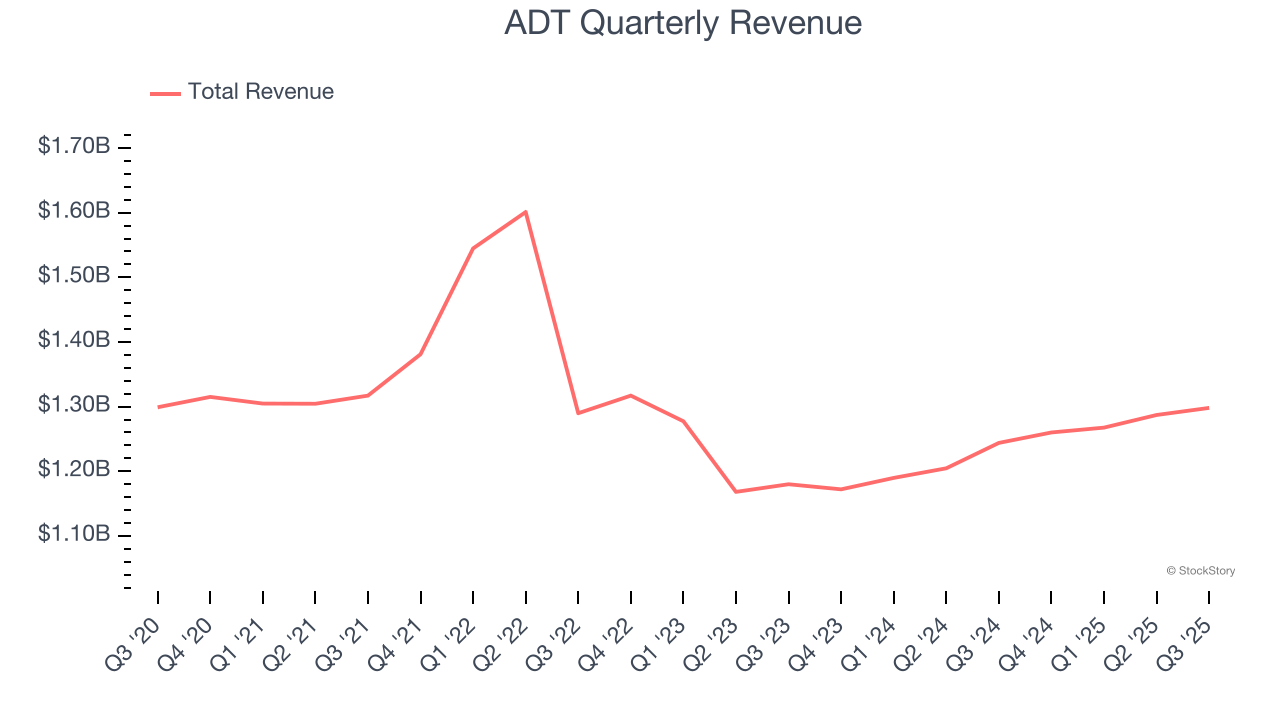

Security technology and services company ADT (NYSE: ADT) met Wall Streets revenue expectations in Q3 CY2025, with sales up 4.4% year on year to $1.30 billion. On the other hand, the company’s full-year revenue guidance of $5.13 billion at the midpoint came in 0.5% below analysts’ estimates. Its non-GAAP profit of $0.23 per share was 6.9% above analysts’ consensus estimates.

Is now the time to buy ADT? Find out by accessing our full research report, it’s free for active Edge members.

ADT (ADT) Q3 CY2025 Highlights:

- Revenue: $1.30 billion vs analyst estimates of $1.29 billion (4.4% year-on-year growth, in line)

- Adjusted EPS: $0.23 vs analyst estimates of $0.22 (6.9% beat)

- Adjusted EBITDA: $676 million vs analyst estimates of $675.6 million (52.1% margin, in line)

- The company reconfirmed its revenue guidance for the full year of $5.13 billion at the midpoint

- Management raised its full-year Adjusted EPS guidance to $0.87 at the midpoint, a 2.4% increase

- EBITDA guidance for the full year is $2.69 billion at the midpoint, in line with analyst expectations

