Infrastructure and defense services provider Parsons (NYSE: PSN) missed Wall Street’s revenue expectations in Q3 CY2025, with sales falling 10.4% year on year to $1.62 billion. The company’s full-year revenue guidance of $6.45 billion at the midpoint came in 1.9% below analysts’ estimates. Its non-GAAP profit of $0.86 per share was 14.5% above analysts’ consensus estimates.

Is now the time to buy Parsons? Find out by accessing our full research report, it’s free for active Edge members.

Parsons (PSN) Q3 CY2025 Highlights:

- Revenue: $1.62 billion vs analyst estimates of $1.66 billion (10.4% year-on-year decline, 2.3% miss)

- Adjusted EPS: $0.86 vs analyst estimates of $0.75 (14.5% beat)

- Adjusted EBITDA: $158.1 million vs analyst estimates of $150.9 million (9.8% margin, 4.8% beat)

- The company dropped its revenue guidance for the full year to $6.45 billion at the midpoint from $6.58 billion, a 2% decrease

- EBITDA guidance for the full year is $615 million at the midpoint, below analyst estimates of $621 million

- Operating Margin: 6.7%, in line with the same quarter last year

- Free Cash Flow Margin: 9.2%, down from 15.9% in the same quarter last year

- Backlog: $8.83 billion at quarter end, in line with the same quarter last year

- Market Capitalization: $8.50 billion

“We are pleased with our third quarter results. We delivered double-digit revenue growth, achieved 60 basis points of margin expansion, exceeded our cash flow expectation, secured defense contracts in the Administration's priority areas, and continued to deliver outstanding results in our Critical Infrastructure segment. In addition, our win rates and hiring and retention remain strong, and we completed another accretive acquisition after the quarter ended,” said Carey Smith, chair, president and chief executive officer.

Company Overview

Delivering aerospace technology during the Cold War-era, Parsons (NYSE: PSN) offers engineering, construction, and cybersecurity solutions for the infrastructure and defense sectors.

Revenue Growth

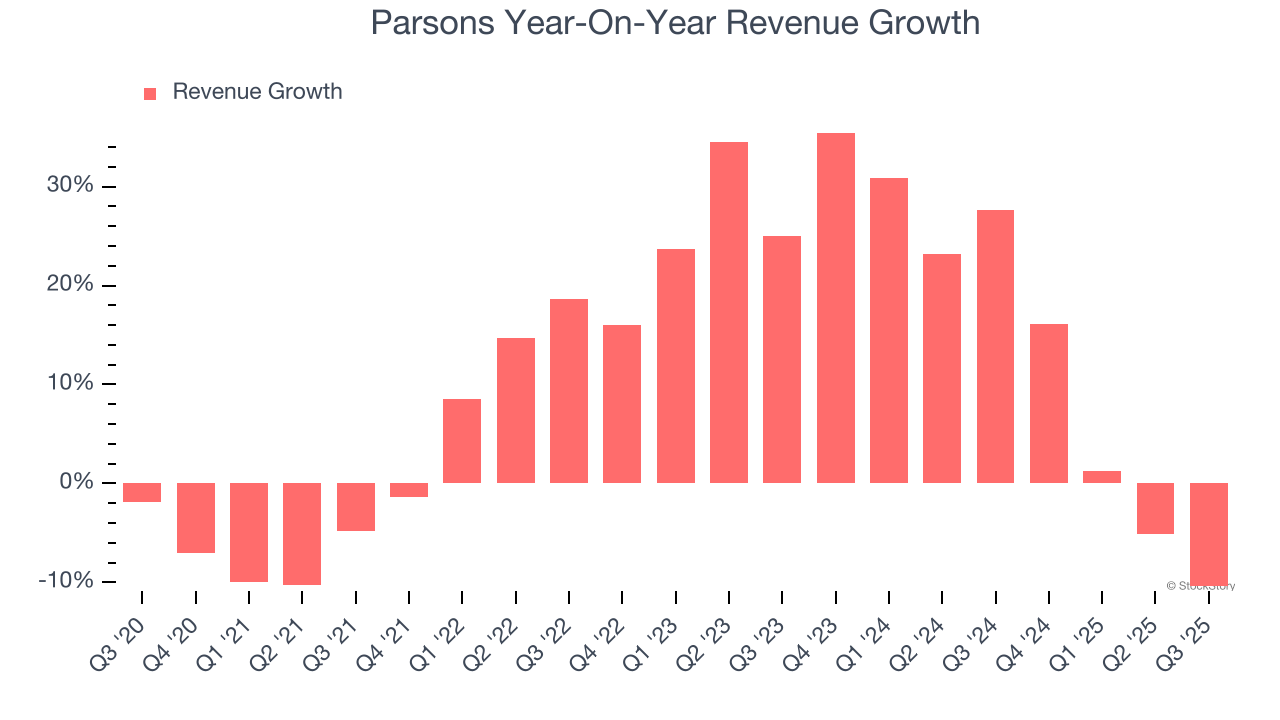

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Parsons’s 10.2% annualized revenue growth over the last five years was solid. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Parsons’s annualized revenue growth of 13.4% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

