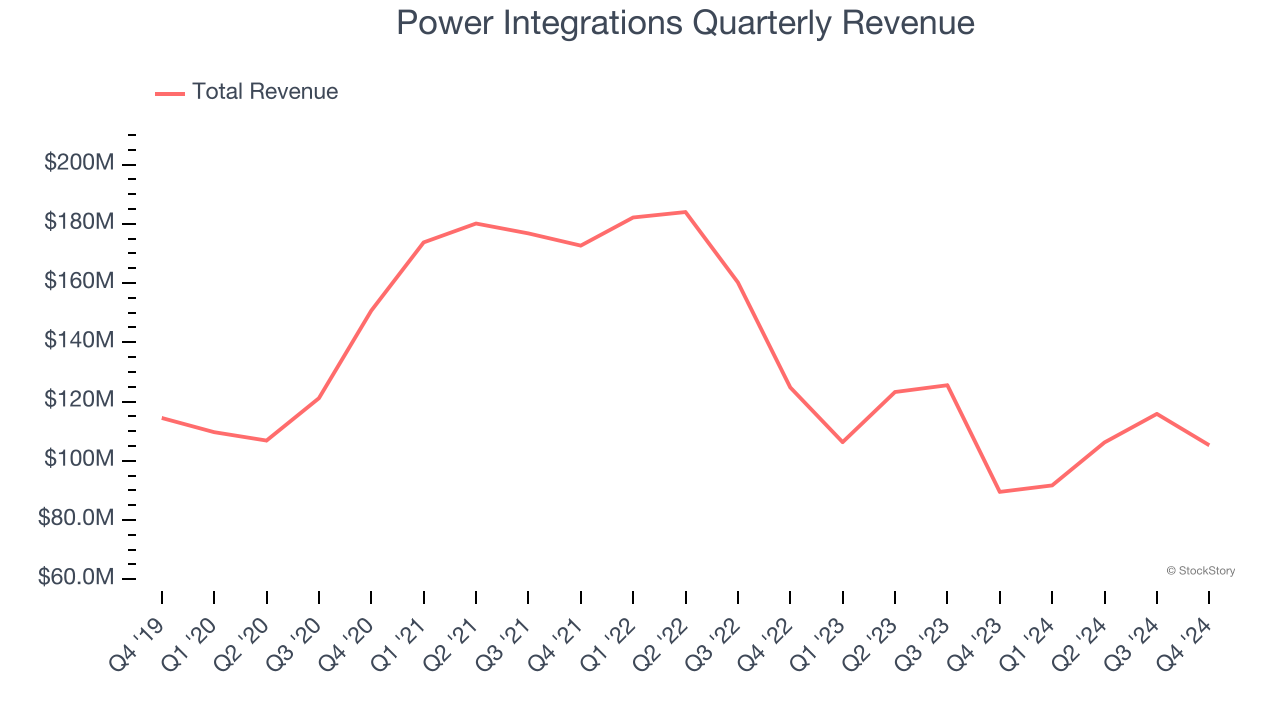

Semiconductor designer Power Integrations (NASDAQ: POWI) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 17.6% year on year to $105.3 million. On the other hand, next quarter’s revenue guidance of $105,250 was less impressive, coming in 99.9% below analysts’ estimates. Its non-GAAP profit of $0.30 per share was 8.7% above analysts’ consensus estimates.

Is now the time to buy Power Integrations? Find out by accessing our full research report, it’s free.

