The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Mister Car Wash (NASDAQ: MCW) and the rest of the specialized consumer services stocks fared in Q3.

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

The 11 specialized consumer services stocks we track reported a mixed Q3. As a group, revenues missed analysts’ consensus estimates by 19.3% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.5% since the latest earnings results.

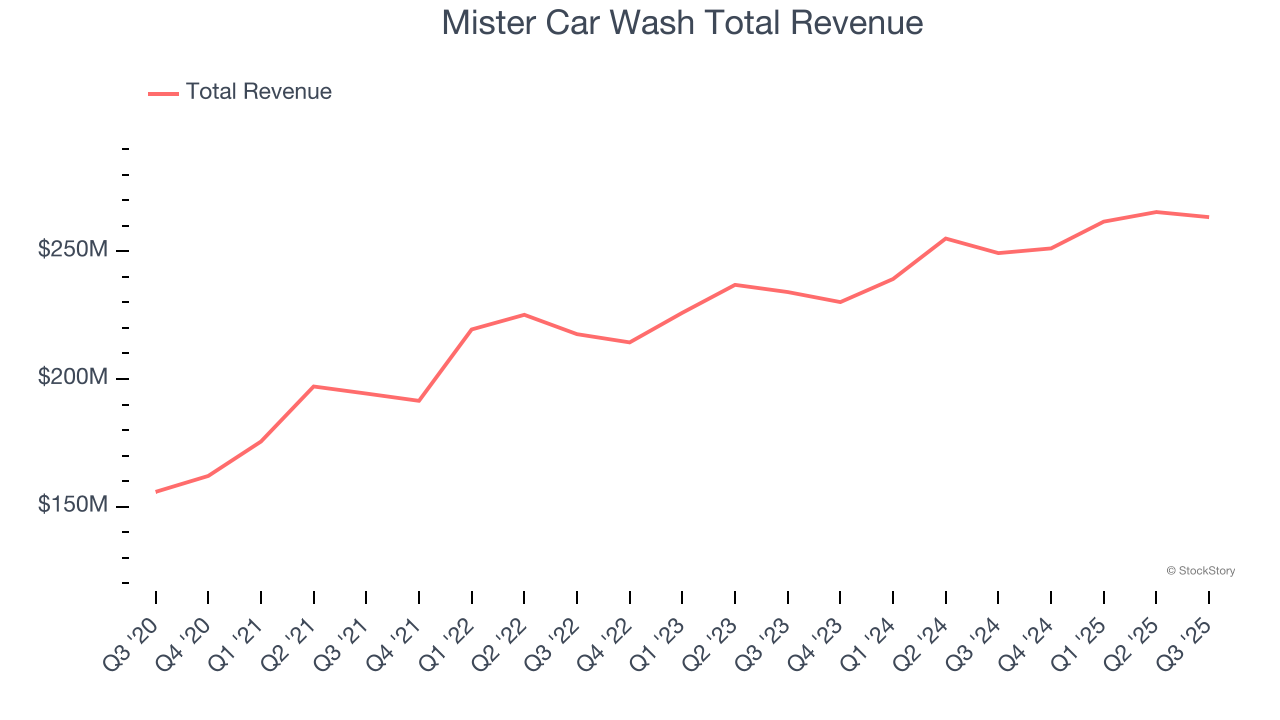

Mister Car Wash (NASDAQ: MCW)

Formerly known as Hotshine Holdings, Mister Car Wash (NYSE: MCW) offers car washes across the United States through its conveyorized service.

Mister Car Wash reported revenues of $263.4 million, up 5.7% year on year. This print exceeded analysts’ expectations by 0.9%. Overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ same-store sales estimates.

“We delivered a solid third quarter performance, underscoring the strength of our strategy, the resilience of our business model, and the dedication of our team,” said John Lai, Chairperson and CEO of Mister Car Wash.

Interestingly, the stock is up 7.1% since reporting and currently trades at $5.57.

Is now the time to buy Mister Car Wash? Access our full analysis of the earnings results here, it’s free for active Edge members.

