressive beat of analysts’ EBITDA estimates and full-year EBITDA guidance topping analysts’ expectations.

The market seems happy with the results as the stock is up 47.9% since reporting. It currently trades at $17.05.

Is now the time to buy Potbelly? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Noodles (NASDAQ: NDLS)

Offering pasta, mac and cheese, pad thai, and more, Noodles & Company (NASDAQ: NDLS) is a casual restaurant chain that serves all manner of noodles from around the world.

Noodles reported revenues of $126.4 million, flat year on year, falling short of analysts’ expectations by 3.9%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations.

Noodles delivered the highest full-year guidance raise but had the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 35.6% since the results and currently trades at $0.65.

Read our full analysis of Noodles’s results here.

Portillo's (NASDAQ: PTLO)

Begun as a Chicago hot dog stand in 1963, Portillo’s (NASDAQ: PTLO) is a casual restaurant chain that serves Chicago-style hot dogs and beef sandwiches as well as fries and shakes.

Portillo's reported revenues of $188.5 million, up 3.6% year on year. This print came in 3.9% below analysts' expectations. It was a slower quarter as it also recorded a slight miss of analysts’ same-store sales estimates.

The stock is down 31% since reporting and currently trades at $6.56.

Read our full, actionable report on Portillo's here, it’s free.

CAVA (NYSE: CAVA)

Starting from a single Washington, D.C. location, CAVA (NYSE: CAVA) operates a fast-casual restaurant chain offering customizable Mediterranean-inspired dishes.

CAVA reported revenues of $280.6 million, up 20.2% year on year. This number missed analysts’ expectations by 1.8%. Overall, it was a slower quarter as it also logged a significant miss of analysts’ same-store sales estimates and full-year EBITDA guidance missing analysts’ expectations.

CAVA achieved the fastest revenue growth among its peers. The stock is down 25.1% since reporting and currently trades at $63.39.

Read our full, actionable report on CAVA here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.