Over the past six months, D.R. Horton’s shares (currently trading at $142.17) have posted a disappointing 16.2% loss, well below the S&P 500’s 1% gain. This might have investors contemplating their next move.

Is there a buying opportunity in D.R. Horton, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think D.R. Horton Will Underperform?

Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons you should be careful with DHI and a stock we'd rather own.

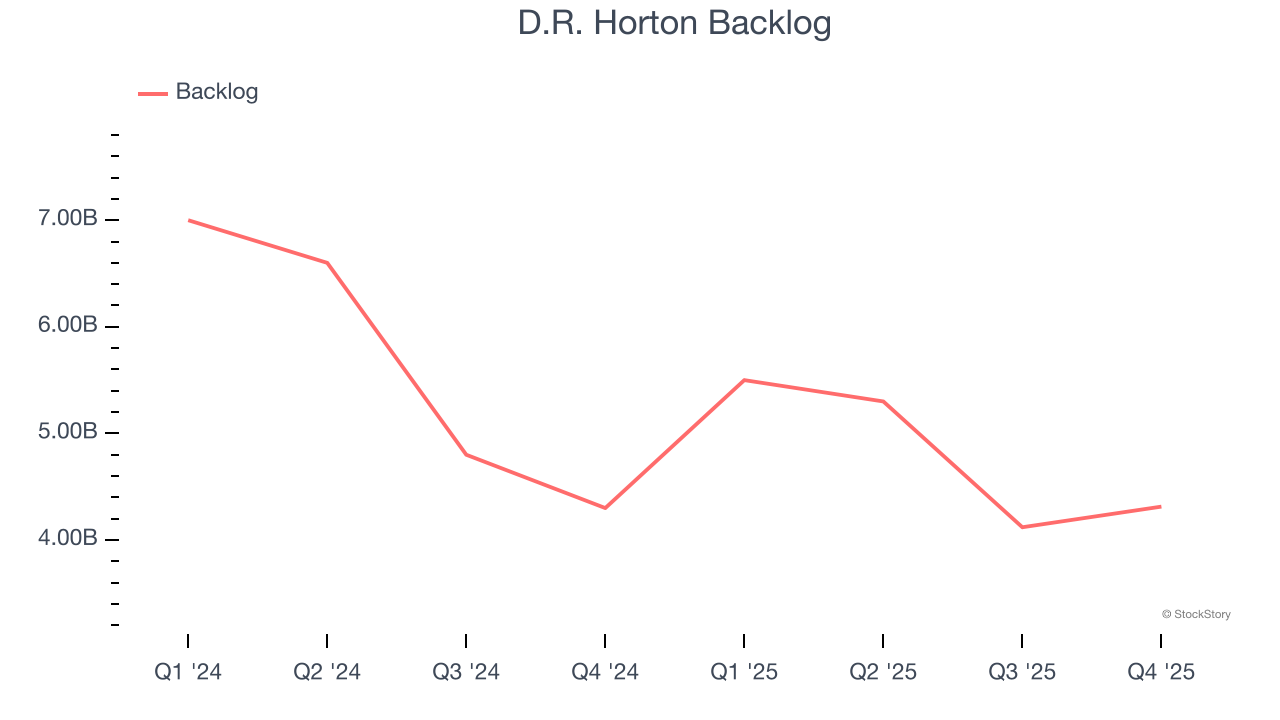

1. Backlog Declines as Orders Drop

We can better understand Home Builders companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into D.R. Horton’s future revenue streams.

D.R. Horton’s backlog came in at $4.31 billion in the latest quarter, and it averaged 13.7% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