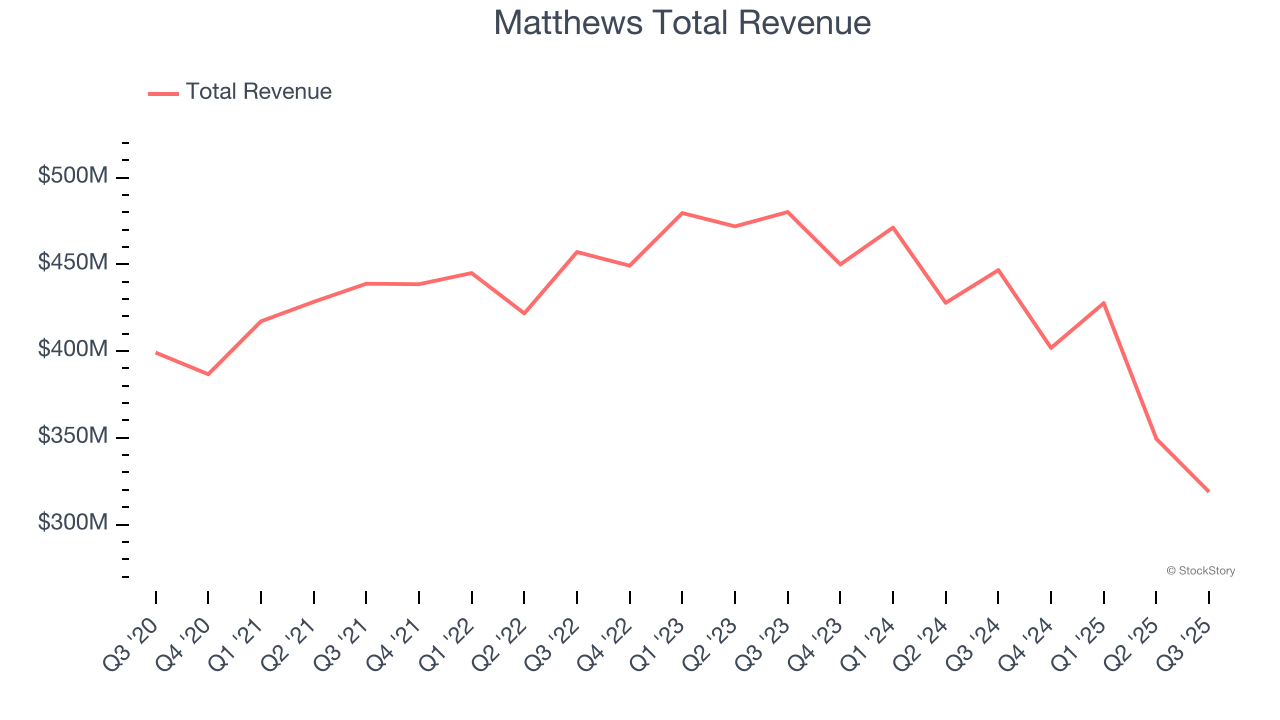

Best Q3: Matthews (NASDAQ: MATW)

Originally a death care company, Matthews International (NASDAQ: MATW) is a diversified company offering ceremonial services, brand solutions and industrial technologies.

Matthews reported revenues of $318.8 million, down 28.6% year on year, outperforming analysts’ expectations by 9.6%. The business had a very strong quarter with a beat of analysts’ EPS and revenue estimates.

Matthews pulled off the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 5.2% since reporting. It currently trades at $25.94.

Is now the time to buy Matthews? Access our full analysis of the earnings results here, it’s free for active Edge members.

Slowest Q3: 1-800-FLOWERS (NASDAQ: FLWS)

Founded in 1976, 1-800-FLOWERS (NASDAQ: FLWS) is an online retailer of flowers, gifts, and gourmet foods, serving customers globally.

1-800-FLOWERS reported revenues of $215.2 million, down 11.1% year on year, falling short of analysts’ expectations by 1.2%. It was a softer quarter as it posted a significant miss of analysts’ EPS and revenue estimates.

Interestingly, the stock is up 4.4% since the results and currently trades at $3.65.

Read our full analysis of 1-800-FLOWERS’s results here.

Frontdoor (NASDAQ: FTDR)

Established in 2018 as a spin-off from ServiceMaster Global Holdings, Frontdoor (NASDAQ: FTDR) is a provider of home warranty and service plans.

Frontdoor reported revenues of $618 million, up 14.4% year on year. This result topped analysts’ expectations by 1.1%. More broadly, it was a mixed quarter as it also logged a decent beat of analysts’ EBITDA estimates but EBITDA guidance for next quarter missing analysts’ expectations.

Frontdoor scored the fastest revenue growth among its peers. The stock is down 13.2% since reporting and currently trades at $57.09.

Read our full, actionable report on Frontdoor here, it’s free for active Edge members.

ADT (NYSE: ADT)

Founded in 1874 and headquartered in Boca Raton, Florida, ADT (NYSE: ADT) is a provider of security, automation, and smart home solutions, offering comprehensive services for home and business protection.

ADT reported revenues of $1.30 billion, up 4.4% year on year. This print was in line with analysts’ expectations. Aside from that, it was a mixed quarter as it also produced a beat of analysts’ EPS estimates but a miss of analysts’ customers estimates.

ADT had the weakest full-year guidance update among its peers. The stock is down 8.6% since reporting and currently trades at $8.04.

Read our full, actionable report on ADT here, it’s free for active Edge members.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.