Parsons also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Parsons’s backlog reached $8.83 billion in the latest quarter and averaged 2.2% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies Parsons was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, Parsons missed Wall Street’s estimates and reported a rather uninspiring 10.4% year-on-year revenue decline, generating $1.62 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

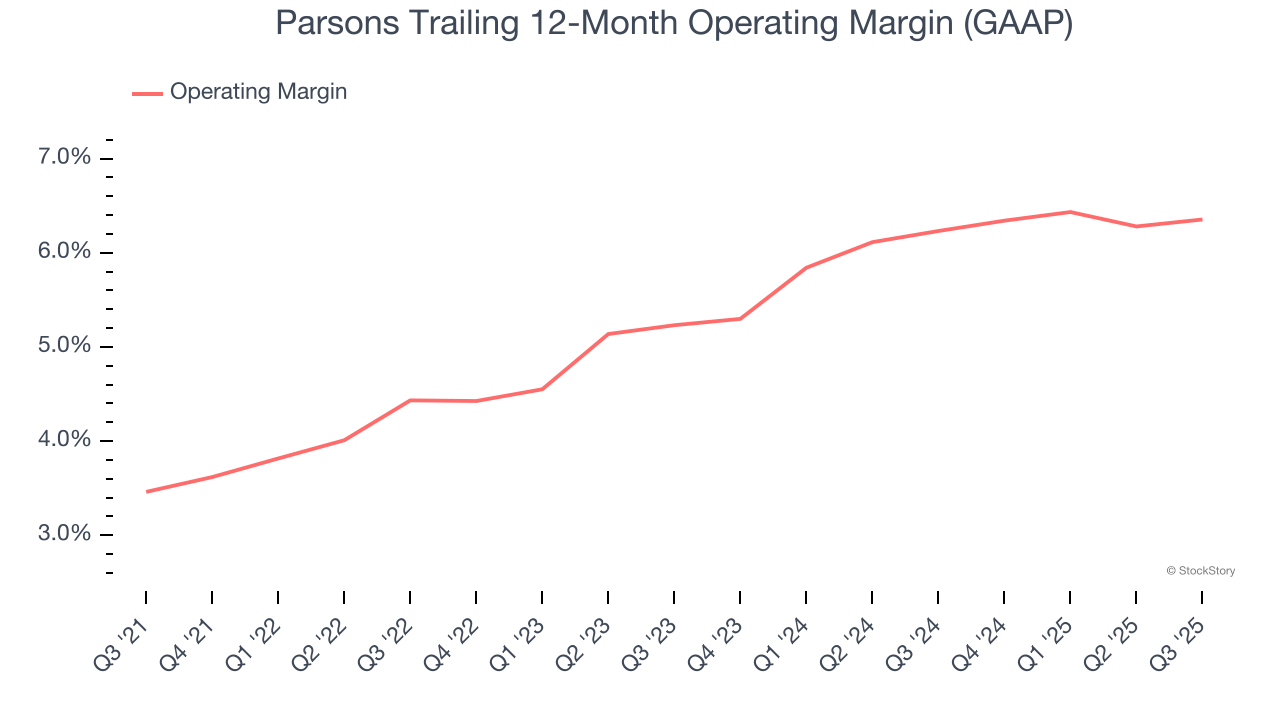

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Parsons was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.4% was weak for an industrials business.

On the plus side, Parsons’s operating margin rose by 2.9 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q3, Parsons generated an operating margin profit margin of 6.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

