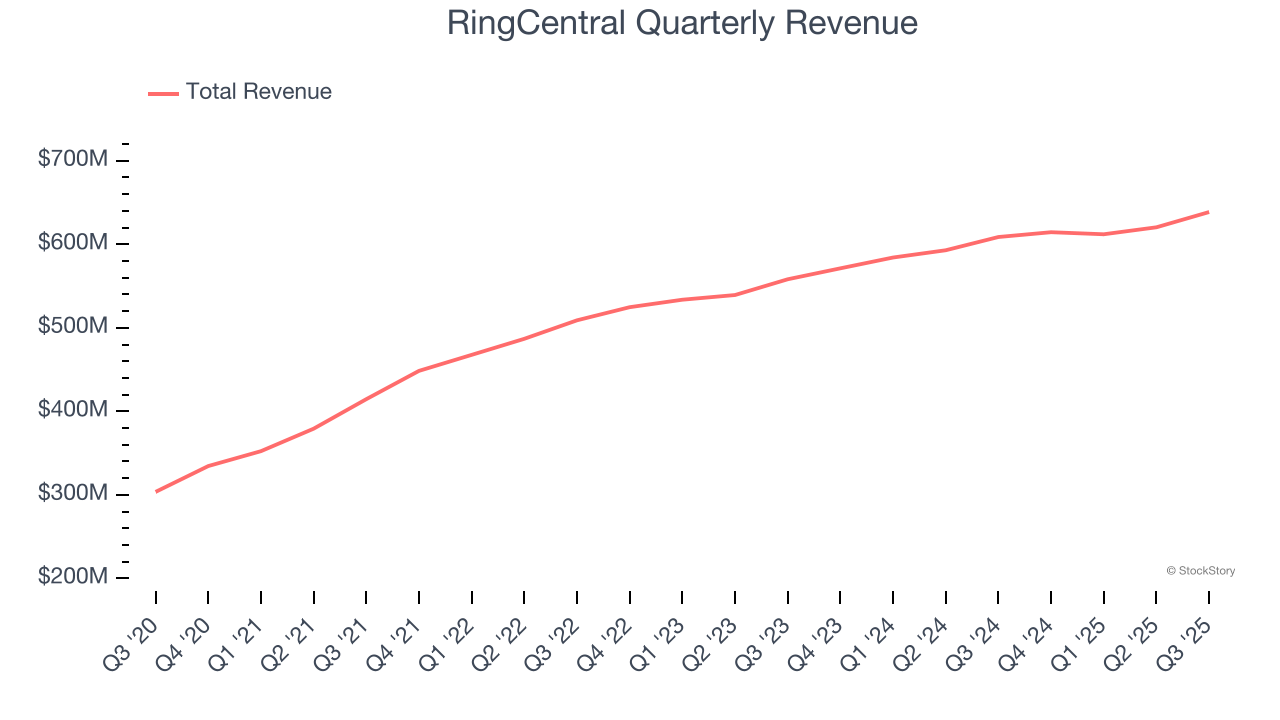

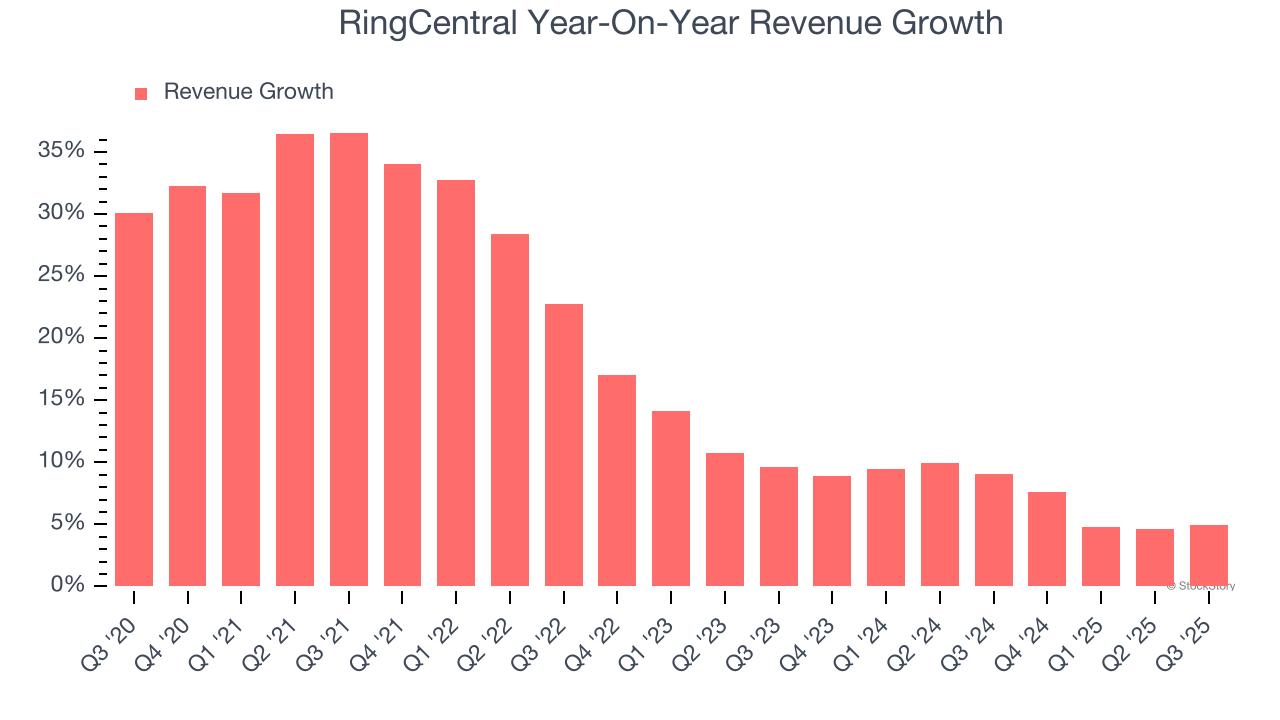

Cloud communications provider RingCentral (NYSE: RNG) met Wall Streets revenue expectations in Q3 CY2025, with sales up 4.9% year on year to $638.7 million. On the other hand, next quarter’s revenue guidance of $622 million was less impressive, coming in 3.8% below analysts’ estimates. Its non-GAAP profit of $1.13 per share was 5.2% above analysts’ consensus estimates.

Is now the time to buy RingCentral? Find out by accessing our full research report, it’s free for active Edge members.

RingCentral (RNG) Q3 CY2025 Highlights:

- Revenue: $638.7 million vs analyst estimates of $635.6 million (4.9% year-on-year growth, in line)

- Adjusted EPS: $1.13 vs analyst estimates of $1.07 (5.2% beat)

- Adjusted Operating Income: $103.9 million vs analyst estimates of $143.7 million (16.3% margin, 27.7% miss)

- Revenue Guidance for Q4 CY2025 is $622 million at the midpoint, below analyst estimates of $646.7 million

- Management raised its full-year Adjusted EPS guidance to $4.31 at the midpoint, a 1.2% increase