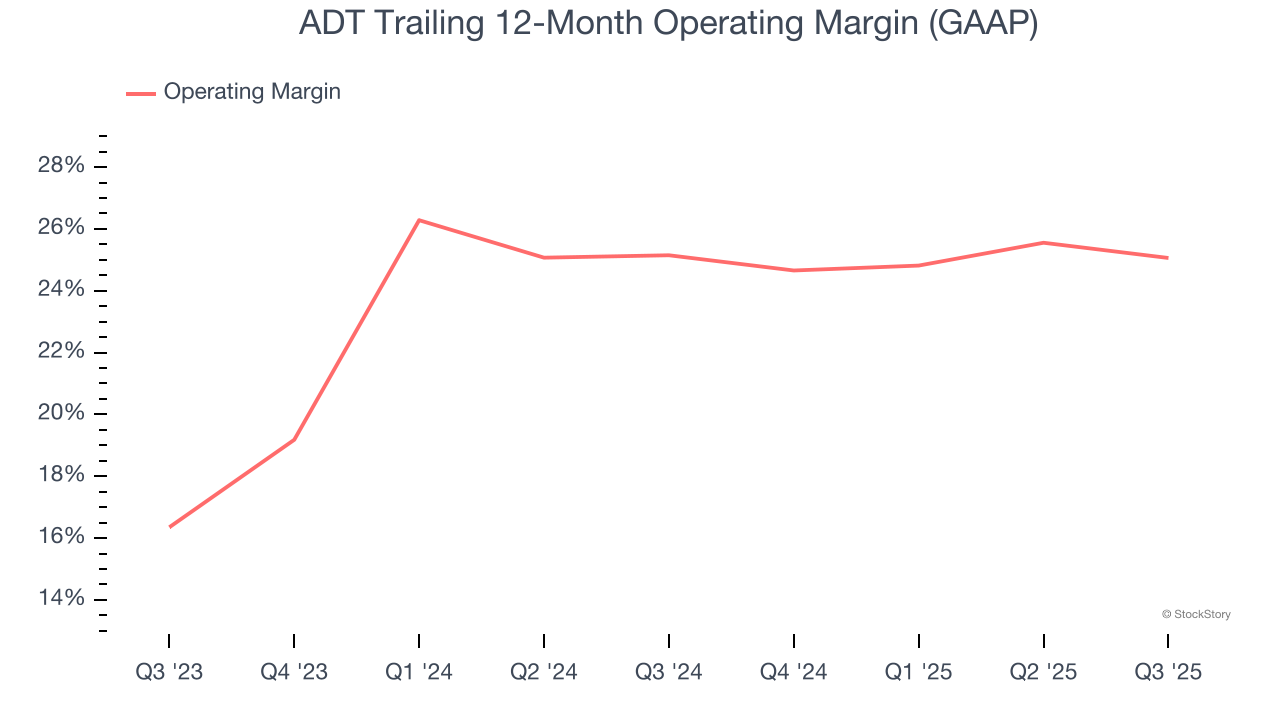

- Operating Margin: 24.3%, down from 26.2% in the same quarter last year

- Free Cash Flow Margin: 33.7%, up from 11% in the same quarter last year

- Market Capitalization: $7.25 billion

“ADT again delivered solid revenue growth, robust cash flow, and very strong earnings per share in the third quarter, reflecting the resilience of our business model and our team’s execution of our strategy,” said ADT Chairman, President and CEO, Jim DeVries.

Company Overview

Founded in 1874 and headquartered in Boca Raton, Florida, ADT (NYSE: ADT) is a provider of security, automation, and smart home solutions, offering comprehensive services for home and business protection.

