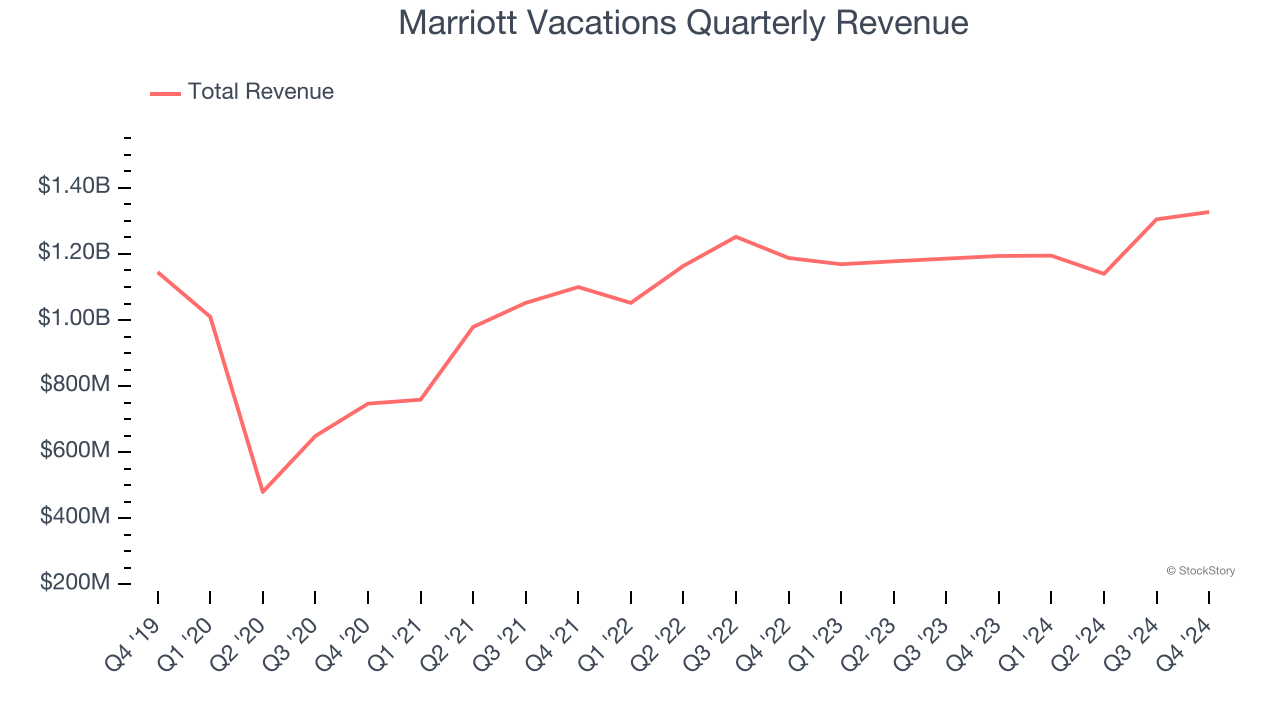

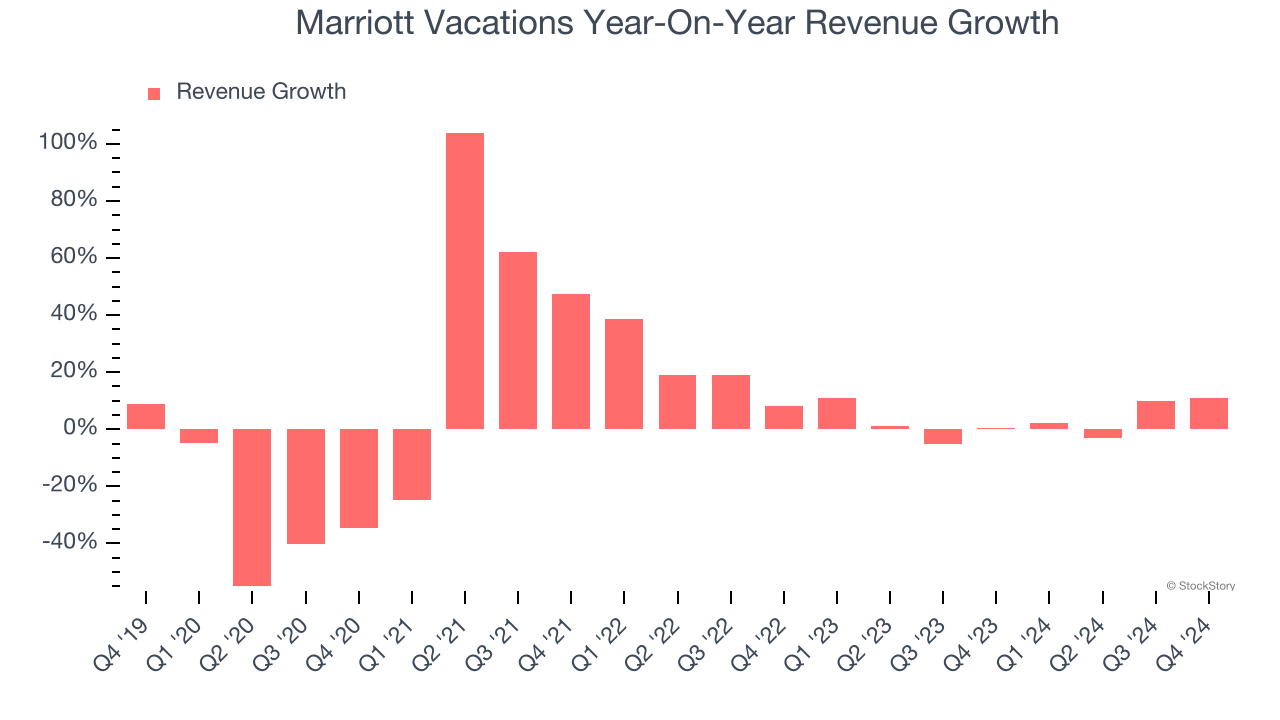

Vacation ownership company Marriott Vacations (NYSE: VAC) announced better-than-expected revenue in Q4 CY2024, with sales up 11.1% year on year to $1.33 billion. Its non-GAAP profit of $1.86 per share was 19.2% above analysts’ consensus estimates.

Is now the time to buy Marriott Vacations? Find out by accessing our full research report, it’s free.

Marriott Vacations (VAC) Q4 CY2024 Highlights:

- Revenue: $1.33 billion vs analyst estimates of $1.24 billion (11.1% year-on-year growth, 6.7% beat)

- Adjusted EPS: $1.86 vs analyst estimates of $1.56 (19.2% beat)

- Adjusted EBITDA: $185 million vs analyst estimates of $170.2 million (13.9% margin, 8.7% beat)