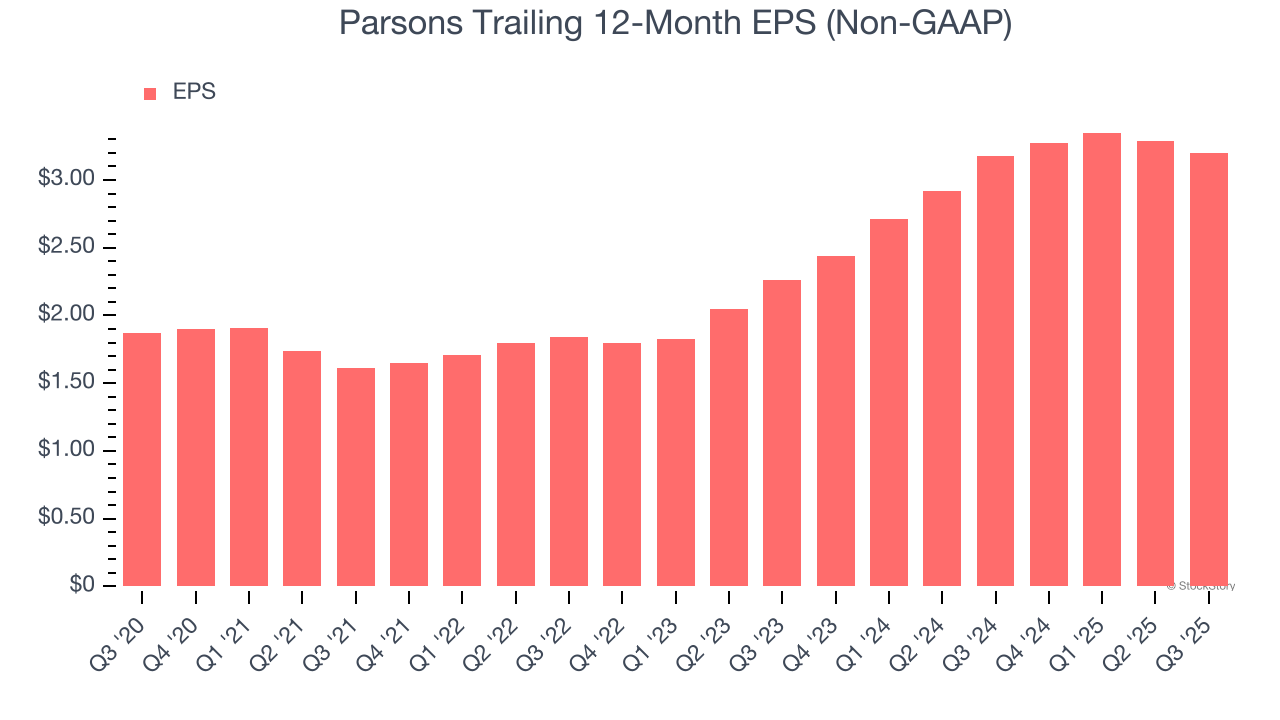

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Parsons’s solid 11.3% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Parsons’s two-year annual EPS growth of 19% was fantastic and topped its 13.4% two-year revenue growth.

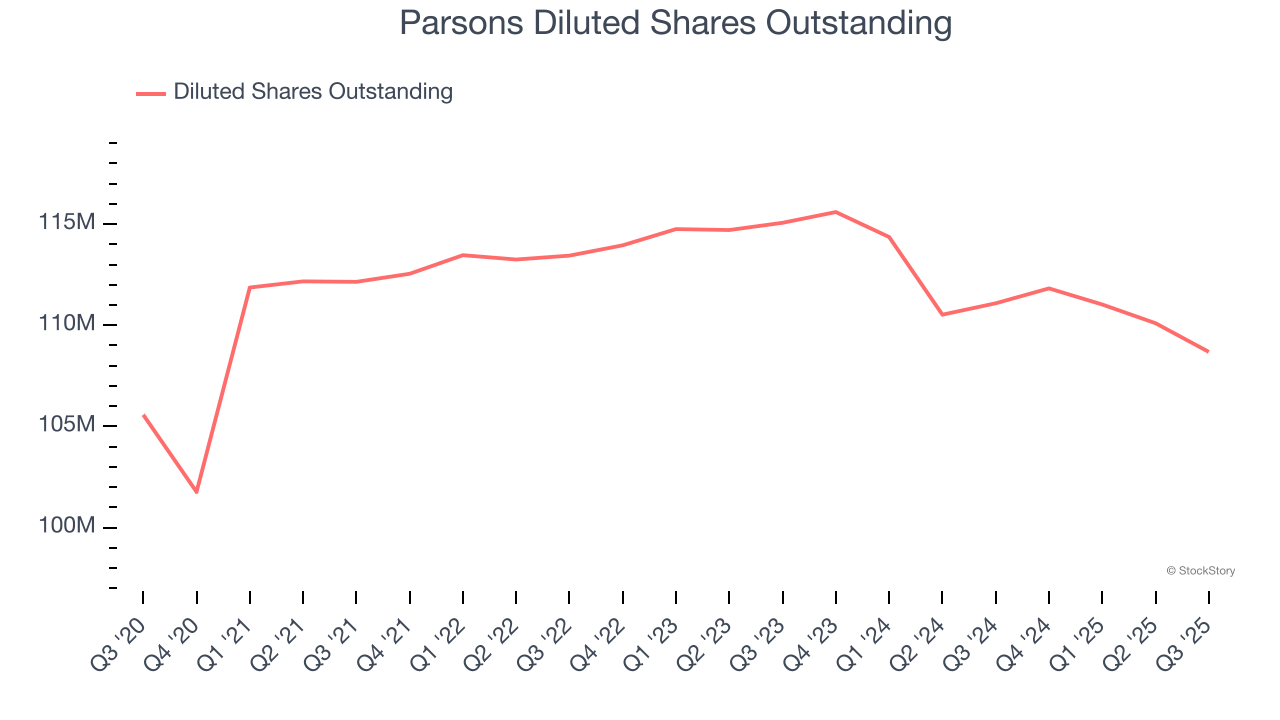

Diving into the nuances of Parsons’s earnings can give us a better understanding of its performance. A two-year view shows that Parsons has repurchased its stock, shrinking its share count by 5.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q3, Parsons reported adjusted EPS of $0.86, down from $0.95 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Parsons’s full-year EPS of $3.20 to grow 8.9%.

Key Takeaways from Parsons’s Q3 Results

We enjoyed seeing Parsons beat analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue missed and its backlog fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 9.1% to $72.27 immediately after reporting.

Parsons’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.