- Operating Margin: 0%, in line with the same quarter last year

- Free Cash Flow Margin: 20.3%, down from 23.3% in the previous quarter

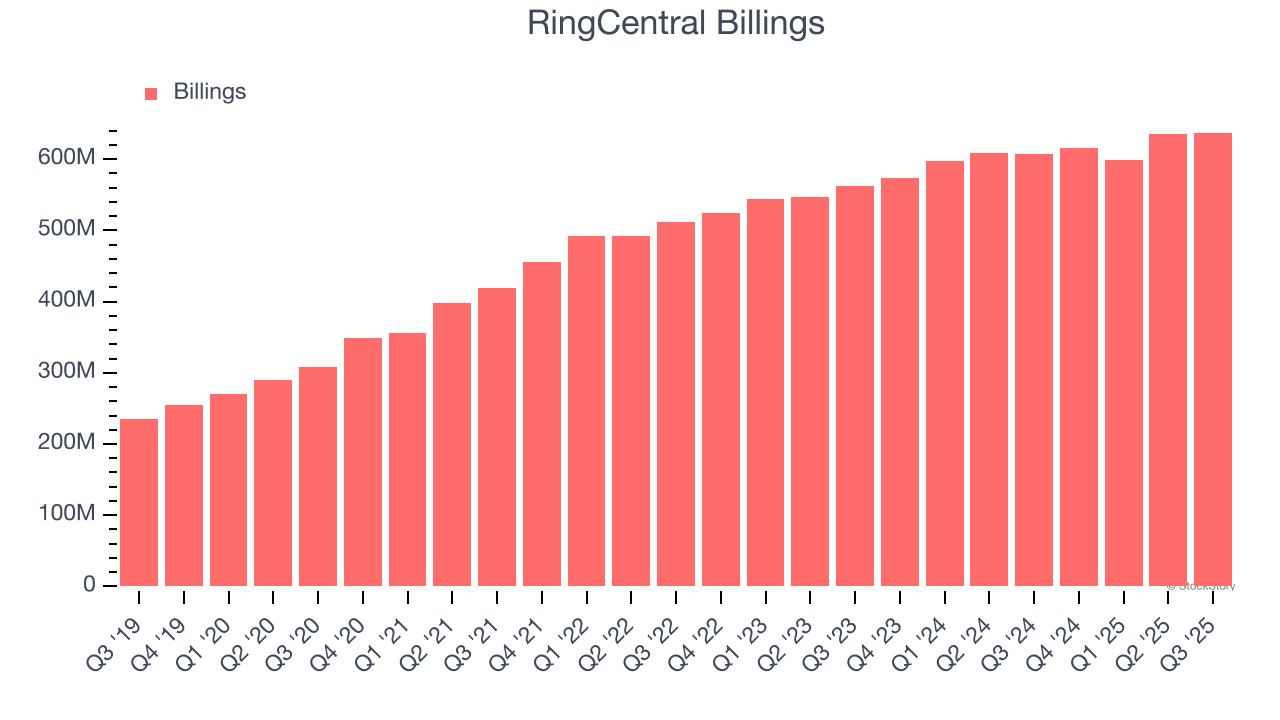

- Billings: $637.2 million at quarter end, up 4.9% year on year

- Market Capitalization: $2.73 billion

“We delivered a solid quarter reinforcing our leadership in cloud business voice while expanding margins and delivering strong free cash flow,” said Vlad Shmunis, founder and CEO of RingCentral.

Company Overview

Built on its proprietary Message Video Phone (MVP) platform that unifies multiple communication methods, RingCentral (NYSE: RNG) provides AI-driven cloud communications and collaboration solutions that enable businesses to connect through voice, video, messaging, and contact center services.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, RingCentral grew its sales at a decent 17.7% compounded annual growth rate. Its growth was slightly above the average software company and shows its offerings resonate with customers.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. RingCentral’s recent performance shows its demand has slowed as its annualized revenue growth of 7.4% over the last two years was below its five-year trend.

This quarter, RingCentral grew its revenue by 4.9% year on year, and its $638.7 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 1.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.2% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

RingCentral’s billings came in at $637.2 million in Q3, and over the last four quarters, its growth was underwhelming as it averaged 4.2% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

RingCentral’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between RingCentral’s products and its peers.

Key Takeaways from RingCentral’s Q3 Results

It was good to see RingCentral provide full-year EPS guidance that slightly beat analysts’ expectations. On the other hand, its adjusted operating profit missed. Additionally, revenue guidance for next quarter missed and billings were just in line with Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 2.7% to $29.10 immediately after reporting.

RingCentral didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.