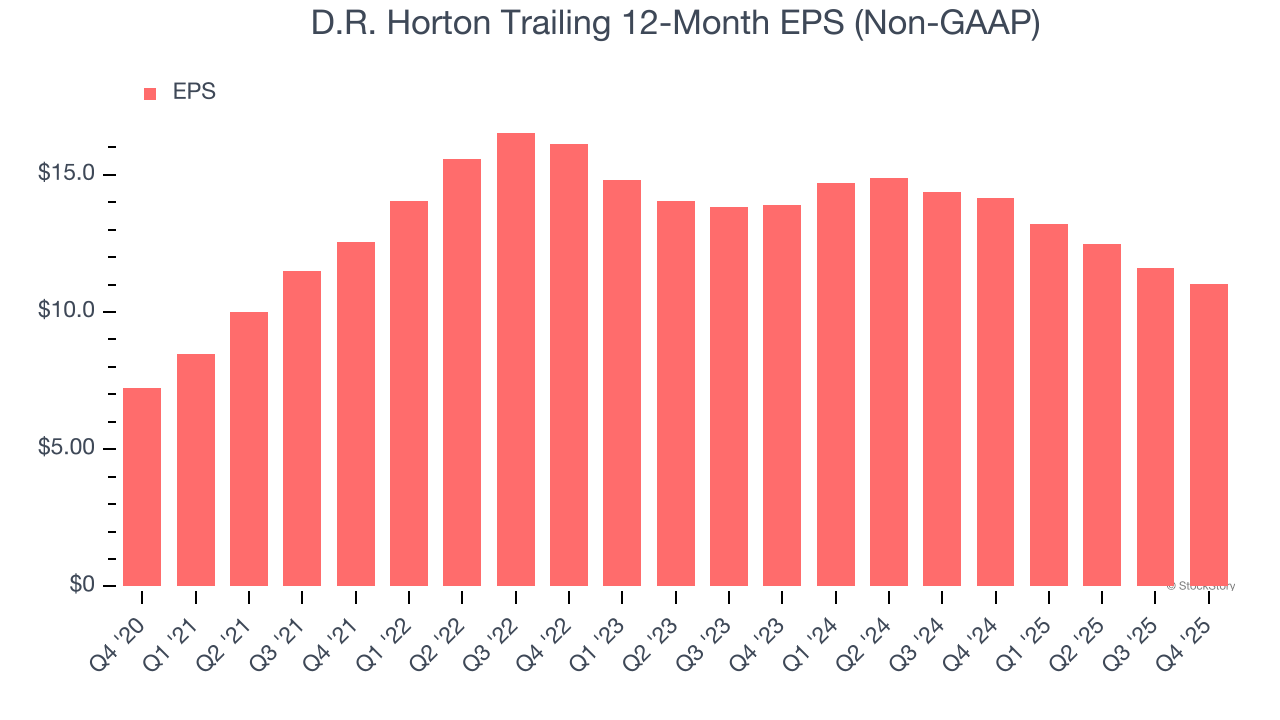

2. EPS Took a Dip Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Sadly for D.R. Horton, its EPS declined by more than its revenue over the last two years, dropping 11%. This tells us the company struggled to adjust to shrinking demand.

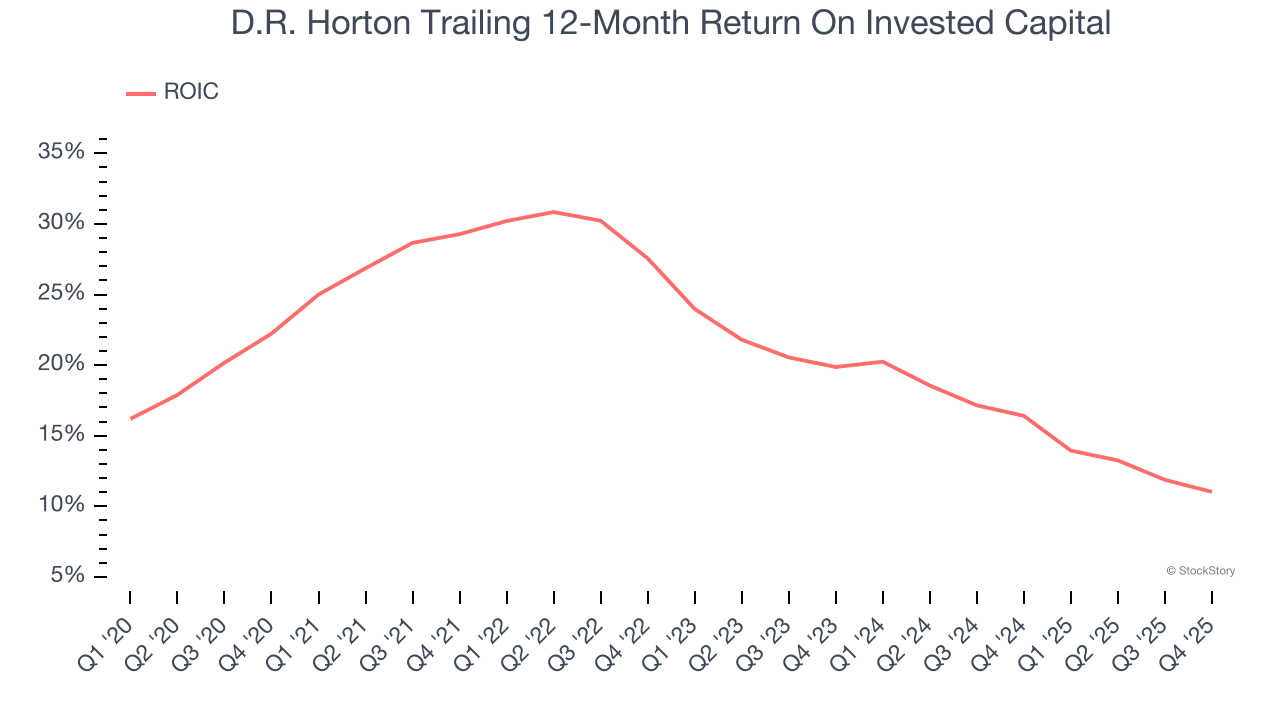

3. New Investments Fail to Bear Fruit as ROIC Declines

We like to invest in businesses with high returns, but the trend in a company’s ROIC can also be an early indicator of future business quality.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, D.R. Horton’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

D.R. Horton doesn’t pass our quality test. After the recent drawdown, the stock trades at 13.4× forward P/E (or $142.17 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are superior stocks to buy right now. We’d recommend looking at a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.