Power Integrations (POWI) Q4 CY2024 Highlights:

- Revenue: $105.3 million vs analyst estimates of $105.1 million (17.6% year-on-year growth, in line)

- Adjusted EPS: $0.30 vs analyst estimates of $0.28 (8.7% beat)

- Adjusted Operating Income: $13.36 million vs analyst estimates of $13.43 million (12.7% margin, 0.6% miss)

- Revenue Guidance for Q1 CY2025 is $105.25 million at the midpoint, below analyst estimates of $106 million

- Operating Margin: 3.7%, up from -1.2% in the same quarter last year

- Free Cash Flow Margin: 11.1%, similar to the same quarter last year

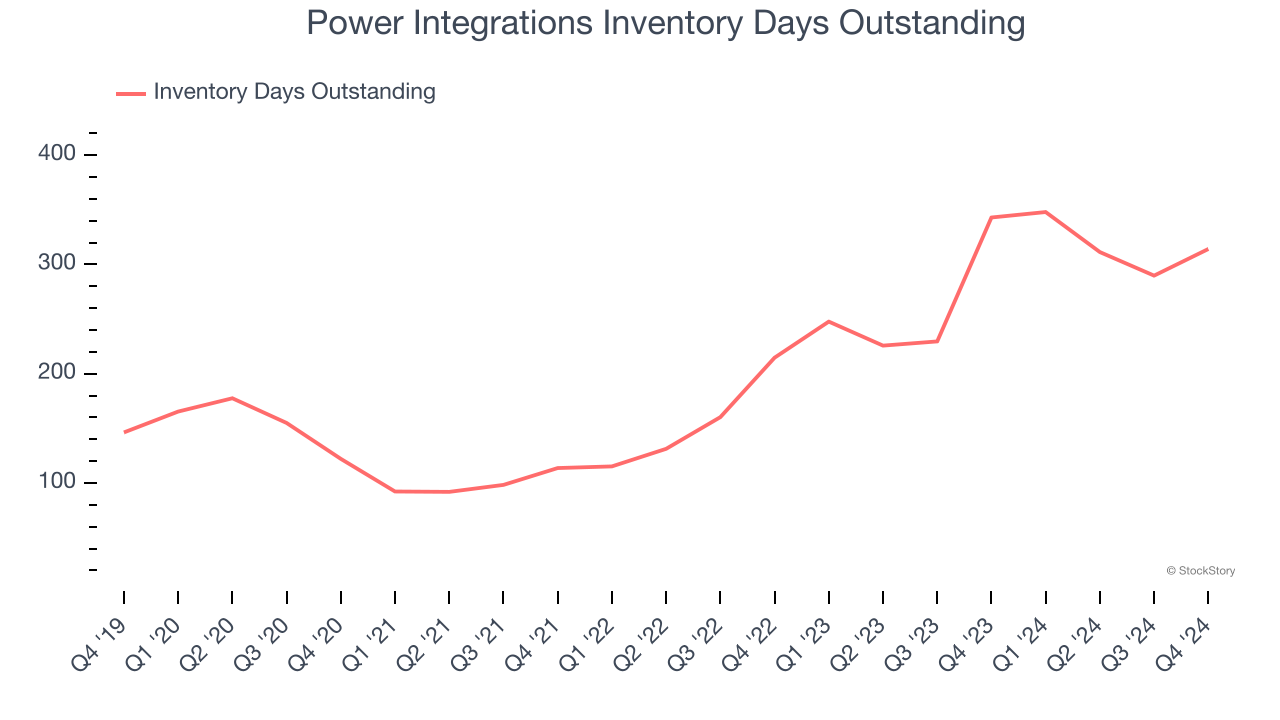

- Inventory Days Outstanding: 314, up from 290 in the previous quarter

- Market Capitalization: $3.55 billion

Company Overview

A leading supplier of parts for electronics such as home appliances, Power Integrations (NASDAQ: POWI) is a semiconductor designer and developer specializing in products used for high-voltage power conversion.

Analog Semiconductors

Demand for analog chips is generally linked to the overall level of economic growth, as analog chips serve as the building blocks of most electronic goods and equipment. Unlike digital chip designers, analog chip makers tend to produce the majority of their own chips, as analog chip production does not require expensive leading edge nodes. Less dependent on major secular growth drivers, analog product cycles are much longer, often 5-7 years.