- Adjusted EPS guidance for the upcoming financial year 2025 is $6.65 at the midpoint, missing analyst estimates by 13.6%

- EBITDA guidance for the upcoming financial year 2025 is $765 million at the midpoint, below analyst estimates of $783 million

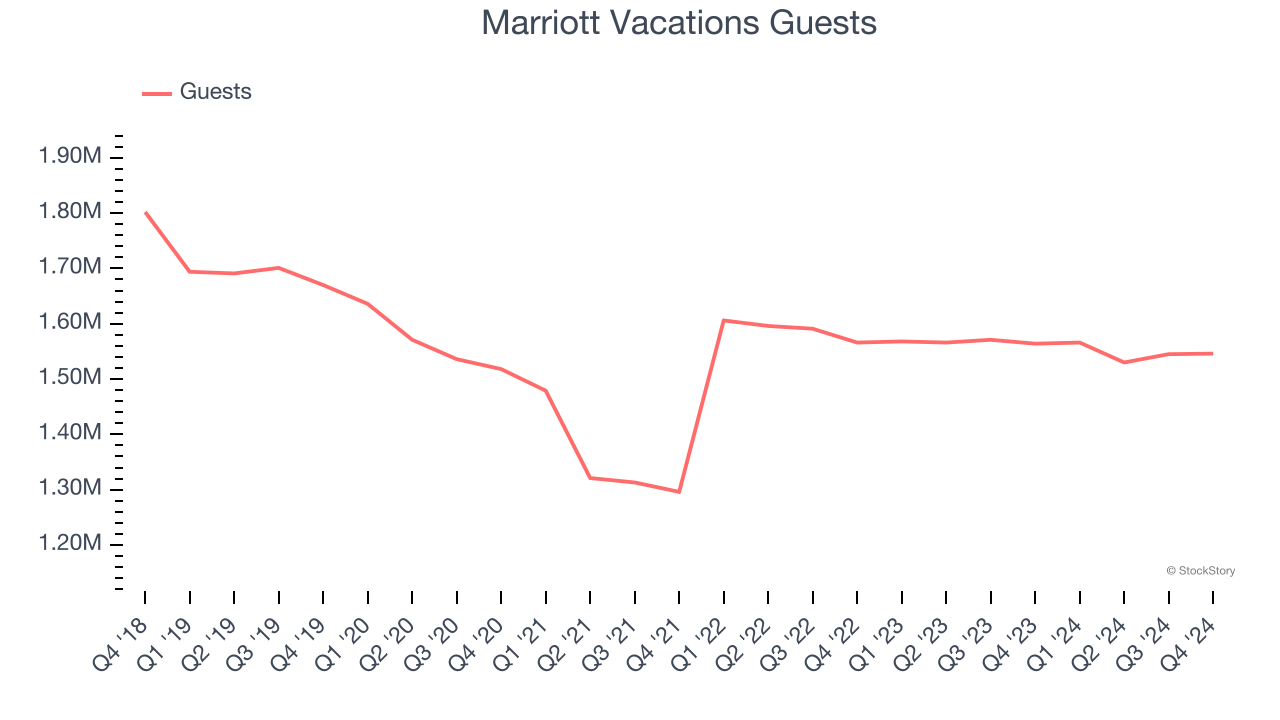

- Guests: 1.55 million, down 18,000 year on year

- Market Capitalization: $2.98 billion

“We had a strong end of the year, reflecting the resilience of our leisure-focused business model and the success of the initiatives we launched last year, with contract sales growing 7% year-over-year in the fourth quarter,” said John Geller, president and chief executive officer.