Revenue Growth

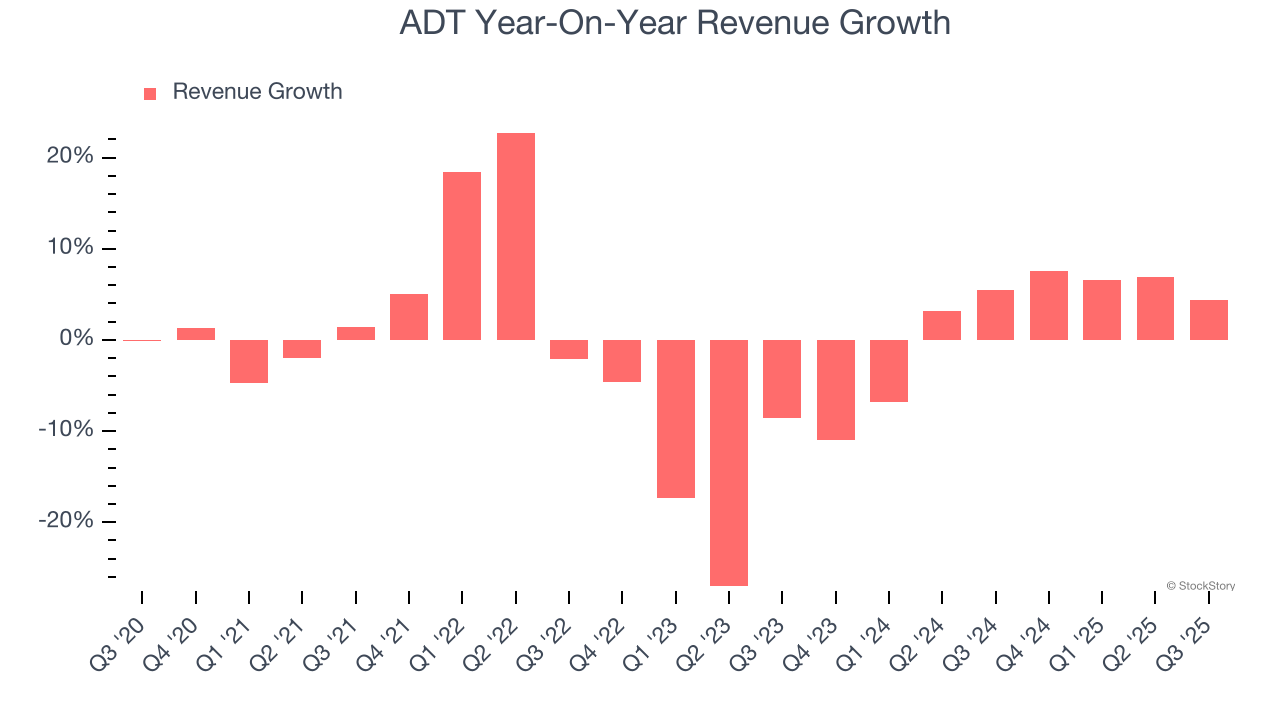

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, ADT struggled to consistently increase demand as its $5.11 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a lower quality business.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. ADT’s annualized revenue growth of 1.7% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, ADT grew its revenue by 4.4% year on year, and its $1.30 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

ADT’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 25.1% over the last two years. This profitability was elite for a consumer discretionary business thanks to its efficient cost structure and economies of scale.

In Q3, ADT generated an operating margin profit margin of 24.3%, down 2 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

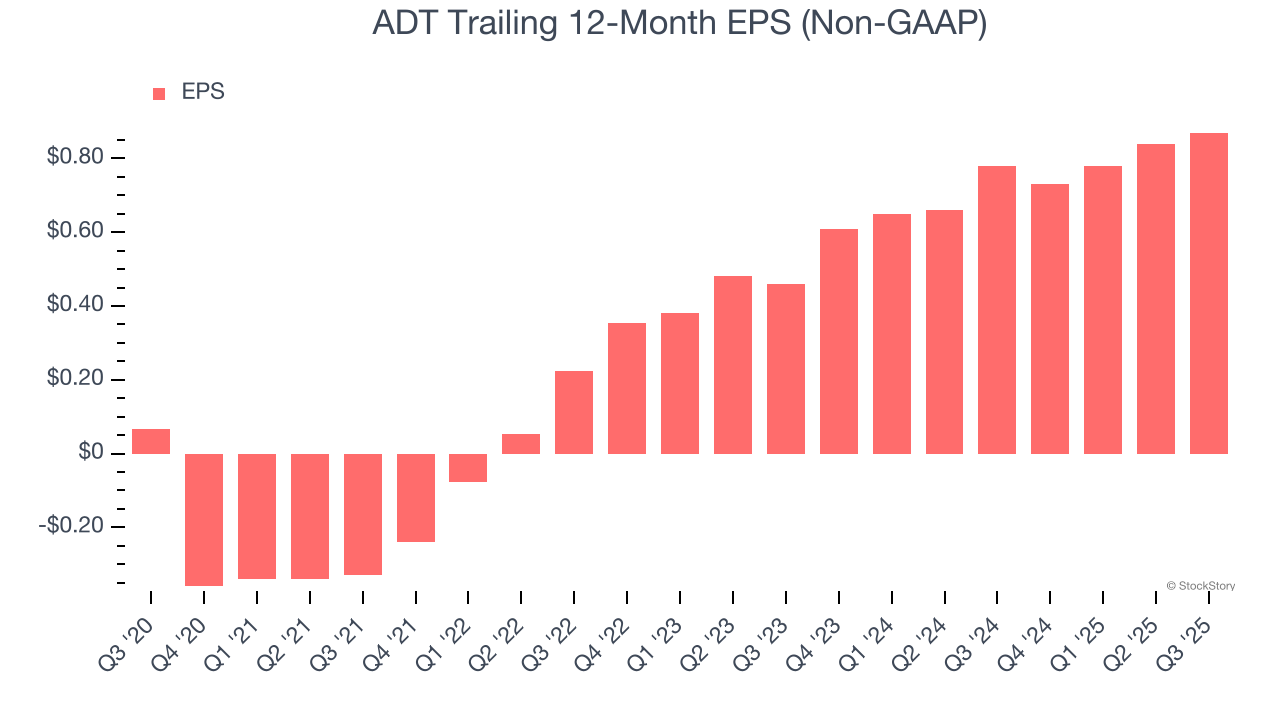

ADT’s EPS grew at an astounding 67.5% compounded annual growth rate over the last five years, higher than its flat revenue. This tells us management responded to softer demand by adapting its cost structure.

In Q3, ADT reported adjusted EPS of $0.23, up from $0.20 in the same quarter last year. This print beat analysts’ estimates by 6.9%. Over the next 12 months, Wall Street expects ADT’s full-year EPS of $0.87 to grow 7.9%.

Key Takeaways from ADT’s Q3 Results

It was good to see ADT beat analysts’ EPS expectations this quarter. On the other hand, its full-year revenue guidance slightly missed. Overall, this was a weaker quarter. The stock traded down 3.2% to $8.49 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.