Sales Growth

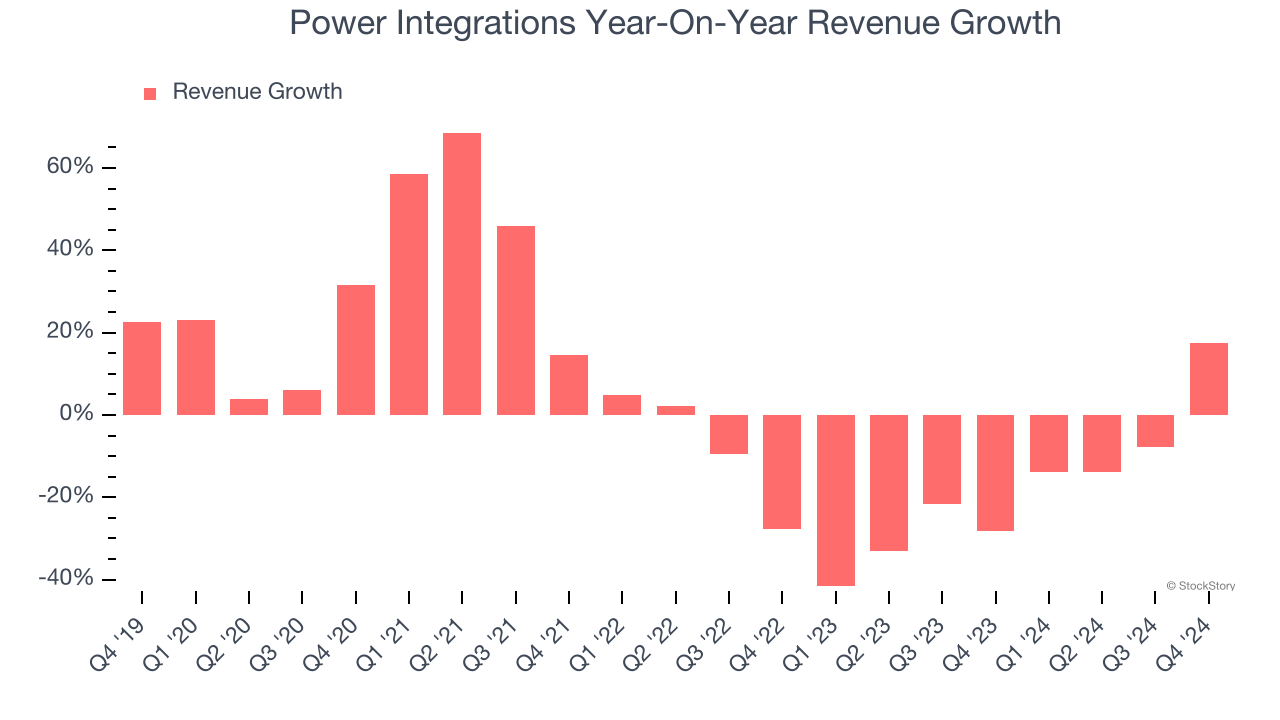

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Power Integrations struggled to consistently increase demand as its $419 million of sales for the trailing 12 months was close to its revenue five years ago. This fell short of our benchmarks and is a sign of poor business quality. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Power Integrations’s recent history shows its demand has stayed suppressed as its revenue has declined by 19.8% annually over the last two years.

This quarter, Power Integrations’s year-on-year revenue growth was 17.6%, and its $105.3 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 99.9% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 14% over the next 12 months, an improvement versus the last two years. This projection is admirable and implies its newer products and services will catalyze better top-line performance.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Power Integrations’s DIO came in at 314, which is 117 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

Key Takeaways from Power Integrations’s Q4 Results

We liked how Power Integrations beat analysts’ EPS expectations this quarter. On the other hand, its revenue in the quarter was just in line and its guidance for next quarter missed and its inventory levels increased. Overall, this quarter could have been better. The stock remained flat at $60.75 immediately following the results.

So do we think Power Integrations is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.