Company Overview

Spun off from Marriott International in 1984, Marriott Vacations (NYSE: VAC) is a vacation company providing leisure experiences for travelers around the world.

Travel and Vacation Providers

Airlines, hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional airlines, hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

Sales Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Marriott Vacations’s 2.7% annualized revenue growth over the last five years was weak. This fell short of our benchmarks and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Marriott Vacations’s annualized revenue growth of 3.3% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can dig further into the company’s revenue dynamics by analyzing its number of guests and conducted tours, which clocked in at 1.55 million and 113,828 in the latest quarter. Over the last two years, Marriott Vacations’s guests averaged 1.4% year-on-year declines. On the other hand, its conducted tours averaged 5.7% year-on-year growth.

This quarter, Marriott Vacations reported year-on-year revenue growth of 11.1%, and its $1.33 billion of revenue exceeded Wall Street’s estimates by 6.7%.

Looking ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its products and services will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

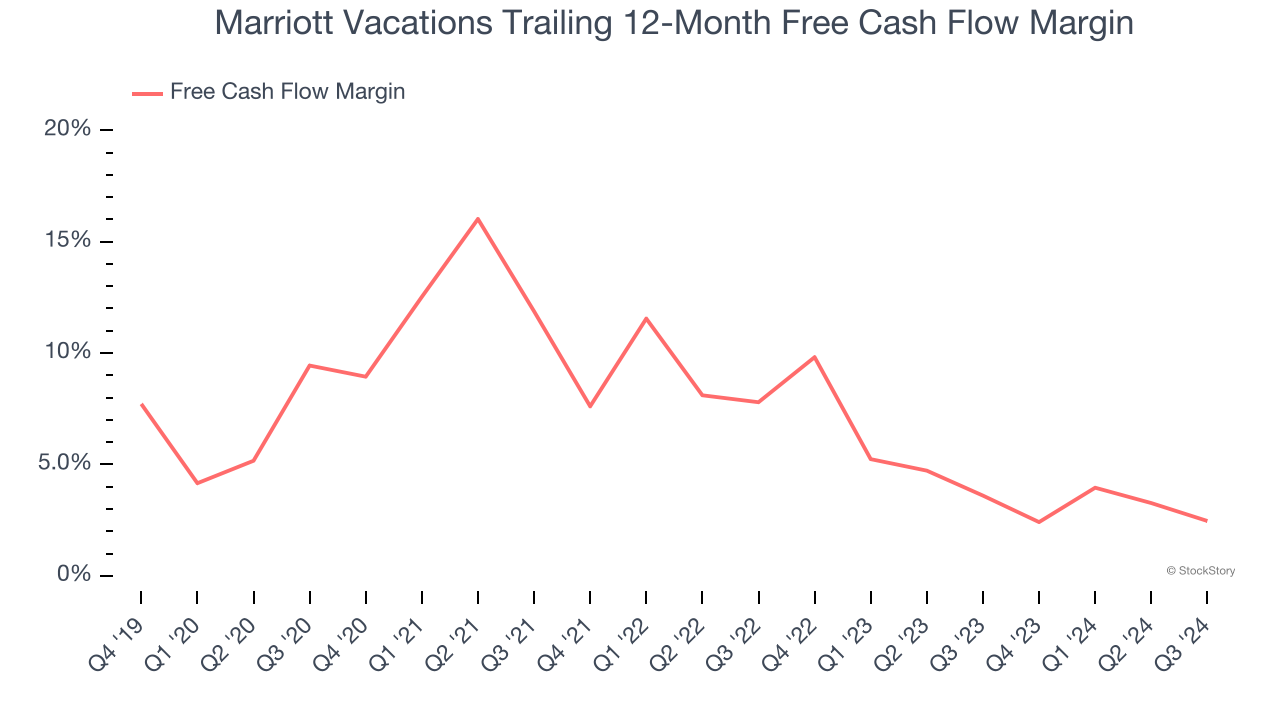

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Marriott Vacations has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.1%, lousy for a consumer discretionary business.

Key Takeaways from Marriott Vacations’s Q4 Results

We enjoyed seeing Marriott Vacations beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its number of guests fell short of Wall Street’s estimates. Overall, we think this was a mixed quarter. The stock remained flat at $84.75 immediately after reporting.

Is Marriott Vacations an attractive investment opportunity at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.