Over the past six months, Parsons’s stock price fell to $60.66. Shareholders have lost 9.5% of their capital, which is disappointing considering the S&P 500 has climbed by 13%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Following the pullback, is now an opportune time to buy PSN? Find out in our full research report, it’s free for active Edge members.

Why Does PSN Stock Spark Debate?

Delivering aerospace technology during the Cold War-era, Parsons (NYSE: PSN) offers engineering, construction, and cybersecurity solutions for the infrastructure and defense sectors.

Two Positive Attributes:

1. Long-Term Revenue Growth Shows Strong Momentum

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Parsons’s 10.2% annualized revenue growth over the last five years was solid. Its growth surpassed the average industrials company and shows its offerings resonate with customers.

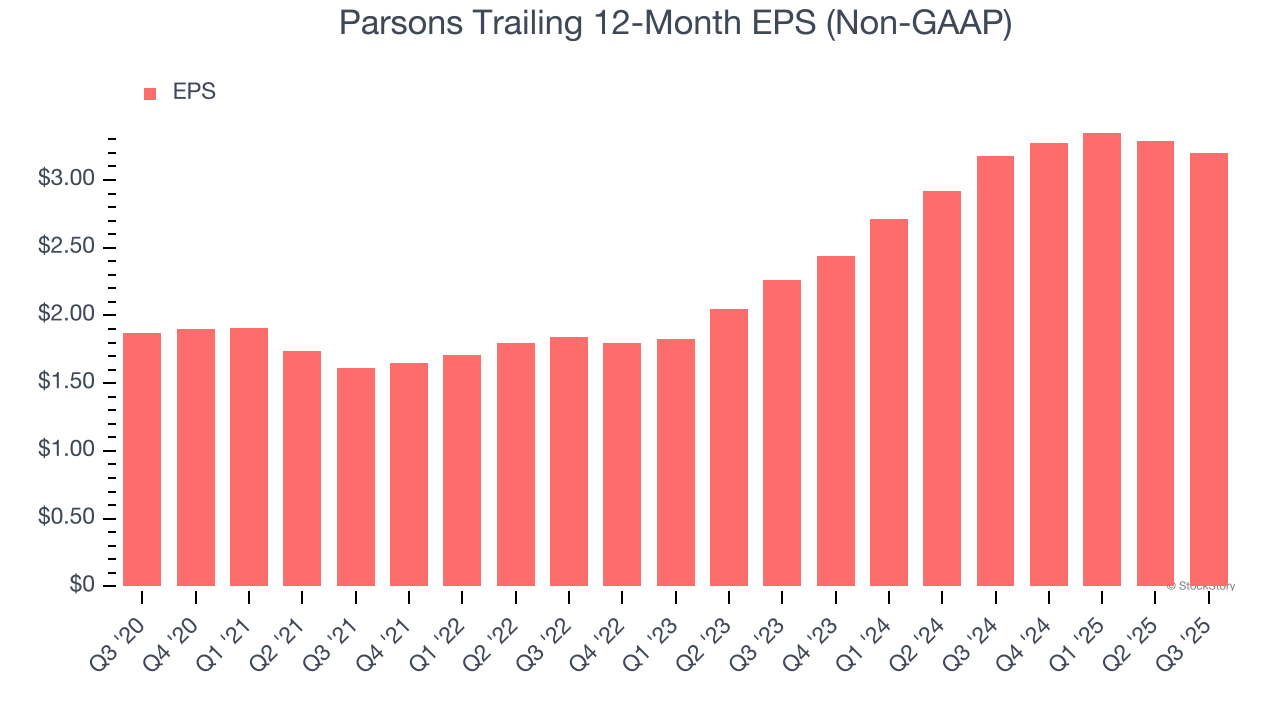

2. EPS Increasing Steadily

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Parsons’s solid 11.3% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

One Reason to be Careful:

Weak Backlog Growth Points to Soft Demand

Investors interested in Defense Contractors companies should track backlog in addition to reported revenue. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Parsons’s future revenue streams.

Parsons’s backlog came in at $8.83 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 2.2%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

Final Judgment

Parsons has huge potential even though it has some open questions. With the recent decline, the stock trades at 18.1× forward P/E (or $60.66 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free for active Edge members .

High-Quality Stocks for All Market Conditions

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.